YUM! Brands Inc

YUM! Brands, Inc. (NYSE: YUM) oversee a global network of approximately 61,000 restaurants across 155 countries and territories, operating under the brands KFC, Taco Bell, Pizza Hut, and The Habit Burger Grill. The company is structured into four divisions: The KFC Division, responsible for KFC’s worldwide operations; The Taco Bell Division, managing Taco Bell locations globally; The Pizza Hut Division, overseeing Pizza Hut’s international presence; and The Habit Burger Grill Division, which handles the global operations of The Habit Burger Grill brand.

Recommendation Rationale –

· Declining Profitability Amid Growth: Despite reporting strong system sales and expansion efforts, Yum! Brands experienced a decline in GAAP earnings per share (EPS), which fell by 8% in the fourth quarter and 7% for the full year of 2024. While the company attributes some of this decline to special items and currency fluctuations, the overall downward trend in profitability raises concerns about operational efficiency. Even with an additional 53rd week contributing to revenues, Yum! failed to convert sales growth into sustainable profit increases, highlighting potential inefficiencies in cost management.

· Struggling Pizza Hut Performance: Pizza Hut, one of Yum! Brands’ major divisions, has continued to underperform compared to its counterparts. While Taco Bell and KFC demonstrated positive sales trends, Pizza Hut reported a 1% decline in full-year system sales and a concerning 4% drop in same-store sales. This downward trajectory indicates an ongoing struggle to remain competitive in an evolving fast-food landscape, where consumer preferences are shifting towards convenience-focused, digitally integrated dining experiences. The division’s operating profit also declined, further signaling the brand’s inability to drive meaningful growth.

· Franchisee Issues and Market Disruptions: Yum! Brands’ operations in Turkey faced significant setbacks, as the company terminated its agreements with franchisee IS Gida A.S. due to failure to meet its standards. This decision impacted 284 KFC and 254 Pizza Hut locations, creating operational instability in a key international market. The termination reflects broader challenges in maintaining franchisee compliance and quality control, which could lead to reputational damage and hinder future expansion in emerging markets.

· Questionable Digital Strategy and Execution: While Yum! Brands boasted a 15% increase in digital sales and the launch of its proprietary "Byte by Yum!" SaaS platform, questions remain about the execution and effectiveness of this digital transformation. Despite heavy investment, digital mix only barely surpassed 50%, indicating slow adoption rates. Furthermore, the consolidation of digital operations and restructuring efforts may have led to disruptions and inefficiencies. If the company's digital initiatives fail to deliver the promised efficiencies, the return on investment may not justify the resources allocated.

YUM’s Daily Price Chart

Valuation Methodology: Price/Earnings Approach (FY Dec'25E) (Illustrative)

Despite growth in sales and expansion, Yum! Brands faced declining profitability, with GAAP EPS down 8% in Q4 and 7% for 2024. Pizza Hut underperformed, same-store sales fell 4%, and franchisee issues in Turkey led to instability. Additionally, its digital transformation, including "Byte by Yum!," showed slow adoption, raising concerns about execution and efficiency.

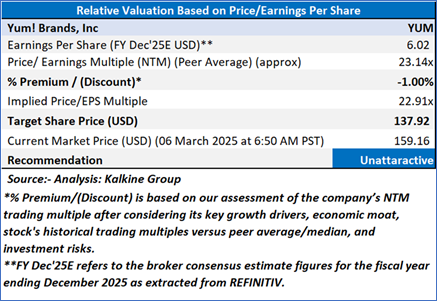

Given its current trading levels, downside indicated by valuation, and risks associated, it is prudent to book profit at the current levels. Hence, a ‘Unattractive’ recommendation is given on the YUM at the current market price of USD 159.16, as of 06 March 2025 at 6:50 AM PST.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical issues prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is neither an indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is March 06, 2025 at 06:50 AM PST. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Please wait processing your request...

Please wait processing your request...