Zeta Global Holdings Corp

Zeta Global Holdings Corp (NYSE: ZETA) operates an omnichannel, data-driven cloud platform that provides enterprises with consumer insights and marketing automation solutions. Its software helps businesses identify, reach, and engage consumers by delivering personalized marketing across multiple channels, including email, social media, websites, chat, connected TV (CTV), video, and more.

Positive Growth Aspects and Growth Challenges

- Strong Revenue Growth and Profitability Momentum: Zeta Global delivered robust financial performance in Q2 2025, with revenue of $308 million, reflecting a 35% year-over-year increase and surpassing guidance by $11 million. This strong top-line growth highlights the increasing demand for its AI-powered marketing platform. The company also generated $42 million in net cash from operating activities, up 35% year-over-year, and achieved $34 million in free cash flow, a notable 69% increase. These metrics position Zeta among the faster-growing players in its sector. The company further demonstrated confidence in its trajectory by raising full-year 2025 revenue guidance to a range of $1,258–$1,268 million, representing 25%–26% growth. Adjusted EBITDA expectations were also raised to $263.6–$265.6 million, up 37%–38% year-over-year, with margins above 20%. Free cash flow guidance was meaningfully upgraded by $10.5 million at the midpoint, translating into growth of over 50%. This upward revision underscores management’s visibility into sustained demand and operating efficiency improvements.

- Shareholder-Friendly Capital Allocation: Zeta is actively rewarding shareholders through its repurchase initiatives. As of July 2025, the company had utilized $85 million of the $100 million authorization announced in November 2024, leaving $15 million remaining. In addition, the board approved a new $200 million stock repurchase program running through December 2027, reflecting management’s belief in the company’s long-term value creation potential. This commitment to capital returns, combined with the absence of net dilution in the quarter, reinforces investor confidence in Zeta’s ability to balance growth with shareholder value. By supplementing operating growth with buybacks, Zeta is also mitigating the dilutive effects of stock-based compensation (SBC), which remains an ongoing investor concern.

- Dependence on Stock-Based Compensation: Despite strong execution, Zeta’s reliance on equity-based compensation continues to weigh on its cost structure. The company expects SBC expenses to reach $190 million for FY25, which is substantial relative to its profitability profile. This practice, while helpful for talent retention in a competitive AI-driven sector, raises questions about long-term shareholder dilution and the sustainability of earnings growth on a per-share basis. Although Zeta’s repurchase programs partially offset dilution, the high level of SBC creates ongoing financial pressure. Investors may interpret this as a sign that the company must continue relying heavily on equity incentives to retain key talent, which could limit margin expansion in the long run.

- Execution Risk and Market Competition: While Zeta is on track to achieve its ambitious 2028 revenue and free cash flow targets, execution risk remains elevated. The company is heavily dependent on continued adoption of its AI-powered platform and successful deployment of new solutions such as Zeta Answers and the expanded Zeta Marketing Platform. Any slowdown in client wins, agency partnerships, or platform adoption could challenge its growth trajectory.: Additionally, Zeta operates in a highly competitive marketing technology landscape, where it competes against established players with deeper financial resources. To maintain its industry-leading growth rates, Zeta must continue innovating at scale while balancing profitability. The risk of market share erosion or slower-than-expected adoption represents a key headwind for investors monitoring its long-term performance.

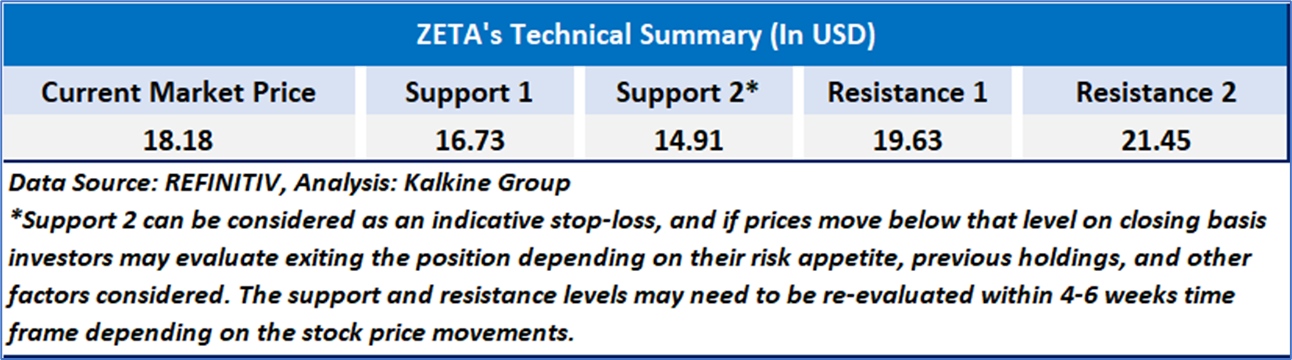

Technical Observation (on the daily chart):

ZETA stock shows a medium-term uptrend supported by the 50-day moving average, though the recent 7% drop on high volume signals short-term selling pressure. RSI sits near neutral at 50, indicating consolidation after prior gains. Holding above support keeps the bullish outlook intact, but a breakdown could trigger a deeper correction.

Zeta Global delivered a strong Q2 2025 with revenue up 35% year-over-year to $308 million, beating guidance, alongside a 69% jump in free cash flow and raised full-year outlook across revenue, EBITDA, and cash generation, highlighting robust demand for its AI-driven platform. The company also reinforced shareholder returns through $85 million in buybacks and the launch of a new $200 million repurchase program, signaling confidence in long-term value creation. However, heavy reliance on stock-based compensation, expected at $190 million for FY25, continues to pose dilution concerns, while execution risk remains elevated in a competitive marketing technology landscape. This combination presents both strong growth momentum and structural challenges, offering a mixed investment rationale.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given to Zeta Global Holdings Corp (NYSE: ZETA) at the closing market price of USD 18.18 as of September 02,2025 at 10:10 am PDT.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is September 02,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...