I. Sector Landscape and Outlook

The housing market in New Zealand remained elevated in the March quarter of 2021, but there have been few indications of cooling, as May 2021 data showed tighter-LVR requirements that are in place to ease housing risks. Meanwhile, in the release of the Government’s Public Housing Plan 2021-2024, the government plans to add 8,000 new houses in public and transitional housing places (6,000 public housing places and 2,000 transitional housing places).

Further, the government also announced a $3.8 billion fund to accelerate housing supply in the short to medium time horizon. Such moves enable more Kiwis to access First Home Grants and Loans with higher income caps and increased house price caps in targeted areas. Bright-line test has been doubled to 10 years with an exclusion to incentivize new builds. In addition, the government plans to support Kāinga Ora to borrow $2 billion extra to accelerate land acquisition to boost the housing supply.

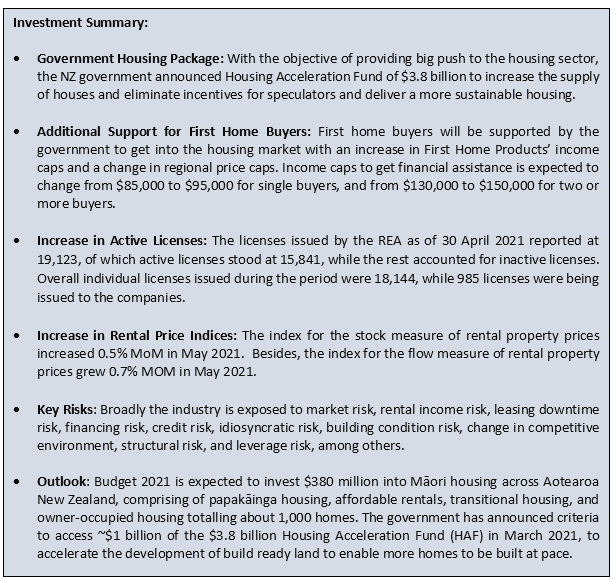

Increased Licenses in Real Estate Business, Indicating Strong Traction in the Sector

The real estate sector of New Zealand is regulated by the Real Estate Authority (REA) that provides licenses to the people as well as companies employed in the real estate industry. The licenses issued by the REA as of 30 April 2021 reported at 19,123, of which active licenses stood at 15,841, while the rest accounted for inactive licenses. Overall individual licenses issued during the period were 18,144, while 985 licenses were being issued to the companies. This indicates the overall active licenses issued by the REA continue to report a steady growth over three years.

Exhibit 1: Trend in Active Licenses by Year

Data Source: rea.govt.nz, Chart Created by Kalkine Group

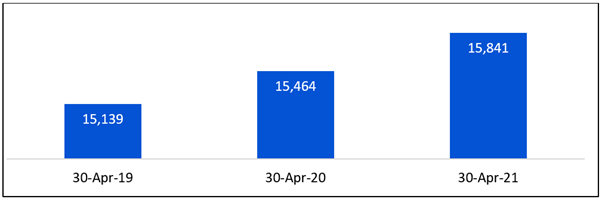

New Zealand House Prices Have Grown Significantly

As per the Reserve Bank of New Zealand, the house prices have grown significantly, mirroring the northward trend as also visible in global asset prices, driven primarily by low-interest rates but several other factors have also lifted housing demand. In addition, an improvement in the resilient labour market and the temporary removal of loan-to-value ratio (LVR) restrictions have boosted the growth. Amid low supply, construction activity has grown and is expected to remain high. With border restrictions reducing migrant inflows due to Covid-19 circumstances, the new housing supply is expected to outstrip population growth.

