REV Group, Inc

REV Group, Inc (NYSE: REVG) designs, manufactures, and distributes specialty vehicles along with related aftermarket parts and services. It serves a diverse range of customers, primarily across North America. The company operates through two main segments: Specialty Vehicles and Recreational Vehicles.

Positive Growth Aspects

- Impressive Sales Growth and Margin Expansion: REV Group delivered robust revenue growth in Q2 2025, achieving net sales of USD 629.1 million — a USD 45.1 million (7.7%) increase over the prior year quarter when excluding the discontinued Bus Manufacturing Businesses. The Specialty Vehicles segment was the main driver, posting a 12.2% increase in net sales, fueled by strong demand and increased shipments of fire apparatus and ambulances. The company's strategic exit from the lower-margin Bus Manufacturing Businesses allowed it to focus on its core specialty and recreational segments, improving overall profitability.

- Substantial EBITDA and Net Income Improvement: The company reported a significant 63.6% increase in Adjusted EBITDA, rising to USD 58.9 million from USD 37.5 million in the previous year’s quarter (excluding bus impact). Adjusted Net Income also rose strongly to USD 35.4 million, up from USD 20.9 million, underscoring improved operational efficiency and effective pricing strategies. This performance was further bolstered by favorable price realization and an improved product mix within the Specialty Vehicles segment.

- Healthy Backlog and Demand Visibility: The Specialty Vehicles backlog rose by USD 272.4 million year-over-year, signaling sustained customer demand. A strong order pipeline, particularly for fire apparatus and ambulances, positions the company for continued revenue visibility and stability in future quarters. This backlog growth supports management’s decision to accelerate capital investment—highlighted by a planned USD 20 million expansion in Brandon, South Dakota—aimed at boosting production throughput to meet demand.

- Shareholder Value Creation and Solid Liquidity: REV Group continues to prioritize shareholder returns through an aggressive share buyback program, repurchasing 2.9 million shares for USD 88.4 million in Q2 2025. It also maintains a healthy liquidity position, with USD 263.2 million available under its revolving credit facility and net debt of just USD 101.2 million. The Board’s approval of a USD 0.06 quarterly dividend further demonstrates confidence in the company’s cash generation capabilities and future growth prospects.

Growth Challenges

- Weak Performance in the Recreational Vehicles Segment: Despite the strong results in Specialty Vehicles, the Recreational Vehicles (RV) segment showed softness, with net sales declining 2.4% to USD 175.3 million. Lower unit shipments and heightened dealer incentives weighed on performance. Furthermore, the RV segment backlog declined slightly by USD 6.8 million, reflecting weaker order intake in certain categories — an indicator of potential headwinds in consumer demand, possibly linked to macroeconomic uncertainty and higher interest rates.

- Profitability Pressures in RV Segment: The RV segment’s Adjusted EBITDA fell nearly 10%, decreasing to USD 10.9 million from USD 12.1 million year-over-year. This contraction in profitability was driven by reduced shipments and increased dealer support costs, which offset gains from pricing actions and cost reduction efforts. This ongoing margin pressure suggests that the RV segment may struggle to contribute meaningfully to overall profit growth in the near term, especially if market demand remains subdued.

- Inflationary and Input Cost Headwinds: Though Specialty Vehicles delivered strong gains, management acknowledged the impact of inflationary pressures on profitability. Unfavorable product mix and rising costs for materials and labor are challenges that could persist, potentially dampening future margin expansion. These inflationary trends, if not adequately managed through pricing or efficiency initiatives, could erode the company’s recent EBITDA gains.

- Reduced Liquidity Cushion and Working Capital Decline: The company’s available credit facility decreased by USD 86.4 million since October 2024, while trade working capital dropped to USD 207.3 million from USD 248.2 million. Although management cited timing factors such as payables and customer advances, the reduced liquidity and working capital could limit flexibility in addressing unforeseen market disruptions. Additionally, the sale of bus assets and concentrated investments in Specialty Vehicles increase dependency on a narrower product base, raising strategic concentration risks.

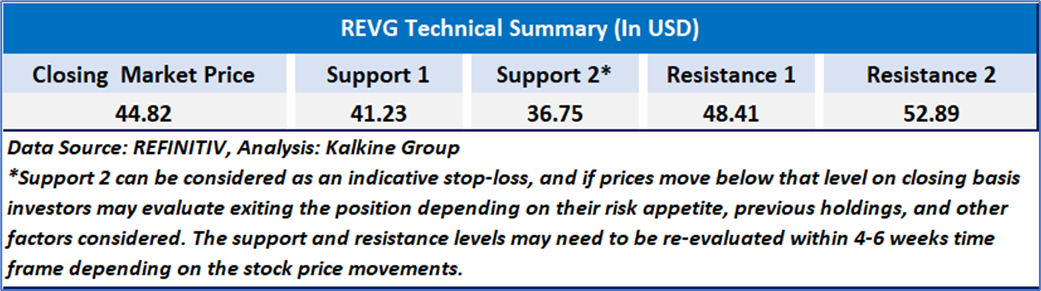

Technical Observation (on the daily chart):

The chart for REVG shows a strong bullish trend, with the stock recently breaking out above prior resistance near USD 40, supported by rising 21-day and 50-day moving averages. The breakout is validated by a significant volume spike, indicating strong buying interest. However, the RSI at 80.89 signals overbought conditions, suggesting potential for short-term consolidation.

REV Group’s Q2 2025 results reflect a mixed performance. The company delivered strong revenue growth and significant margin expansion, driven largely by its Specialty Vehicles segment, which benefited from robust demand for fire apparatus and ambulances. Adjusted EBITDA and net income saw notable gains, supported by operational improvements and strategic capital investments. However, the Recreational Vehicles segment underperformed, facing declining sales and profitability amid softer consumer demand and increased dealer incentives. Additionally, inflationary pressures and a reduced liquidity cushion present ongoing challenges. While REV Group’s focused portfolio and healthy backlog offer future growth potential, near-term risks in certain markets and cost headwinds warrant cautious optimism.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given to REV Group, Inc (NYSE: REVG) at the closing market price of USD 44.82 as of Jun 06,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is June 06,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...