I. Sector Landscape and Outlook

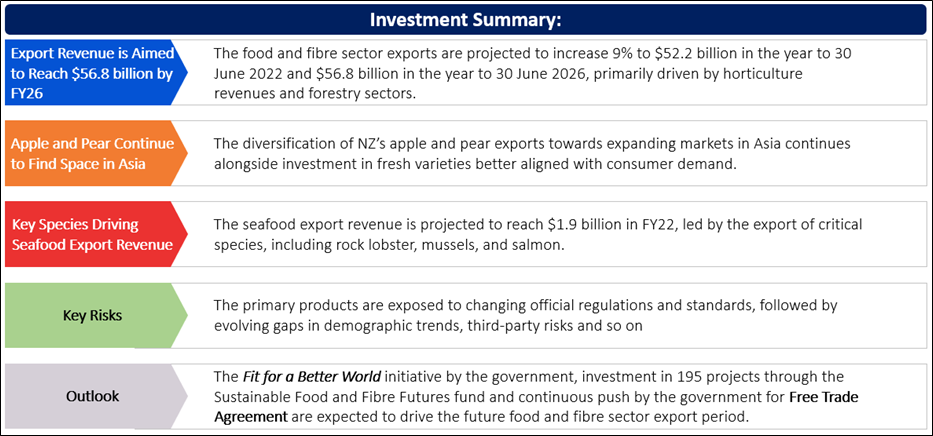

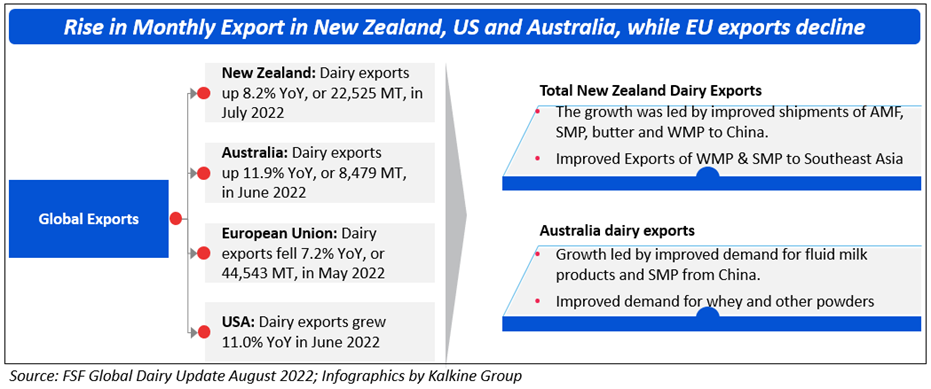

As per the Ministry for Primary Industries (MPI), the dairy export revenue is forecasted to rise by 13% to reach $21.6 billion in the year to 30 June 2022, primarily led by a reduced supply from other exporting regions and stable demand for NZ dairy. The horticulture export revenue is forecasted to rise 2% to $6.7 billion during the same period, mainly led by large kiwifruit crops and improved export prices for wine. However, adverse climatic conditions have disrupted the production of apples and pears and several vegetable crops. Meanwhile, seafood export revenue is forecasted to rise by 9% to reach $1.9 billion for the same period, primarily due to the reopening of food services and demand rebounding.

Exhibit 1: Rise in NZ Dairy Export in July 2022 Over Corresponding Period Last Year

