Dun & Bradstreet Holdings, Inc

Dun & Bradstreet Holdings, Inc (NYSE: DNB) operates globally as a provider of data and analytics solutions that support business decision-making.

Positive Growth Aspects

- Steady Revenue Growth and Margin Expansion: Dun & Bradstreet reported Q1 2025 revenue of USD 579.8 million, representing a 2.7% year-over-year increase, with an organic growth rate of 3.6%. This reflects resilience in core business segments and stability in demand across markets. The company maintained growth despite macroeconomic uncertainties, with consistent performance across both North America and international regions. Additionally, Adjusted Revenue year-over-year growth before foreign currency impacts stood at 4.2%, further highlighting operational strength.

- Improvement in Adjusted EBITDA and Profitability: The company posted Adjusted EBITDA of USD 210.9 million in Q1 2025, marking a 4.8% year-over-year increase. The Adjusted EBITDA margin improved by 70 basis points to 36.4%, reflecting enhanced operational efficiency. Segment-level performance in North America was especially strong, with North America delivering a 41.8% EBITDA margin, up from 39.3% in the previous year. The international segment also remained profitable, maintaining a stable margin above 33%.

- Strong Cash Generation and Liquidity Position: Dun & Bradstreet generated USD 136.9 million in operating cash flow in Q1 2025, showing continued ability to convert profits into cash. The company ended the quarter with USD 241.3 million in cash and equivalents, up from USD 205.9 million in December 2024. The ability to increase liquidity while continuing to invest in technology and software demonstrates sound financial management and prudent capital allocation.

- Robust Performance in Strategic Segments: Within North America, the Finance & Risk segment grew to USD 216.6 million, while Sales & Marketing revenue reached USD 181.4 million. These segments delivered a combined Adjusted EBITDA of USD 166.2 million, accounting for nearly 79% of the total company EBITDA. This concentration of profitability in high-value services indicates a strategic focus on scalable and high-margin offerings, supporting long-term value creation.

Growth Challenges

- Persistent GAAP Net Losses: Despite improvements in adjusted metrics, Dun & Bradstreet reported a GAAP net loss of USD 15.8 million in Q1 2025. This marks the fourth consecutive quarterly loss, raising concerns about sustained profitability under GAAP accounting. The negative bottom-line result is largely attributable to high depreciation, amortization, and interest expenses, suggesting structural cost pressures and heavy investment burdens.

- Elevated Non-Operating Expenses and Debt Levels: Interest expense remains a drag on profitability, standing at USD 52.9 million for the quarter, only slightly improved from the previous year. Long-term debt totaled USD 3.5 billion, with high leverage ratios likely to constrain financial flexibility. The company also recorded non-operating losses of USD 50.1 million, reinforcing the impact of its capital structure on reported results.

- Continued Decline in International Profit Margins: While international revenue posted modest growth, the Adjusted EBITDA margin for the international segment fell to 33.3% in Q1 2025 from 36.1% in Q1 2024. The decline in operating leverage within this region could signal rising cost pressures or weaker execution compared to North America. Additionally, international adjusted EBITDA declined sequentially from Q4 2024 (USD 58.1 million) to Q1 2025 (USD 60.5 million), highlighting the challenge of maintaining efficiency across geographies.

- Weak Return Metrics and Decline in Equity: The company's accumulated deficit widened to USD 855.5 million, up from USD 839.7 million at the end of 2024, indicating an erosion of retained earnings. Equity also declined slightly, and treasury stock increased, implying share repurchases were not offset by gains elsewhere. Moreover, despite adjusted EPS growth, GAAP EPS remained negative at -USD 0.04, pointing to the gap between operational performance and shareholder return.

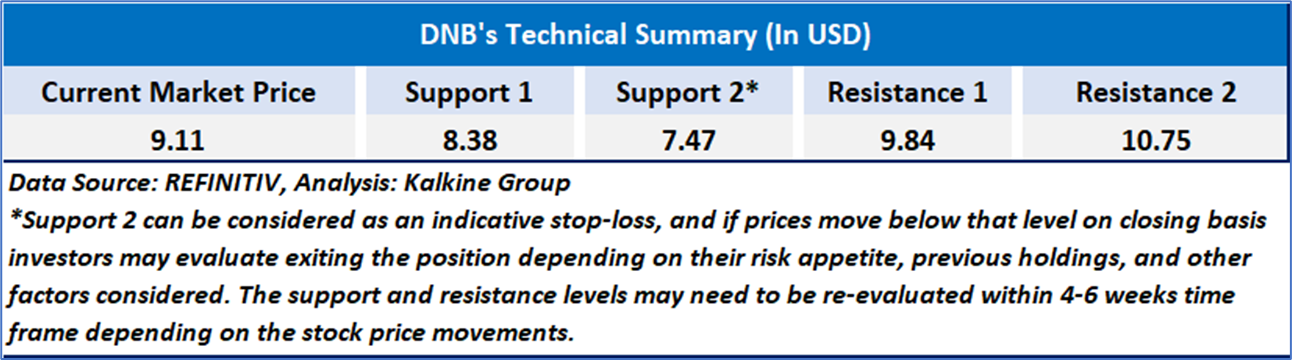

Technical Observation (on the daily chart):

DNB shows a period of consolidation following a prior downtrend, with the price stabilizing around USD 9.11. The 21-day and 50-day moving averages have converged, reflecting indecision in market direction, while the RSI at 52.32 indicates neutral momentum. Low trading volume further supports the view of limited investor activity, suggesting the stock is in a wait-and-watch phase with no clear breakout or breakdown signal yet.

Dun & Bradstreet's Q1 2025 performance presents a mixed picture, reflecting both operational strength and financial headwinds. On the positive side, the company delivered solid year-over-year revenue growth of 2.7% with a stronger 3.6% organic increase, alongside a higher adjusted EBITDA margin of 36.4%, signaling improved operational efficiency. Strong cash flow generation and resilient performance in North America further underscore stability in core segments. However, persistent GAAP net losses, high interest expenses, and a sizable debt burden weigh on profitability. Additionally, the international segment saw a margin decline, and equity erosion continued with an increasing accumulated deficit, highlighting ongoing structural challenges despite underlying growth.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given to Dun & Bradstreet Holdings, Inc (NYSE: DNB) at the current market price of USD 9.11 as of Aug 08,2025 at 10:15 am PDT.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is August 08,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...