Halma PLC (LSE: HLMA)

Halma PLC (LSE: HLMA) is an FTSE 100 index listed life-saving technology company operating through three segments. The Safety segment, the Environmental & Analysis Segment, and the medical segment. This Report covers the Key Recommendation Rationale, Conclusion, and Recommendation on the stock.

On 12 June 2025, HLMA will release FY25 results for the year ending 31 March 2025.

Key Recommendation Rationale – Sell at GBX 2,856.00

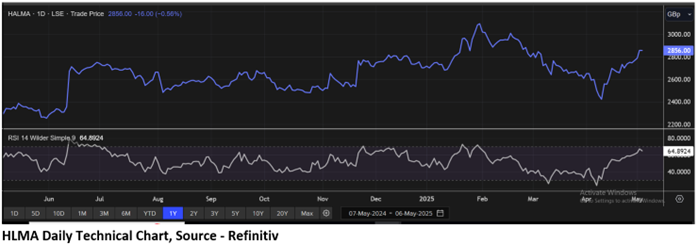

- Resistance near Current levels: HLMA’s stock price has approached Resistance (R1) which was stated in the previous report on 01 April 2025 therefore, there can be a possibility of a decline from resistance levels. Considering the market conditions and the price action, it is prudent to exit the stock.

- Currency Translation Impact on Financial Performance: Despite the strong progress in the Group's organic revenue growth and margin performance, the appreciation of Sterling poses a significant risk to the Group's financial results. The negative currency translation effect could potentially erode the benefits from the Group's solid performance in international markets, reducing the overall profitability when converted to Sterling. This currency risk remains an ongoing challenge, particularly in a fluctuating economic environment.

- Potential Over-Reliance on Acquisitions for Growth: While the Group's acquisition strategy has led to notable expansion, with seven acquisitions in the year to date, there is a concern that over-reliance on acquisitions could mask underlying organic growth challenges. If these acquisitions fail to integrate smoothly or generate the anticipated synergies, it could impact the long-term sustainability of growth and place undue pressure on the Group's financial health. The emphasis on acquisitions raises questions about the stability of organic performance in the absence of external growth drivers.

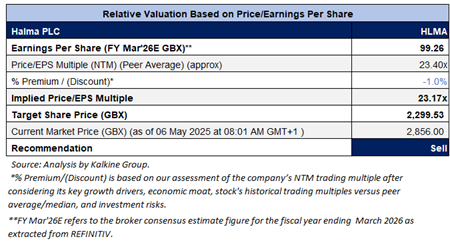

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

Conclusion

HLMA is expected to trade at a discount, considering the US Recession fears and Currency Translation Impact on Financial Performance. For conducting the valuation, the following peers have been considered Spirax Group PLC (LSE: SPX), Smiths Group PLC (LSE: SMIN) and Rotork PLC (LSE: ROR).

Given its current trading levels, Potential Over-Reliance on Acquisitions for Growth, recent rally in the share price, relative valuation, and associated risks, it is prudent to exit the stock at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the current Market Price of GBX 2,856.00 as of 06 May 2025 at 08:01 AM GMT+1.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 06 May 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...