Exhibit 2: Value of Housing – Reporting a growth of ~75% Since March 2015 to December 2020

Data Source: rbnz.govt.nz, Chart Created by Kalkine Group

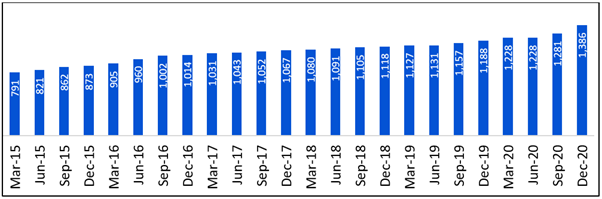

Meanwhile, bank mortgage lending has grown with the increase in house prices, mostly to investors but also to owner-occupiers. Borrowers have opted for more risk, with an increased proportion of lending at high debt-to-income (DTI) and loan-to-value ratios. For highly indebted buyers, elevated interest rates would increase debt-servicing costs phenomenally and reduce the income left for consumption.

Exhibit 3: High-Risk Shares of New Mortgage Lending by Buyer Type

Data Source: rbnz.govt.nz, Chart Created by Kalkine Group

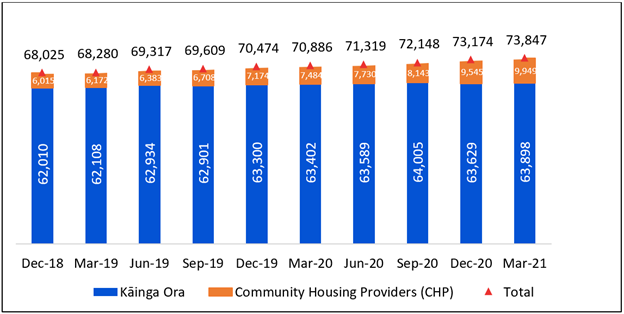

Increased Demand for Public Housing in Quarter Ending March 2021

As per the public housing quarterly report March 2021, published by the Ministry of Housing and Urban Development, the country had 73,847 public houses an increase of 673 from the previous quarter (73,174 in December 2020). Within this, 63,898 state houses were provided by Kāinga Ora, (who provide accommodation to over 180,000 people), and 9,949 community houses were provided by 59 registered Community Housing Providers across New Zealand. Community houses are homes owned, leased, or managed by non-governmental organisations (NGOs) or independent government subsidiaries. Over the March quarter of 2021, registered CHPs have grown their total tenancies by 404.

Exhibit 4: Trend in Public Houses, Tenanted by People Who are Eligible

Data Source: hud.govt.nz, Chart Created by Kalkine Group

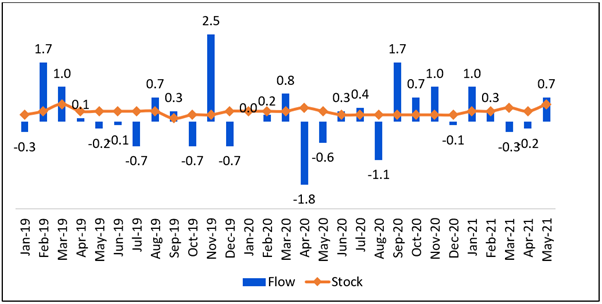

Increase in Rental Price Indexes – Changes in Prices That Households Pay for Housing Rentals

The index for the stock measure of rental property prices increased 0.5% MoM in May 2021. In line with this, the index for the flow measure of rental property prices grew 0.7% MoM in May 2021. However, stock index grew by 3.1% YOY in May 2021, and the flow index increased by 4.5% YOY in May 2021. The flow measure captures the fluctuation in rental price only for dwellings that have a new tenancy started in the reference month, as it tends to be more volatile than the stock movement. This indicates rental price changes across the whole rental population, including renters currently in tenancies.

Exhibit 5: Trend in Monthly Percent Change in Rental Price Indexes, Jan 2019–May 2021

