Cleveland-Cliffs Inc. (NYSE: CLF) is a steel producer with a focus on value-added sheet products, particularly for the automotive industry in North America. The Company is vertically integrated from the mining of iron ore, production of pellets and direct reduced iron, and processing of ferrous scrap through primary steelmaking and downstream finishing, stamping, tooling, and tubing.

Recent Business and Financial Updates

- Impact of Recent Steel Import Tariffs on Cleveland-Cliffs (CLF): Recent steel import tariffs imposed by the Trump administration, escalating from 25% to 50% effective June 4, 2025, are poised to benefit Cleveland-Cliffs Inc. (CLF), North America’s largest flat-rolled steel producer, by reducing foreign competition and potentially increasing domestic steel prices. Historically, tariffs have supported domestic steelmakers like Cleveland-Cliffs, as seen in 2018 when a 25% tariff improved pricing power, though the current doubling of tariffs has sparked concerns about demand reduction, particularly in the automotive sector, which constitutes 29% of CLF’s steelmaking revenues. While these tariffs could theoretically enhance capacity utilization for CLF, which has been operating at a lower rate—evidenced by recent idling of six facilities—the company’s optimism about reshoring automotive production suggests potential for increased utilization, though this is tempered by market dynamics and the risk of higher costs impacting downstream manufacturers, as noted in recent analyses.

- First-Quarter 2025 Financial Overview: Cleveland-Cliffs reported first-quarter 2025 consolidated revenues of USD 4.6 billion, a rise from USD 4.3 billion in Q4 2024, but recorded a GAAP net loss of USD 483 million (USD 1.00 per diluted share) and an adjusted net loss of USD 456 million (USD 0.92 per diluted share), compared to a Q4 2024 GAAP net loss of USD 434 million (USD 0.92 per diluted share) and an adjusted net loss of USD 332 million (USD 0.68 per diluted share). The Adjusted EBITDA loss widened to USD 174 million from USD 81 million in the prior quarter, reflecting challenges from underperforming non-core assets and the lingering impact of lower steel prices in late 2024 and early 2025. These financial results underscore the company’s struggles with profitability amid lower capacity utilization and market pressures, which the new tariffs may help alleviate by boosting domestic demand.

- Operational Restructuring and Cost Savings: Between March and May 2025, Cleveland-Cliffs idled six facilities, including the Minorca and Hibbing Taconite mines in Minnesota, the Dearborn Works blast furnace in Michigan, and plants in Steelton, Conshohocken, and Riverdale, to optimize its footprint, exit loss-making operations, and release excess working capital, expecting annual savings of over USD 300 million. The idlings, which do not impact flat-rolled steel output due to the planned restart of the #6 blast furnace at Cleveland Works, aim to improve efficiency and focus on core markets like automotive, though they highlight the company’s current underutilization of capacity. The tariffs may support increased utilization by driving demand to domestic producers, but the idlings suggest a cautious approach to scaling operations until market conditions stabilize.

- Strategic Focus and Market Positioning: CEO Lourenco Goncalves emphasized a strategic repositioning toward the automotive sector, which benefits from the Trump administration’s support for domestic vehicle production, securing higher volume commitments from automotive OEM customers to recover a stable EBITDA base. The company also plans to exit non-core markets like rail, high-carbon sheet, and specialty plate, and will not renew an unprofitable slab contract with ArcelorMittal/Nippon Steel Calvert, expected to add USD 500 million to annualized EBITDA starting in 2026. These moves align with the potential benefits of tariffs, which could increase domestic steel demand and allow Cleveland-Cliffs to better utilize its capacity, particularly in its core automotive segment.

- Steelmaking Segment Performance: The steelmaking segment reported Q1 2025 revenues of USD 4.5 billion, down from USD 5.0 billion in Q1 2024, with a gross margin loss of USD 400 million compared to a USD 270 million profit in Q1 2024, driven by a lower average net selling price per net ton (USD 980 versus USD 1,175) despite higher sales volumes of 4.1 million net tons. Sales distribution included 30% to infrastructure and manufacturing, 29% to automotive, 28% to distributors and converters, and 13% to steel producers, with product mix comprising 41% hot-rolled and 27% coated steel. The segment’s performance reflects underutilization challenges that the tariffs aim to address by potentially increasing domestic steel prices and demand, which could lead to higher capacity utilization if automotive production reshoring materializes as anticipated.

- Financial Outlook and Liquidity: Cleveland-Cliffs maintains a robust liquidity position with USD 3.0 billion as of March 31, 2025, and updated its 2025 outlook, projecting steel unit cost reductions of USD 50 per net ton (up from USD 40), capital expenditures of USD 625 million (down from USD 700 million), and selling, general, and administrative expenses of USD 600 million (down from USD 625 million). The company’s focus on cost reduction, operational efficiency, and the Stelco acquisition supports its strategy to restore cash flow generation and reduce debt, positioning it to capitalize on potential tariff-driven demand increases. While current capacity utilization remains low, the tariffs, combined with these strategic adjustments, provide a pathway for Cleveland-Cliffs to enhance its operational efficiency and market share in the domestic steel industry .

Technical Observation (on the daily chart):

The 14-day Relative Strength Index (RSI) is currently at 49.59, currently recovered from oversold levels, indicating bearishness, with the expectations of consolidation or downward momentum if the USD 8.00-USD 8.50 resistance is not broken on the upside. In addition, the current price is below both the 50-day Simple Moving Averages (SMAs) and 200-day SMA, which may work as medium to long term resistance levels.

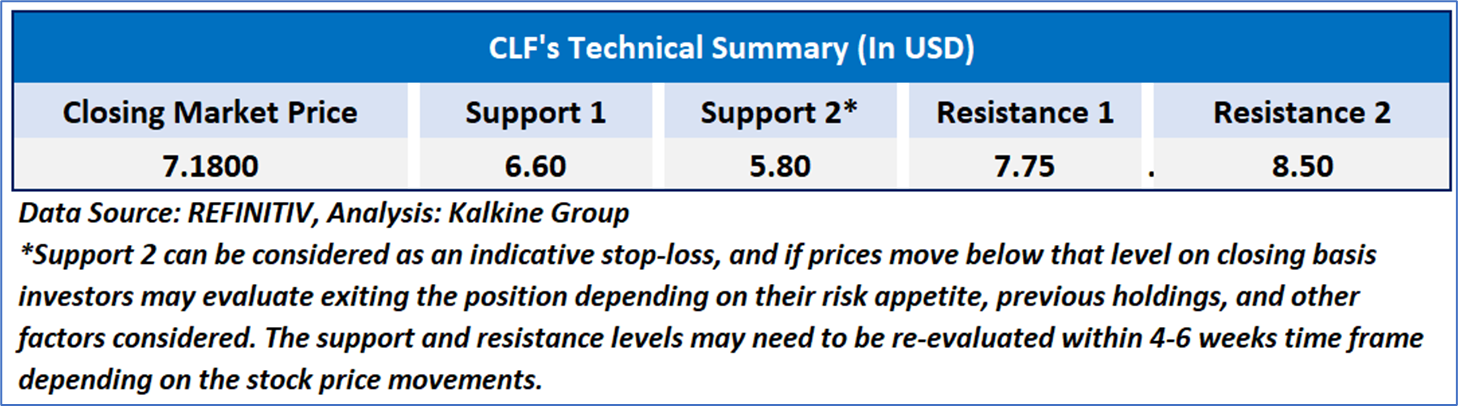

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘WATCH’ rating has been given Cleveland-Cliffs Inc. (NYSE: CLF) at the closing price of USD 7.18, as of June 02, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is June 02, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...