1.sector Landscape and Outlook

As per Treasury.NZ, the oil prices are cooling from their elevated level resulting in some ease to inflation. However, prompting the Reserve Bank of New Zealand to tighten policy to bring inflation to the targeted level. The core measures of inflation are anticipated to persist. Annual headline inflation is expected to be ~6.7%, a little above the median of other estimates and the Reserve Bank’s projection of 6.4%. Meanwhile, September’s Electronic Card Transactions report indicated some promising numbers as spending increased 2.5% in September 2022 and 4.0% in the September 2022 quarter, primarily driven by higher hospitality spending as international tourism returned.

Rise in Housing and Business Lending in August 2022

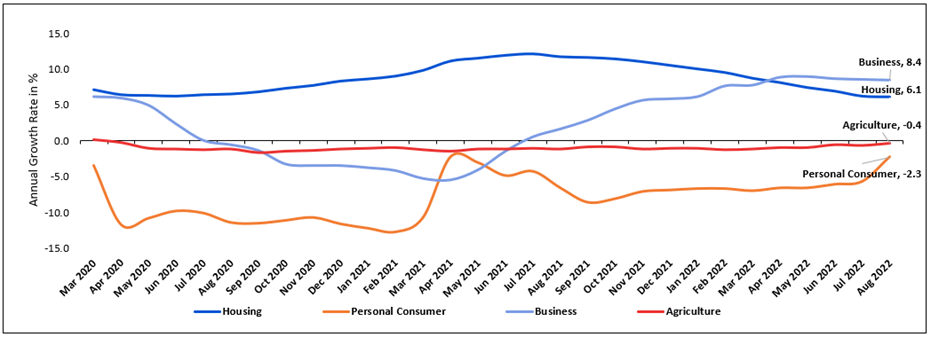

RBNZ's total housing lending stock grew by $952 million (0.3%) in August 2022, up on the $848 million (0.2%) rise reported in July 2022. However, the annual growth decreased to 6.1%, sliding further from 6.2% in July 2022, the 13th month of sluggish annual growth. Meanwhile, the total business lending stock grew by $782 million (0.6%) in August 2022, while its annual growth fell from 8.5% to 8.4%. Annual growth has decreased from its high in May 2022, with the highest annual growth rate since February 2009.

Exhibit 1: Lending Pattern Since March 2020 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Improved Asset Quality of Banks

As per RBNZ, the banks’ asset quality remains high due to positive economic momentum and lower non-performing loans and arrears. Further, the banks have continued to slash the loss provisioning and improve profitability, which facilitated banks to grow their capital positions, thereby enhancing their resilience. The regulatory bodies have increased the funding costs, passed through higher lending rates, retaining interest margins broadly at a comfortable level.

Fall in Total Funds Under Management, But Well Above the Average Number

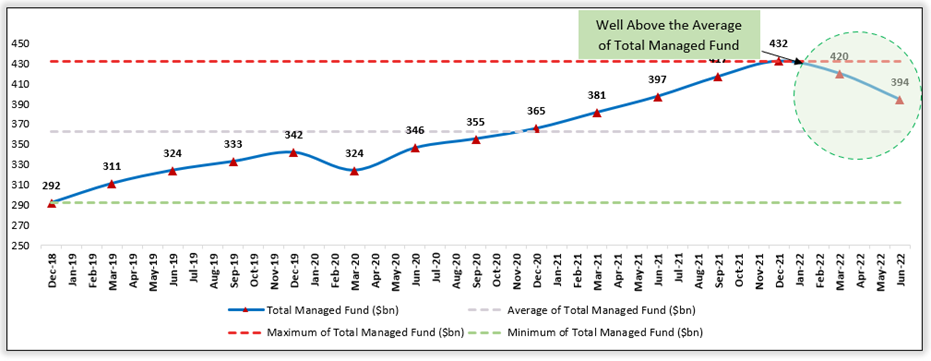

As per RBNZ, total funds under management fell by 5.6% QoQ to $243.1 billion in the June 2022 quarter, reflecting a second consecutive quarterly fall. Annually, total funds under management fell 2.2% YoY, the first yearly fall reported since March 2009. Furthermore, private Wealth fell 4.5% in June 2022 to $37.9 billion. The value of Retail Unit Trusts decreased by 7.3% in the June 2022 quarter to $51.8 billion. However, it reflected a rise since March 2021. Both Private Wealth and Retail Unit Trusts accumulated a large proportion of shares; hence the fall is in line with the fall in listed shares.