Data Source: stats.govt.nz, Chart Created by Kalkine Group

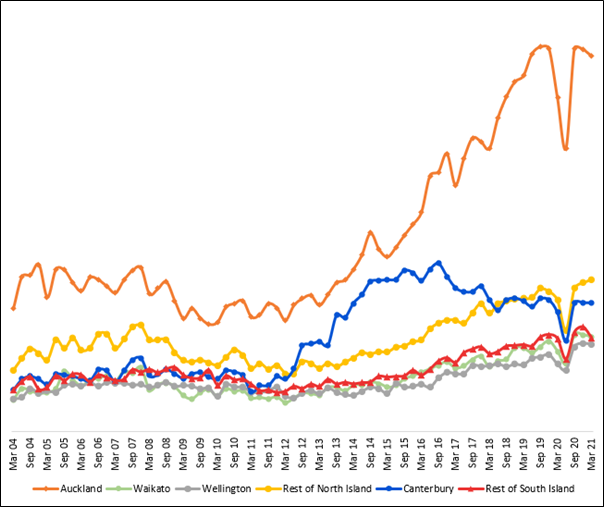

Rise in Building Value and Volume in March Quarter 2021

As per statistics estimate, total building volume increased 3.7% QOQ, where residential building work increased 4.3%, and non-residential increased 2.6%. In addition, total building value grew 13% YOY to $6.7 billion in March quarter 2021. Within this, residential building work rose 21% to $4.6 billion, while non-residential work decreased 0.6% to $2.1 billion. By region, the actual value of total building work in the March 2021 quarter over the March 2020 quarter, was Auckland (up 13% to $2.7 billion), Waikato (up 18% to $673 million), Wellington (up 29% to $621 million), Rest of North Island (up 16% to $1.1 billion), Canterbury (up 8.2% to $918 million), Rest of South Island (up 1.0% to $668 million). Meanwhile, residential construction prices have increased 1.0% in the March 2021 quarter, while non-residential prices grew 0.4%.

Exhibit 6: Total Building Work Put in Place – An Increase in Value Terms in March Quarter 2021

Data Source: stats.govt.nz, Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Real Estate (Sector) Index generated a 1-year return of ~21.30% versus ~11.75% by the S&P/NZX 50 Index. Therefore, NZX All Real Estate Index overperformed NZX50 Index by ~9.55% in 1 year.

Exhibit 7: S&P/NZX All Real Estate (Sector) vs S&P/NZX50 Index

Source: REFINITIV

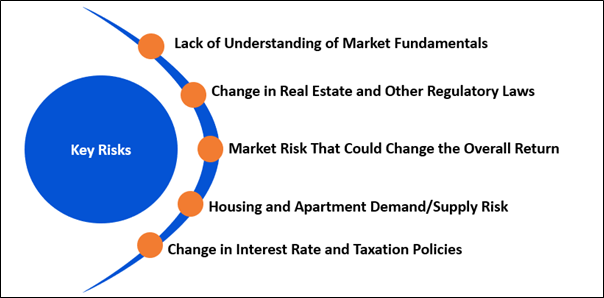

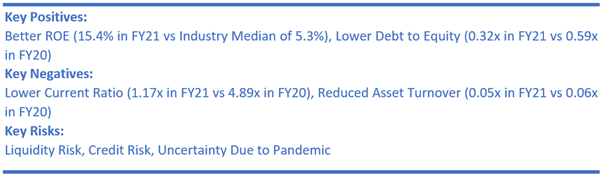

Key Risks and Challenges:

As per the Reserve Bank of New Zealand, house prices have increased phenomenally in the past 12 months. This rise has raised concerns at the Reserve Bank of New Zealand – about the risk this poses to financial stability. The reduction in borrowing rate at historic low levels has supported the economy at a crucial time of Covid-19 but also had the flow-on effect of boosting asset prices. Amid strong population growth and limited housing availability, house prices jumped from already elevated levels, and so the debt levels. This has led to a situation of vulnerabilities as some households have borrowed more than their income to buy homes at historically high prices.

People who are choosing whether to buy a property or continue renting, are the main group contributing to housing demand. If house prices continue to rise too much then the incentive to own diminishes, and prices may not be as sustainable.

Amid higher risk lending due to increasing house prices and to ensure low vulnerability in mortgage lending, the Reserve Bank has tightened loan-to-value ratio (LVR) requirements. Since 1 May 2021, a maximum of 5% of new lending to investors can be at LVRs above 60%. In addition, a maximum of 20% of new lending to owner-occupiers can be at LVRs above 80%. With these restrictions in place, new lending to investors at high LVRs is decelerating.

