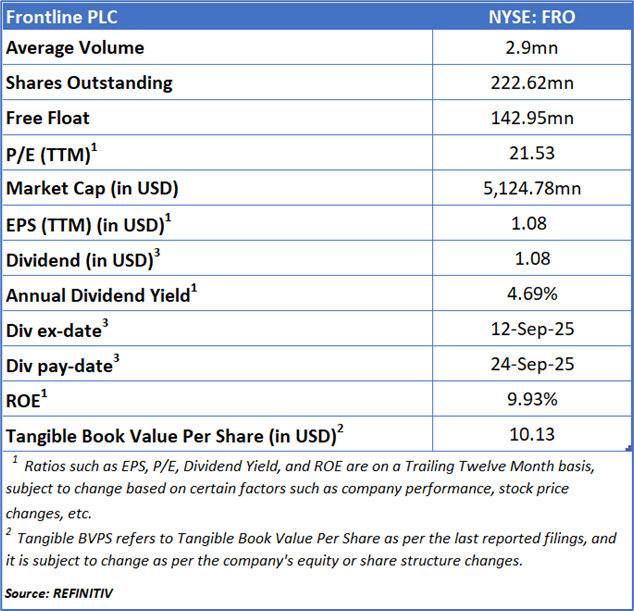

Frontline PLC.

Frontline PLC (NYSE: FRO), based in Cyprus, is a global transportation company focused on the maritime shipment of crude oil and refined petroleum products. It operates an international fleet of VLCCs, Suezmax, and LR2/Aframax tankers, which are primarily deployed for seaborne transport of oil and related cargo along major global trade routes.

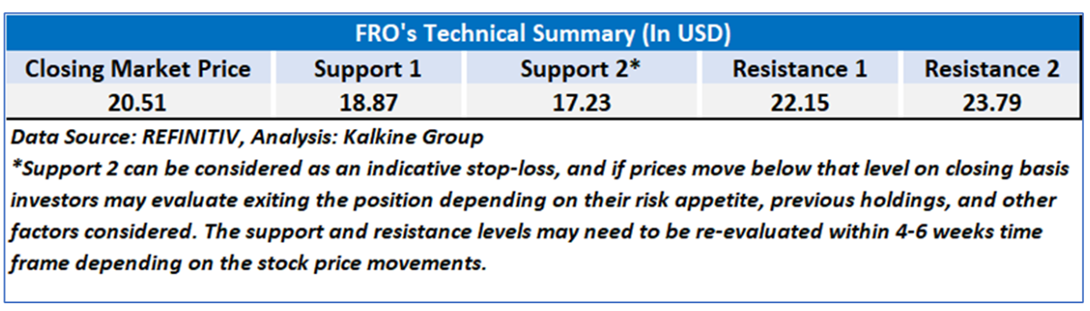

As per previous Kalkine’s Dividend Income Report published on ‘FRO’ on August 06, 2025, Kalkine provided an ‘Buy’ stance on the stock at USD 20.51 based on fundamental analysis and the stock price has now moved up by ~ 13.46% since then and has breached resistance level 1.

Noted below are the details of support and resistance levels provided in our previous report:

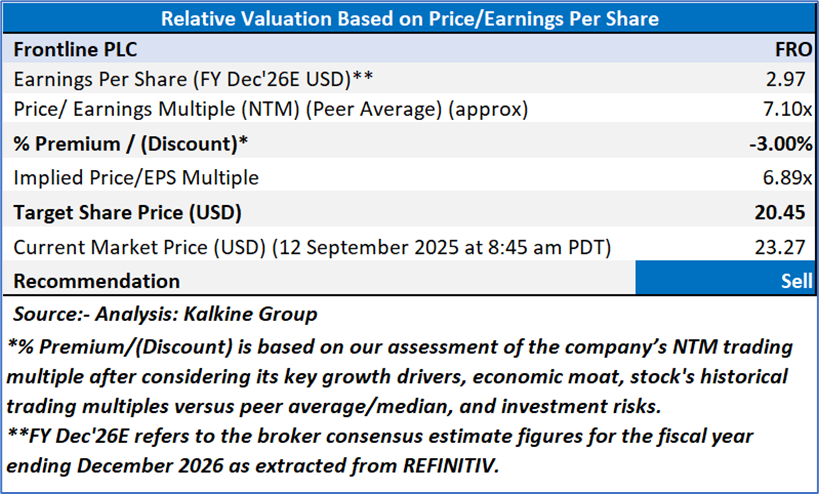

Rationale – Sell at USD 23.27

- High Debt Burden and Financing Risks: Frontline remains highly leveraged, with long-term debt standing at USD 3.27 billion as of June 30, 2025. Although the company refinanced USD 1.29 billion in April 2025 to extend maturities, the large debt load continues to weigh on financial flexibility. High interest expenses, adjusted at USD 56.4 million in Q2FY25, also reduce profitability and increase sensitivity to rising interest rates or tightening credit conditions.

- Volatile Earnings from Market Exposures: The company’s reliance on spot market exposure exposes it to earnings volatility. For Q3FY25, contracted time charter equivalent (TCE) rates have already declined compared to Q2, particularly for VLCCs at USD 38,700/day versus USD 43,100/day previously. This dependency on unpredictable market rates creates uncertainty in cash flows, which could weaken financial performance if market conditions deteriorate.

- Derivative and Option Losses: Earnings were negatively impacted by non-operational financial items. In Q2FY25, the company recorded USD 3.6 million in unrealized losses on derivatives and USD 1.7 million in synthetic option revaluation losses. While adjusted figures exclude these, recurring derivative losses reflect hedging inefficiencies and expose shareholders to earnings distortions.

- Asset Base and Fleet Concentration Risks: Despite having one of the youngest fleets in the industry, Frontline’s business remains heavily concentrated in crude and product tankers. A downturn in global oil demand, OPEC production policies, or sanctions-related trade shifts could significantly reduce fleet utilization. Furthermore, vessel values are subject to market cycles, and any decline in asset prices could negatively impact the balance sheet and restrict financing opportunities.

Valuation (Using Price/Earnings Value Multiple)

Share Price Chart

Conclusion

Frontline’s financial profile carries notable risks, as the company remains highly leveraged with long-term debt exceeding USD 3.2 billion, leading to heavy interest expenses that erode profitability. Its reliance on spot market exposure further adds volatility, with Q3 contracted TCE rates already trending below Q2 levels, creating uncertainty in earnings and cash flow stability. Additionally, recurring losses from derivatives and option revaluations highlight financial inefficiencies, while the fleet’s heavy dependence on crude and product tankers leaves it vulnerable to oil demand shifts, OPEC policies, and sanctions-related trade disruptions.

Based on the notional gains, valuation downside and price action stance, a "Sell" recommendation on Frontline PLC (NYSE: FRO) has been given at the current market price of USD 23.27 as on 12 September 2025 at 8:45 am PDT.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is 12 September 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...