Zeta Global Holdings Corp (NYSE: ZETA)

Zeta Global Holdings Corp (NYSE: ZETA) operates a data-driven cloud platform that helps enterprises enhance consumer intelligence and automate marketing. Its software enables businesses to target, connect with, and engage consumers through personalized marketing across multiple channels, including email, social media, websites, chat, connected TV (CTV), and video.

Recent Business and Financial Updates

- Zeta Global Reports Strong Revenue Growth in 2024: Zeta Global (NYSE: ZETA), a leading AI-powered marketing cloud, announced its financial results for the fourth quarter and full year ending December 31, 2024. The company delivered USD 315 million in revenue in Q4 2024, marking a 50% year-over-year (Y/Y) increase, and USD 1.006 billion in total revenue for 2024, representing 38% Y/Y growth. The company attributes its consistent expansion to its strategic investments in AI and first-party data, which continue to drive customer engagement and market share gains.

- Customer Growth and Revenue Per User Expansion: Zeta Global demonstrated strong customer acquisition and engagement metrics in 2024. The Scaled Customer count grew by 17% Y/Y, while Super-Scaled Customer count increased by 13% Y/Y. Additionally, the company achieved a 19% increase in Scaled Customer average revenue per user (ARPU), reaching USD 1.87 million in 2024. The growth in customer base and revenue per user highlights Zeta’s ability to drive value for enterprises through its AI-driven marketing solutions.

- Profitability and Cash Flow Improvements: The company reported significant improvements in profitability, with GAAP net income of USD 15 million in Q4 2024, compared to a GAAP net loss of USD 35 million in Q4 2023. Furthermore, cash flow from operating activities reached USD 44 million in Q4 and USD 134 million for the full year, reflecting enhanced financial efficiency. Free Cash Flow improved to USD 92 million for 2024, up from USD 55 million in 2023. Zeta’s commitment to financial discipline and operational efficiencies contributed to these positive results.

- Consistent EBITDA Growth and Margin Expansion: Zeta Global achieved record levels of profitability, with Adjusted EBITDA reaching USD 70.4 million in Q4 2024, a 57% Y/Y increase, and USD 193.0 million for the full year, up 49% Y/Y. The Adjusted EBITDA margin improved to 22.4% in Q4, compared to 21.3% in the prior year, while the full-year margin rose to 19.2% from 17.8% in 2023. These figures underscore Zeta’s ability to scale its operations while maintaining strong profit margins.

- Guidance for 2025 Reflects Continued Growth: For Q1 2025, Zeta Global forecasts revenue between USD 253 million and USD 255 million, reflecting a 30% to 31% Y/Y growth rate. Adjusted EBITDA is expected to range between USD 44.2 million and USD 44.8 million, representing a 45% to 47% Y/Y increase. For the full year 2025, the company projects revenue between USD 1.235 billion and USD 1.245 billion, marking a 23% to 24% Y/Y increase. Adjusted EBITDA is expected to range between USD 255.5 million and USD 257.5 million, with a 20.5% to 20.8% EBITDA margin.

- Zeta 2028 Plan Aims for USD 2 Billion in Revenue: Zeta Global has outlined its Zeta 2028 plan, targeting at least USD 2.1 billion in annual revenue by 2028, representing a 20% organic compound annual growth rate (CAGR). Additionally, the company aims for Adjusted EBITDA of at least USD 525 million, reflecting a 25% margin, and Free Cash Flow of at least USD 340 million, with a 16% margin. These long-term objectives reinforce Zeta’s confidence in its business model and continued market expansion.

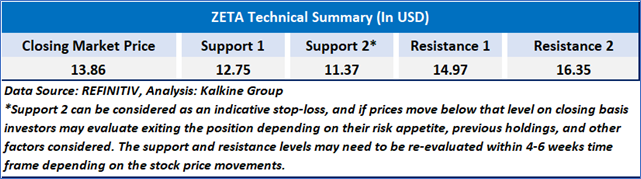

Technical Observation (on the daily chart):

ZETA is in a clear downtrend, trading below its 21-day and 50-day moving averages, with strong selling pressure. The stock has declined from its November 2024 peak above USD 35 and is now testing key support around USD 13.00-13.50. The RSI at 33.47 indicates bearish momentum but isn't yet oversold. A break below support could lead to further downside, while a recovery above USD 15 with strong volume would signal potential reversal.

ZETA delivered exceptional financial results in 2024, with 50% Y/Y revenue growth in Q4 and 38% Y/Y growth for the full year, surpassing USD 1 billion in annual revenue. Strong customer expansion, rising ARPU, and increased profitability highlight the company’s ability to scale effectively. With record-high Adjusted EBITDA, improving margins, and robust cash flow generation, Zeta continues to strengthen its financial position. Looking ahead, the company’s 2025 guidance projects continued double-digit growth, while its Zeta 2028 plan aims for over USD 2 billion in revenue, reinforcing confidence in its long-term vision and AI-driven strategy.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Buy’ rating has been given to Zeta Global Holdings Corp (NYSE: ZETA) at the closing market price of USD 13.86 as of March 18,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is March 18,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...