Zymeworks Inc

Zymeworks Inc (NASDAQ: ZYME) is a global, clinical-stage biotechnology company focused on advancing a broad portfolio of multifunctional biotherapeutics aimed at improving treatment outcomes for challenging conditions, including cancer, autoimmune disorders, and inflammatory diseases.

Key Growth Aspects

- Strengthening Clinical Pipeline and Platform Validation: Zymeworks demonstrated substantial clinical progress during the quarter, reinforcing the strength of its ADC platform. Early Phase 1 data from ZW191 showed strong objective response rates, particularly in gynecological cancers, and a favorable safety profile, validating the company’s next-generation ADC design and offering meaningful differentiation in a competitive oncology landscape. This early validation increases confidence in downstream programs that leverage the same platform. Additionally, the initiation of the ZW251 Phase 1 trial marks continued momentum across its wholly-owned pipeline. Entry into clinical development for a GPC3-targeting ADC in hepatocellular carcinoma positions the company well within a high-need therapeutic area. These developments collectively underscore Zymeworks’ ability to translate research into early clinical impact while expanding therapeutic reach.

- Robust Partnership Model and Improving Financial Performance: The company’s partnership-driven model continued to generate significant financial value, including a substantial USD 25.0 million milestone from Johnson & Johnson and ongoing royalty contributions from Jazz and BeOne Medicines. These diversified revenue sources reduce operational risk, reinforce capital efficiency, and create future pathways for durable royalty streams. Upcoming Phase 3 data from zanidatamab further enhances milestone visibility and could unlock substantial long-term value. Financially, Zymeworks reported a strong top-line increase driven by milestone payments, contributing to a meaningful reduction in net loss year-over-year. With nearly USD 300 million in cash resources and expected milestone inflows, the company maintains a healthy liquidity position, supporting a projected cash runway into 2H-2027 while preserving flexibility for strategic investments.

- Proactive Capital Allocation and Leadership Strengthening: The company continued executing its strategic share repurchase program, completing USD 22.7 million in buybacks, reflecting management’s confidence in long-term prospects and providing immediate shareholder value through reduced share count. These repurchases were funded through non-dilutive milestone and royalty streams, demonstrating disciplined financial stewardship.

Zymeworks also enhanced organizational depth with the appointment of an Acting Chief Development Officer and a refreshed board that brings expertise in development strategy and capital allocation. This strengthened executive and governance structure supports disciplined execution as the company advances its clinical pipeline and partnership strategy.

Growth Challenges

- Continued Operating Losses and Declining Cash Balance: Despite higher revenues, Zymeworks continues to operate at a net loss, recording a USD 19.6 million deficit for the quarter. While improved from the prior-year period, sustained losses highlight continued dependence on milestone-driven revenue rather than recurring product income. This dynamic underscores the need for successful clinical outcomes and commercialization by partners to sustain financial momentum. Moreover, cash resources declined to USD 299.4 million as of September 30, 2025, from USD 324.2 million at year-end 2024. Although adequately capitalized, the reduction reflects ongoing R&D burn and the need to carefully balance program advancement with long-term liquidity management.

- Slower Progress in Certain Internal R&D Programs: While some programs advanced, R&D expenses decreased partly due to reduced spending on several internal assets, including ZW220, ZW251, and zanidatamab zovodotin. This shift may indicate delays, deprioritization, or slower progress across portions of the pipeline. Such variability creates uncertainty in timelines for program advancement and may limit near-term catalysts outside of partnered assets. Furthermore, increased preclinical investments in newer programs may extend the timeline before these projects generate clinical readouts or partnership opportunities. This could dilute investor visibility into future wholly-owned value creation, particularly as the company focuses on a partnership-centric model.

- Dependence on Partner Performance and External Milestones: Zymeworks’ revenue structure remains heavily reliant on milestone payments and royalties from partner-led programs. While this strategy supports capital efficiency, it also limits the company’s direct control over development timelines, trial execution, and commercialization outcomes. Any delays or prioritization shifts by partners could directly impact near-term revenue and long-term royalty streams.

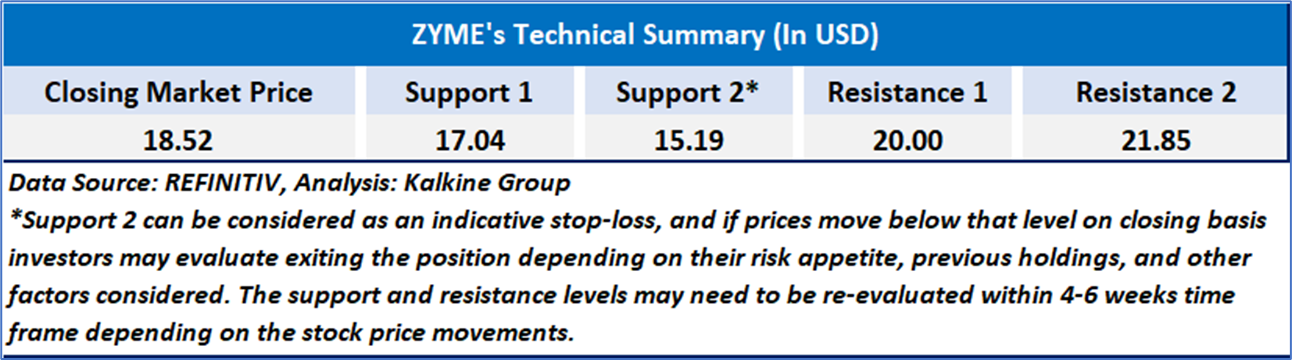

Technical Observation (on the daily chart):

Zymeworks’ stock remains in a steady uptrend, with the recent pullback finding firm support at the 50-day moving average before rebounding above the 20-day line. Momentum is neutral around the RSI 50 level, leaving room for further upside if buying strength continues. Rising volume on the latest bounce indicates renewed accumulation, and a move above the USD 19.50–USD 20 resistance zone could resume the upward trajectory, while a drop below USD 17.04 would temper the bullish outlook.

Zymeworks delivered a quarter marked by meaningful clinical and financial progress, including strong early data from ZW191, initiation of the ZW251 Phase 1 trial, and a significant milestone payment from Johnson & Johnson, all of which reinforce the strength of its ADC platform and partnership-driven model. However, the company continues to operate at a net loss, maintains a declining cash balance, and remains reliant on partner-led milestones and trial execution for revenue visibility, creating inherent variability in future performance. Overall, the outlook reflects a balanced mix of advancing clinical momentum and strategic execution, tempered by financial dependence on external collaborators and ongoing R&D expenditure.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Speculative Buy ’ rating has been given Zymeworks Inc (NASDAQ: ZYME) at the closing market price of USD 18.52 as of Nov 14,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is November 14,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...