Apple and Pear Continue to Find Space in Asia

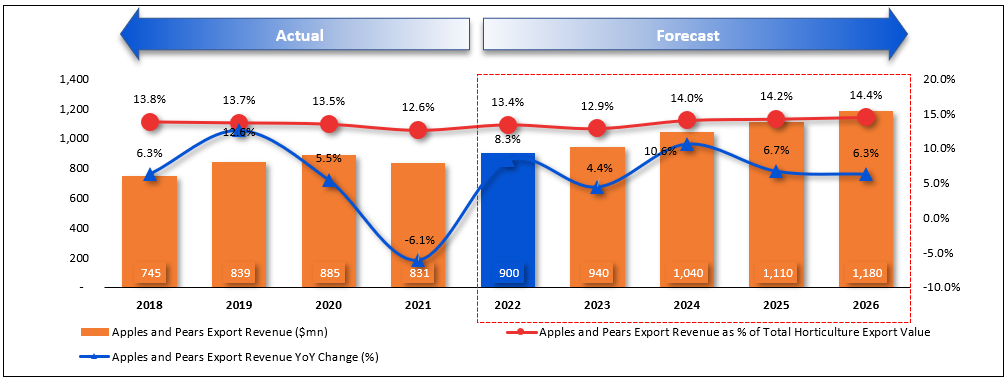

As per MPI, the Nelson-Tasman region had an improved apple crop, primarily driven by better sunshine days, despite disruptive climate conditions at the start and end of the season in Hawke’s Bay. In the forecasted period, the annual export volumes are projected to grow steadily. Further, the diversification of New Zealand’s apple and pear exports towards expanding markets in Asia continues alongside investment in new varieties better aligned with consumer demand.

Exhibit 2: Trend in Apples and pears Export Revenue 2018–26 (Year to 30 June, NZ$ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Key Species Driving Seafood Export Revenue

As per MPI, the seafood sector is driven by improved export growth in recent years, with export revenue projected to reach $1.9 billion for FY22, led by the export of critical species, including rock lobster, mussels, and salmon. The fundamental headwinds for the sector are rising production costs that pressure profitability. The revival in prices of wild capture to an average of $6.53 per kilogram and the rise in aquaculture prices to $11.53 per kilogram are projected to drive the sector further.

Exhibit 3: NZ’s Top 10 Seafood Export Destinations (Year to 31 March 2022, NZ$ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 1-year return of ~-0.79% versus ~-14.43% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~13.64% in 1-year.

Exhibit 4: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

Source: REFINITIV, Chart Created by Kalkine

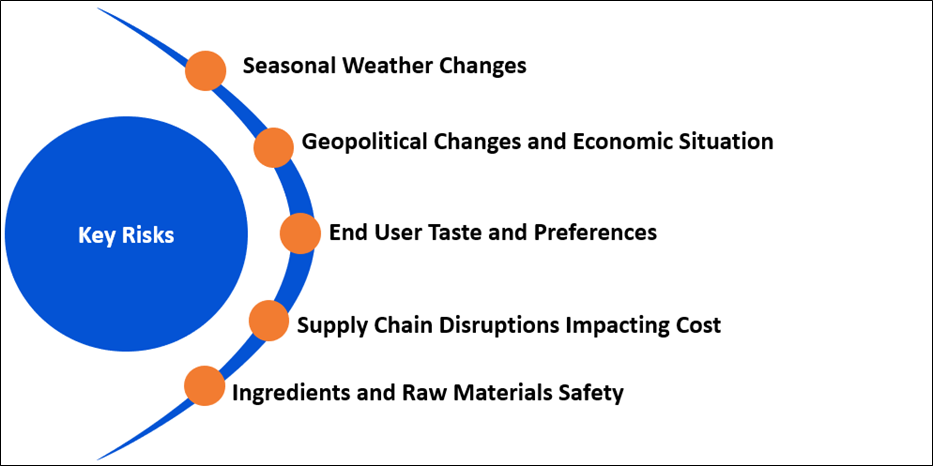

Key Risks and Challenges:

Farmers, growers, and fishers have been facing disruptions caused by climate change in the past two years in producing and delivering food and fibre products to their customers. Further, the shipping delays increased warehousing and logistics costs for the product, thereby impacting product margins without adding any value. Meanwhile, the vital parts of food ecosystems are becoming more capital-intensive, vertically integrated and concentrated in fewer hands. Also, crises and natural disasters are growing in number and intensity.

