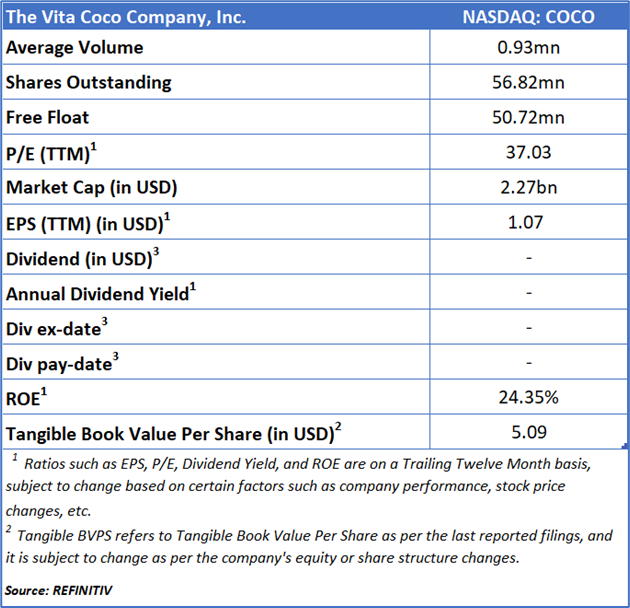

The Vita Coco Company, Inc

The Vita Coco Company, Inc. (NASDAQ: COCO) functions as a platform for functional beverage brands. Its portfolio features Vita Coco, a prominent coconut water brand; Ever & Ever, a sustainably packaged water offering; and PWR LIFT, a protein-infused water.

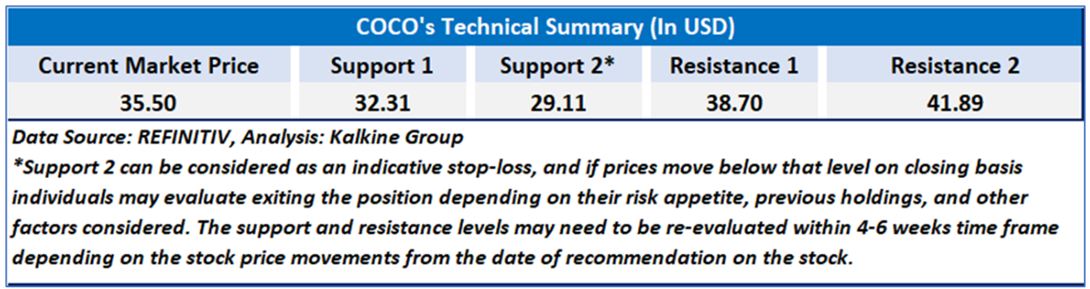

As per previous Kalkine’s Diversified Opportunities Report published on ‘COCO’ on August 21, 2025, Kalkine provided an ‘Buy’ stance on the stock at USD 35.50 based on fundamental analysis and the stock price has now moved up by ~ 18.93% since then and has breached resistance level 2.

Noted below are the details of support and resistance levels provided in our previous report:

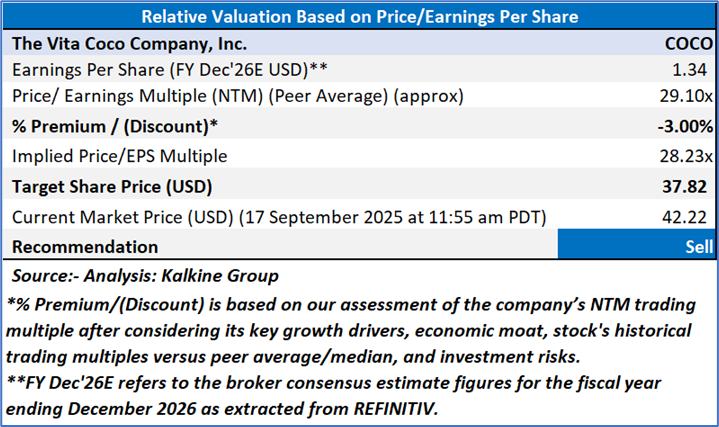

Rationale – Sell at USD 42.22

- Margin Pressure from Rising Costs: Despite revenue growth, Vita Coco faced a notable decline in gross margins, which dropped to 36% from 41% in the prior year. This erosion was largely attributed to elevated ocean freight rates, higher finished goods costs, and the imposition of a 10% baseline tariff. These inflationary cost pressures outweighed pricing actions and favorable product mix, thereby constraining profitability. The margin deterioration raises concerns about the company’s ability to sustain earnings momentum in the face of external cost headwinds.

- Increased Operating Expenses: Selling, general, and administrative (SG&A) expenses climbed significantly to USD 36 million in the quarter, up from USD 29 million last year. This rise stemmed from higher marketing investments, personnel-related costs, increased reserves for bad debt, and overlapping rent expenses due to office relocation. The sharp increase in overhead contributed to a decline in adjusted EBITDA, which fell to USD 29.2 million from USD 32.2 million, signaling weaker operating leverage despite strong top-line growth.

- Volatility in Private Label Business: The company’s private label segment experienced considerable weakness, with sales dropping 37% in the Americas. This decline reflected the loss of key contracts and highlighted the volatility inherent in this business line. While Vita Coco remains competitive in bidding for new opportunities and has secured additional business expected to benefit 2026, near-term revenue stability in private label remains uncertain. The segment’s unpredictability adds another layer of risk to the company’s overall performance.

- Exposure to Tariff and Freight Uncertainty: Vita Coco’s reliance on international sourcing exposes it to geopolitical and trade risks. While the company has factored a 10% tariff into its guidance, potential increases—such as the proposed 19% tariff on Philippine imports—pose further downside risks to margins. Coupled with unpredictable ocean freight volatility, which continues to affect near-term cost structures, Vita Coco’s profitability remains vulnerable to external supply chain pressures.

Valuation (Using Price/Earnings Value Multiple)

Share Price Chart

Conclusion

Vita Coco’s performance, while strong on the top line, is tempered by notable headwinds including margin compression from elevated freight costs, higher product expenses, and tariff exposure. Operating costs have risen sharply due to increased marketing spend, personnel expenses, and bad debt reserves, leading to a decline in adjusted EBITDA despite revenue growth. Additionally, the volatility and contraction in its private label segment, coupled with uncertainty around future tariff hikes, underscore potential risks to profitability and earnings stability.

Based on the notional gains, valuation downside and price action stance, a "Sell" recommendation on The Vita Coco Company, Inc. (NASDAQ: COCO) has been given at the current market price of USD 42.22 as on 17 September 2025 at 11:50 am PDT.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is 17 September 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...