Exhibit 2: Trend in Managed Funds in NZ ($bn)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Growth in Premium Contribution Continues Despite Economic Uncertainty

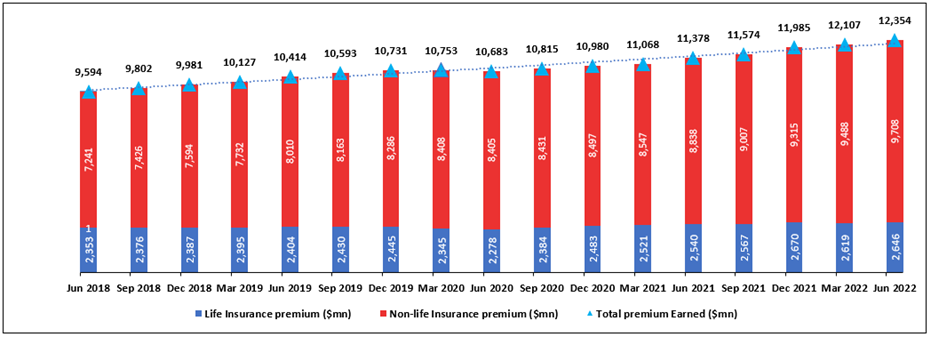

As per RBNZ, the insurers are well-placed to mitigate surprising stresses on their businesses and shield the common interests of policyholders. The NZ insurance sector remains resilient despite the multiple continuing uncertainties. The corporates continue with high-rate activities like new entry and exit, strategic mergers and acquisitions planned and executed, and sales of portions of insurers’ books.

Exhibit 3: Trend in Insurance Companies in NZ ($million)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Financials Index generated a 2-year return of ~13.88% versus ~-13.08% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~26.96% in 2-year.

Exhibit 4: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

Key Risks and Challenges:

The factors impacting the financial market are primarily driven by elevated inflation, higher interest-rate policy, a strong dollar and the disruptions caused by the Ukraine-Russia war. Meanwhile, the Monetary Policy Committee of NZ increased the Official Cash Rate (OCR) to 3% from 2.5% to fight against elevated inflation. It plans to make similar decisions to maintain price stability and sustainable employment.

Exhibit 5. Key Risks in Financial Sector:

Source: Analysis by Kalkine Group

Outlook:

The NZ financial system remains well-placed to augment the economic growth story. Banks' capital stability has grown in the past well ahead of upcoming higher capital requirements. This move has strengthened the banking sector's ability to absorb losses and continue lending during a downturn. According to 'Fortnightly Economic Update', released by 'The Treasury' on 14 October 2022, the war between Ukraine and Russia, elevated inflation and slower growth in China are expected to provide a challenging environment in future. Further, the Reserve Bank of New Zealand raised the Official Cash Rate by 50 basis points to 3.50% in the Monetary Policy Review, per market expectations. The government reported an operating (OBEGAL) deficit of $9.6 billion for 2021-22 (2.7% of GDP), approximately half the budget forecast of $19.0 billion, primarily led by stronger-than-expected tax revenue. Moreover, the net debt was 17.2% of GDP, marginally higher than the budget estimates.

Apart from the sector-specific factors, an analysis on three NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) The Bankers Investment Trust Plc (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD2.46 billion, Annual Dividend Yield (TTM)1: 2.26%)

Business Description:

The Bankers Investment Trust Plc (NZX: BIT) was incorporated in 1888. It has a globally diversified portfolio, and this Trust has sought income and capital growth for shareholders.

Outlook:

The company expects stock markets to remain volatile until inflation is under control and investors gain confidence in stock valuations. Further, the portfolio is broadly diversified by geography, sector and company to mitigate investment risk. The company has the flexibility to invest in multiple geographies and any sector with no pre-determined limits on an individual country or sector exposures. As of 18 October 2022, the unaudited net asset value per share was 104.8p, and the net asset value per share with debt marked at fair value was 104.8p.

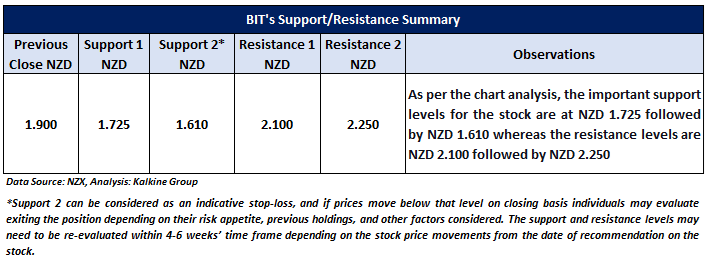

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD1.90 per share, down 1.04% as of 20 October 2022.

