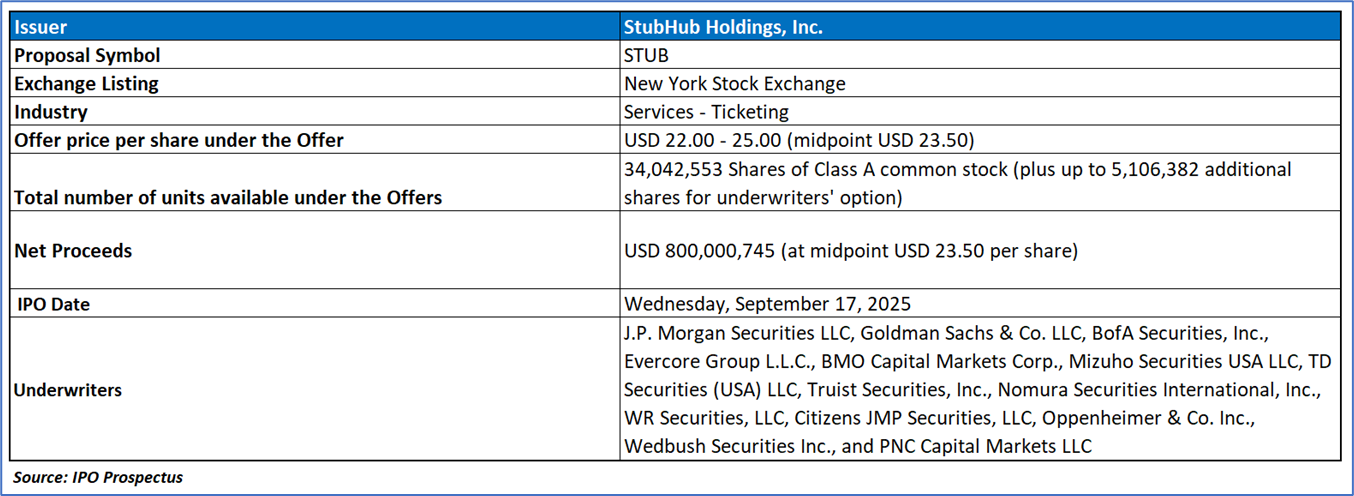

The Offer

Company Overview

StubHub Holdings, Inc. (STUB) is a leading global online ticket marketplace specializing in connecting buyers and sellers of event tickets, offering a secure, user-friendly platform with advanced fraud detection and customer support. The company distinguishes itself as an innovator in the ticketing industry by providing tailored ticket purchasing options and comprehensive support to enhance buyer-seller interactions, leveraging its extensive network and industry expertise, which has earned recognition such as the "Global Innovation in Ticketing Award" in 2023. Beyond ticketing, StubHub provides consultancy services through its StubHub Solutions division, assisting corporate clients with event management and sponsorship options using the same experienced team, targeting past customers and new referrals from entertainment and sports networks, while actively promoting its services at industry conferences to attract new clientele.

Key Highlights

Primary Offering:

Primary offering of 34,042,553 shares of Class A common stock at an assumed offering price of USD 23.50 per share (midpoint of the price range of USD 22.00 to USD 25.00), resulting in gross proceeds of USD 800 million, while net proceeds are estimated at USD 750 million after deducting underwriting discounts and estimated offering expenses. Should the underwriters fully exercise their over-allotment option, gross proceeds would increase to USD 920 million.

Use of proceeds:

StubHub Holdings expects to raise approximately USD 750 million from its IPO, assuming full exercise of the over-allotment option at USD 23.50 per share. Around 80% of proceeds will be used to repay debt, 15% will support international expansion in Europe and Asia, and 5% will be allocated to working capital and general corporate needs. While no acquisitions have been identified, the company emphasizes financial flexibility and intends to invest any unused funds in short-term, interest-bearing instruments to maintain liquidity and support long-term growth.

Industry Overview and Analysis

- Expanding Global Market with Strong Growth Potential: The live events industry reached approximately USD 140 billion in gross transaction value (GTV) in 2023 and is projected to exceed USD 240 billion by 2028 at an 11% CAGR. Within this, the secondary ticketing market—StubHub’s primary domain—accounted for USD 28–35 billion in 2023 and is expected to grow faster than primary ticketing, potentially reaching USD 50–60 billion by 2028. Rising demand for experiential entertainment and fan-to-fan resale flexibility underpin this growth trajectory.

- Key Industry Shifts Driving Transformation: The sector is undergoing rapid digital adoption, with over 70% of ticket sales made via mobile platforms enhanced by AI-driven personalization and fraud prevention tools. Blockchain and NFTs are emerging for ticket authenticity, while regulatory scrutiny around fees and anti-scalping creates both compliance challenges and differentiation opportunities. Additionally, global expansion is accelerating, particularly in Europe and Asia-Pacific, supported by rising disposable incomes and high-profile international events. Sustainability and inclusiveness are also shaping consumer expectations, influencing ticketing platforms’ strategies.

- StubHub’s Competitive Positioning and Strategic Outlook: The industry remains fragmented, with Ticketmaster dominating primary ticketing, while StubHub leads in secondary markets with ~25% share across 195 countries. Its fan-focused platform, neutral marketplace model, and technological capabilities create entry barriers against smaller rivals. Growth opportunities lie in emerging markets, integrated resale partnerships, and data-driven upselling, though risks from regulatory shifts, economic downturns, and fee pressures persist. StubHub’s positioning suggests resilience and potential for sustained growth, supported by innovation, strategic flexibility, and consolidation opportunities.