Exhibit 8. Key Risks in Real Estate Sector:

Sources: Analysis by Kalkine Group

Outlook:

Budget 2021 is expected to invest $380 million into Māori housing across Aotearoa New Zealand, comprising of papakāinga housing, affordable rentals, transitional housing, and owner-occupied housing totaling about 1,000 homes. In addition, improvement of quality homes for whānau with repairs for 700 Māori-owned houses, is led by Te Puni Kōkiri. Also, the government plans $30 million towards building future capability for Kiwi and Māori groups to accelerate housing projects and support services. This investment is expected to provide ~2,700 houses, assuming an average cost of $100,000 to $130,000 per site.

Meanwhile, the government has opened two new Salvation Army developments at Westgate and Flatbush, offering 68 new public housing places for Aucklanders, their whānau and tamariki. In addition, Kaitiakitanga in Flat Bush with ten one-bedroom units and 36 two-bedroom units, is expected to add 46 new public housing places in Auckland. Of this, ~85% of referrals for tenants are for households with dependent children. Te Manaaki Tāngata in Westgate has 22 new public housing places, comprised of two one-bedroom units and 20 two-bedroom units.

The government has announced criteria to access ~$1 billion of the $3.8 billion Housing Acceleration Fund (HAF) in March 2021, to accelerate the development of build ready land to enable more homes to be built at pace with scale.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Precinct Properties New Zealand Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.35 billion, Gross Dividend Yield: 4.073%)

Business Description:

Precinct Properties New Zealand Limited (NZX: PCT) is the owner and developer of inner-city business space in Auckland and Wellington.

Outlook:

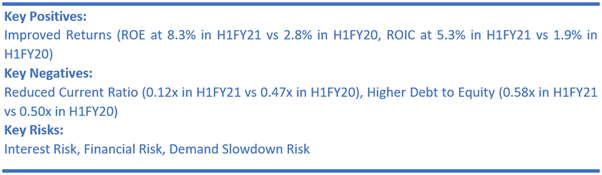

The company has completed multiple regular projects and now focuses on future projects such as Queen Street. It is also selling its non-core assets to boost its earnings profile. Meanwhile, the long-term outlook remains robust primarily driven by high occupancy levels and a 7.7-year WALT offering lower leasing costs and incentives. This is followed by, roughly 55% of the portfolio supported by structured reviews, revenue backed by the government and high-quality occupiers, low cost of debt, and low recurring CapEx requirements due to premium portfolio quality and asset age. Broadly, FY21 AFFO and dividend remain at 6.50 cps, representing a 3.2% increase to shareholders.

As per the release dated 21 June 2021, the company completed the bookbuild for the underwritten $220 million placement component of the $250 million equity raise. Primarily, this will be used to acquire the two Wellington re-development opportunities and fund the Bowen House re-development plan. On 22 June 2021, it opened its non-underwritten retail offer of up to $30 million.

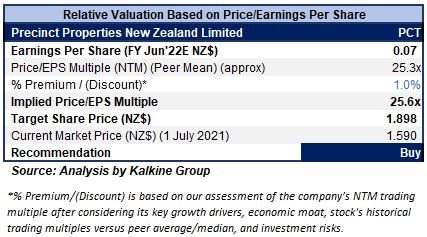

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Stock Recommendation

Considering the aforesaid facts, we have valued the stock using a P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We believe the company can trade at a slight premium to its peer P/E (NTM Trading multiple) as the company is focused on concentrated ownership in strategic locations, investing in quality assets and environment, and maintaining a long-term view on future growth.

For relative valuation, we have taken peers like Asset Plus Ltd. (APL.NZ), Property for Industry Ltd. (PFI.NZ), and Argosy Property Ltd. (ARG.NZ).

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $1.59 per share on 1st July 2021.

2) Kiwi Property Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.85 billion, Gross Dividend Yield: 5.589%)

Business Description:

Kiwi Property Group Limited (NZX: KPG) has over 25 years of exposure in property investment, development, and asset management in retail, and office buildings.

