The Home Depot, Inc

The Home Depot, Inc (NYSE: HD) operates as a home improvement retailer, providing a broad range of products including building materials, home improvement supplies, lawn and garden items, home décor, and maintenance, repair, and operations (MRO) products, both in-store and through its online platforms.

Positive Growth Aspects

Growth Challenges

Technical Observation (on the daily chart):

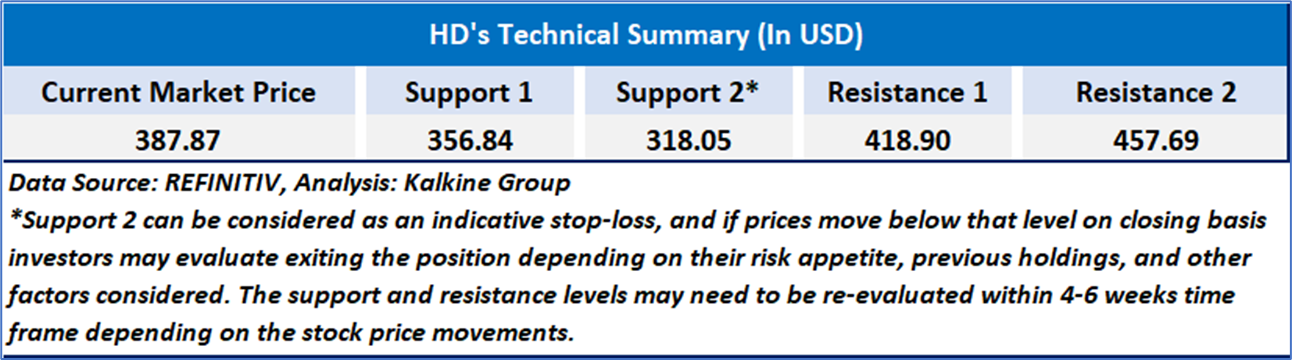

Home Depot's stock has recently turned technically bullish, with a breakout above both its 21-day and 50-day moving averages and a positive crossover indicating upward momentum. The RSI at 65.96 reflects strong but not yet overbought conditions, while rising volume supports the current uptrend.

The Home Depot delivered solid revenue growth of 9.4% in Q1 FY2025, supported by strong performance in Pro segments, increased digital engagement, and strategic sourcing flexibility. However, the company faced margin compression, with adjusted EPS down 3% and gross margins pressured by mix shifts and rising expenses. While consumer demand remained resilient for smaller projects, larger remodeling activity continued to lag due to high interest rates and macro uncertainty. The outlook remains cautiously optimistic as Home Depot leverages its Pro ecosystem and operational strengths to navigate a complex environment.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given to The Home Depot, Inc (NYSE: HD) at the current market price of USD 387.87 as of Aug 08,2025 at 10:30 am PDT.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is August 08,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Disclaimer This report has been issued by Kalkine New Zealand Limited (FSP691351) (NZBN:9429047678101) (“Kalkine”). Kalkine is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity securities, managed funds and other managed investment schemes and other financial advice products. The recommendations and opinions in this report and on Kalkine website do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...