Financial Highlights (Results of Operations) (Expressed in USD)

- Strong Revenue Growth and Market Momentum: StubHub demonstrated resilient top-line performance, with GTV rising 13.5% YoY to USD 4.2 billion in 2024 and net revenue increasing ~14% to ~USD 375 million. Growth was fueled by strong global demand for live events and network effects within its secondary marketplace. This momentum aligns with broader market expansion, positioning StubHub to capture additional market share post-IPO, particularly in Europe and Asia.

- Improving Profitability but Persistent Net Losses: The company narrowed its net loss from USD 65 million in 2023 to USD 45 million in 2024, while adjusted EBITDA turned positive at ~USD 22 million. Operational efficiencies and platform scalability drove this improvement, though fixed costs remain high. Progress toward profitability enhances investor confidence, with potential net income break-even by 2026 if revenue growth sustains above 15% annually.

- IPO Proceeds Target Debt Reduction and Balance Sheet Strengthening: StubHub carries a heavy debt load of ~USD 900 million, contributing to high interest expenses. The IPO, expected to raise ~USD 750 million net, will primarily be used to repay ~80% of this debt, materially reducing leverage and interest burden. Post-IPO, equity is projected to rise from ~USD 250 million to ~USD 1 billion, cutting the debt-to-equity ratio from above 1.5x to below 0.2x, thus enhancing financial resilience.

- High Margins and Strategic Outlook: With gross margins near 85% and customer retention at 70%, StubHub benefits from an asset-light, scalable model that supports rapid operating leverage. The IPO marks a reset for long-term growth, providing capital for international expansion and reinforcing its leadership in the USD 140+ billion live events market. While economic sensitivity and regulatory risks persist, strong fundamentals, high margins, and deleveraging efforts position StubHub for sustainable value creation.

Risk Associated (High)

Investment in the IPO of “STUB” is exposed to a variety of risks such as:

- Dependence on Event Supply and Economic Sensitivity: StubHub's revenue relies heavily on the volume and frequency of live events (e.g., concerts, sports), which can be disrupted by external factors such as economic downturns, health crises, or cancellations. With gross transaction value (GTV) at USD 4.2 billion in 2024 and a projected market sensitivity reducing GTV by 15-20% in a recession, any decline in consumer spending or event scheduling could significantly impact net revenue (USD 350-400 million) and exacerbate existing losses (USD 45 million in 2024).

- High Leverage and Post-IPO Execution Risk: Prior to the IPO, StubHub carries USD 900 million in debt against USD 120 million in cash, creating a leveraged balance sheet. While the IPO aims to reduce debt by ~80% with USD 750 million in net proceeds, failure to execute this deleveraging (e.g., due to market pricing below the USD 22-25 range or underwriter option not exercised) could maintain high interest burdens, straining cash flows and delaying growth investments in international markets or technology.

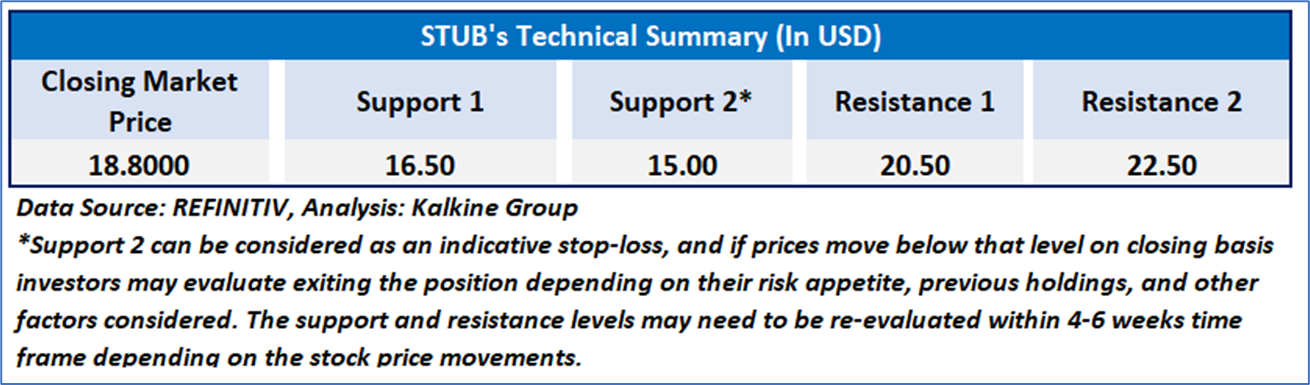

Technical Chart & Table:

Stock Recommendation

StubHub Holdings, Inc. (STUB) boasts a robust position in the growing secondary ticketing market, with a 2024 gross transaction value of USD 4.2 billion reflecting a 13.5% year-over-year increase driven by heightened live event demand. The company's asset-light marketplace model delivers an impressive 85% gross margin, supported by a 70% customer retention rate, showcasing strong operational efficiency and brand loyalty. Post-IPO, with USD 750 million in net proceeds aimed at reducing debt by 80%, StubHub is poised to strengthen its balance sheet and pursue international expansion, enhancing long-term growth potential in a projected USD 240 billion industry by 2028.

As per the above-mentioned price action, after IPO trading levels, momentum in the stock over the last month, and technical indicators analysis, a ‘Buy’ rating has been given for StubHub Holdings, Inc. (NYSE: STUB) at the closing price of USD 18.80, as of September 23, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is September 23, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided have been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...