Exhibit 5. Key Risks in Consumer Staples Sector:

Source: Analysis by Kalkine Group

Outlook:

As per the 'Fortnightly Economic Update' by The Treasury', the goods exports values increased 3.3% MoM in July 2022 on an adjusted basis, driven by improved dairy and meat volumes, up 12.4% MoM and 12.7% MoM, respectively. Imports value grew 3.0% MoM in July 2022, and the annual trade deficit widened further to a new high of $11.6 billion. As per the report, the dairy prices decreased a further 2.9% at the GlobalDairyTrade auction on 16 August 2022, resulting in a total fall since March to 29%. Dairy prices are projected to remain under pressure due to softer global prospects, mainly in China, which would weigh on export returns over the year's second half. Meanwhile, the government is focused on 195 projects through the Sustainable Food and Fibre Futures fund to deliver outcomes. Trade partnerships like the historic FTA with the United Kingdom in March 2022 are expected to drive further growth and savings for exporters, driven by innovating and adapting to changing markets.

Apart from the sector-specific factors, an analysis on four NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

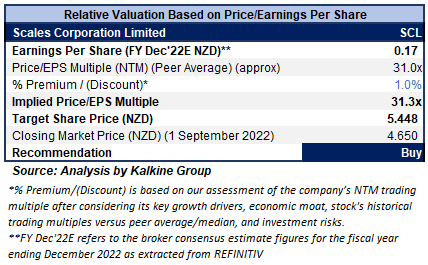

1) Scales Corporation Limited (Recommendation: Buy, Potential Upside: Low Double-Digit (M-Cap: NZD663.66 million, Annual Dividend Yield (TTM)1: 5.58%)

Business Description:

Scales Corporation Limited (NZX: SCL) is engaged in the agri-business. It operates in three divisions that include horticulture, logistics, and food ingredients, in adjacent primary sectors.

Outlook:

The company anticipates Underlying Net Profit Attributable to Shareholders at the upper end of NZD23.5-28.5 million. Due to a favourable change in earnings mix, the implied Underlying Net Profit range has grown to NZD35-43 million and the Underlying EBITDA range between NZD65-75 million. Meanwhile, the company continues to investigate offshore opportunities to grow the global proteins division.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

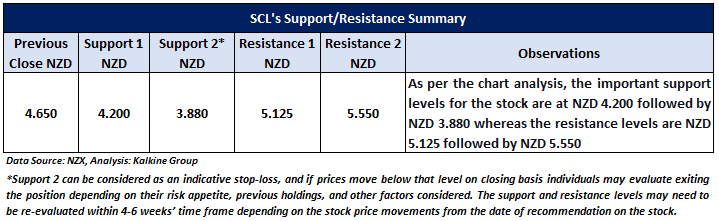

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering the financial rebound in 1H’FY22 and the positive outlook.

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD4.65 per share, down 1.69% as of 1 September 2022.

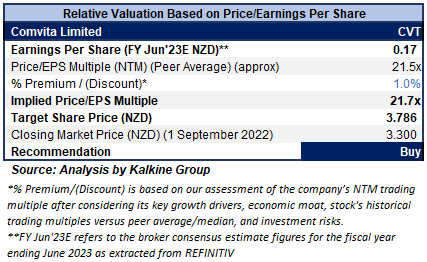

2) Comvita Limited (Recommendation: Buy, Potential Upside: Low Double-Digit (M-Cap: NZD230.11 million, Annual Dividend Yield (TTM)1: 2.28%)

Business Description:

Comvita Limited (NZX: CVT) is one of the leading global players in producing Manuka honey. The company has a decent geographical presence across Australia, New Zealand, China, and North America, among others.