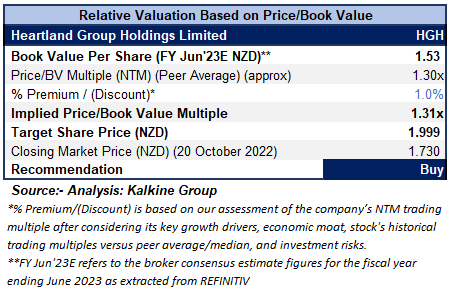

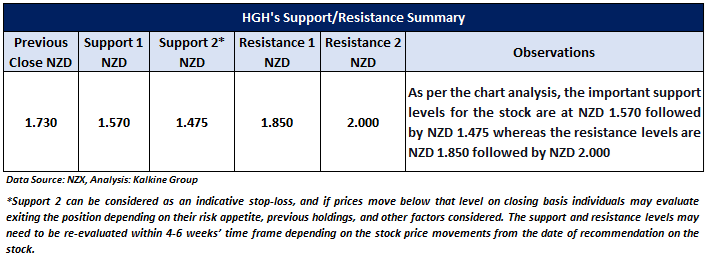

2) Heartland Group Holdings Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD1.22 billion, Annual Dividend Yield (TTM)1: 8.99%)

Business Description:

Heartland Group Holdings Limited (NZX: HGH) is a financial services group. In New Zealand, Heartland Bank Limited is a registered bank. The company provides reverse mortgage loans and funding to small business and customer lending sectors through Australian businesses.

Outlook:

As per the company, the Australian market provides decent growth prospects, with the potential addressable market for reverse mortgages estimated to be NZD10-15 billion.

On 20 October 2022, the company advised that it signed a conditional share purchase agreement to purchase Challenger Bank Limited’s shares from Challenger Limited.

On 13 October 2022, the company reaffirmed the guidance range for net profit after tax (NPAT) for FY2023 to be between $109-$114 million, excluding any impacts of fair value changes on equity investments.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/B multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/B Multiple (NTM) (Peer Average), considering its record profit in FY22, equity raising initiative to pay the debt, fund growth strategies, and decent outlook.

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD1.73 per share, up 1.76% as of 20 October 2022.

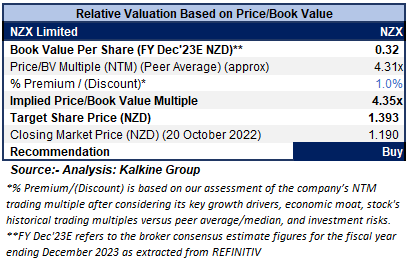

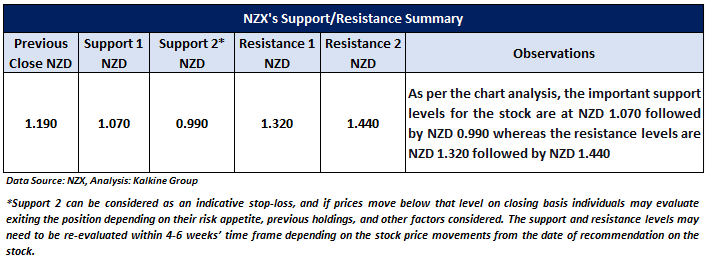

3) NZX Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD374.50 million, Gross Dividend Yield (TTM1): 7.12%)

Business Description:

NZX Limited (NZX: NZX) operates New Zealand’s equity, debt, derivatives, and energy markets. It provides clearing, trading, depository, settlement, and data services.

Outlook

The company estimates FY22 Operating Earnings (EBITDA) between $33.5-$38.0 million. The dividend policy is to pay between 80-110% of adjusted Net Profit After Tax over time. Plans to integrate ASB Superannuation Master Trust and continue hunting for a strategic acquisition, Asian Region Funds Passport obtained, drive further organic growth momentum. It will continue transitioning clients to the new platform and delivering on the FY23 target of between $35-$50 billion FUA.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Technical Overview:

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using P/B multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/B Multiple (NTM) (Peer Average), considering strategic growth investment and acquisition opportunities.

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD1.19 per share, as of 20 October 2022.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is October 20, 2022. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Transitional FAP license issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...