Outlook:

Comvita anticipates double-digit earnings growth in FY23, driven by the momentum in the second half. Ecommerce sales are expected to be over 40% and are targeted to increase further 100 bps in gross margin and marketing. Transformation investment is projected to increase to NZD5.5 million. The 2025 plan is to focus on GP of at ~60%, creating brand value by investing 15% in Brand building activity and achieving a 20% EBITDA margin.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

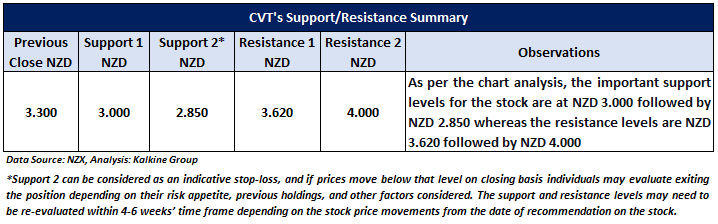

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering its record e-commerce sales in FY22 and decent outlook for FY23.

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD3.30 per share, down 1.49% as of 1 September 2022.

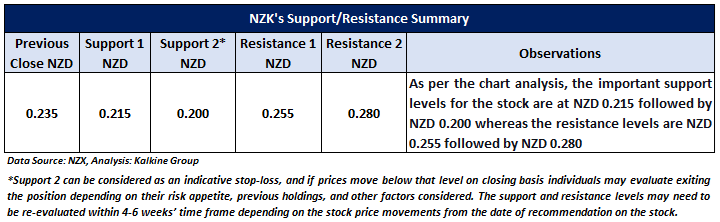

3) New Zealand King Salmon Investments Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit (M-Cap: NZD127.24 million)

Business Description:

New Zealand King Salmon Investments Limited (NZX: NZK) is the producer and seller of salmon fish to chefs, retailers, and wholesalers in New Zealand and overseas.

Outlook:

The company is undertaking structural changes to its farming model to prevent increasing fish mortalities, which would position it better. FY23 would be a transition year, and it projects a proforma EBITDA loss between NZD8-12 million in FY23 and sustainable earnings in a guided range of NZD15-19 million.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the facts above, a ‘Speculative Buy’ recommendation on the stock has been provided at the closing market price of NZD0.235 per share, as of 1 September 2022.

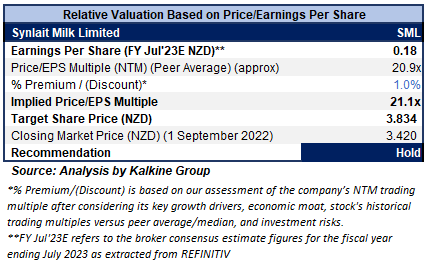

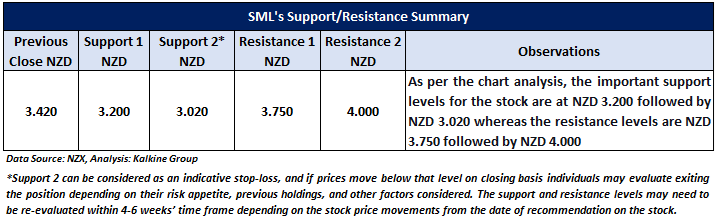

4) Synlait Milk Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZD747.55 million)

Business Description:

Synlait Milk Limited (NZX: SML) is engaged in producing a range of nutritional milk products for its global customers by combining expert farming with state-of-the-art processing.

Outlook

The company has reduced its forecast base milk price for the 2021/2022 season to $9.30/kgMS from $9.60/kgMS. Although the dairy commodity prices declined over the past two months, this milk price will be the highest ever paid by the company. Further, the company is witnessing a decent start to the 2022/2023 season as certain products were sold at historically high prices, and foreign exchange movements facilitated a robust milk price. It increased its forecast base milk price forecast for the 2022/2023 season to $9.50/kgMS from $9.00/kgMS.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/E multiple-based illustrative relative valuation, and the target price reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering its strong result performance in H1FY22 and outlook for FY22.

Considering the facts above, a ‘Hold’ recommendation on the stock has been provided at the closing market price of NZD3.42 per share, down 1.72% as of 1 September 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is September 1, 2022. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Transitional FAP license issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...