Outlook

As per the management, the property market started FY22 with a strong ethos and a clear emphasis to create value for shareholders and other stakeholders. The company will continue to focus on its strategy to diversify fund and property investment, grow strategic property development, develop community creation, and involve in active leasing and asset management. Meanwhile, the cash dividend for FY22 is expected to be no less than 5.30 cents per share.

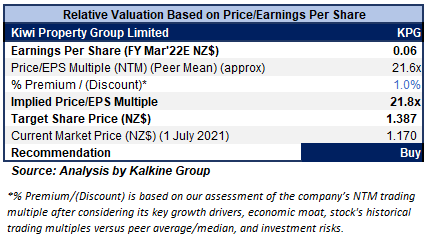

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Stock Recommendation

Considering the aforesaid facts, we have valued the stock using a P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We believe the company can trade at a slight premium to its peer P/E (NTM Trading multiple) considering improved occupancy rate in FY21 over FY20 and better Net Margin at 84.0% in FY21 versus -76.6% in FY20.

For relative valuation, we have taken peers like Precinct Properties New Zealand Ltd. (PCT.NZ), Investore Property Ltd. (IPL.NZ), and Stride Property Ltd. (SPG.NZ).

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $1.17 per share on 1st July 2021.

3) Argosy Property Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.37 billion, Gross Dividend Yield: 4.367%)

Business Description:

Argosy Property Limited (NZX: ARG) owns a diversified portfolio of industrial, office, and retail properties in Auckland and Wellington.

Outlook

The company’s portfolio and capital position are strong, providing strong resilience. Moreover, the company is strategically placed to deliver on its objectives over the medium as well as long term. With a particular focus on initiatives such as carbon neutrality and greening 50% of the portfolio, the company will ensure that its green, resilient, and diversified business is well placed with peers, which minimizes its impact on the environment.

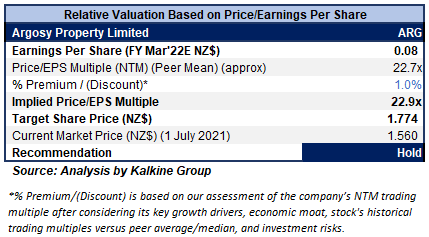

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Stock Recommendation

Considering the aforesaid facts, we have valued the stock using a P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We believe the company can trade at a slight premium to its peer P/E (NTM Trading multiple) considering better ROE as well as decent outlook.

For relative valuation, we have taken peers like Kiwi Property Group Ltd. (KPG.NZ), Precinct Properties New Zealand Ltd. (PCT.NZ), and Investore Property Ltd. (IPL.NZ).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $1.56 per share on 1st July 2021.

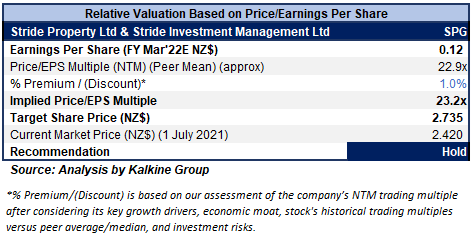

4) Stride Property Ltd & Stride Investment Management Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.16 billion, Gross Dividend Yield: 5.250%)

Business Description:

Stride Property Ltd & Stride Investment Management Ltd (NZX: SPG) consists of Stride Investment Management Limited (SIML) and Stride Property Limited (SPL). SIML is an investment manager and staff employer for the group company, and SPL owns the property portfolio and has an ownership interest in each of the Stride portfolio.

Outlook

The strategy of the company is to establish a group of portfolios in specific sectors to strengthen growth in its investment management business. It has continued to grow its office portfolio in FY21, to a value of $580 million as of 31 March 2021. Further, the company has an unconditional agreement to acquire an additional Auckland office property at 46 Sale Street for a purchase price of $152 million. This enables the company to create a newly listed product focused on the commercial office property sector. Importantly, the company intends to pay a combined cash dividend of 9.91 cents per share for FY22.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Stock Recommendation

Considering the aforesaid facts, we have valued the stock using a P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We believe the company can trade at a slight premium to its peer P/E (NTM Trading multiple) considering better margins in FY21 than peers and improved ROE as well as ROIC in FY21 over FY20.

For relative valuation, we have taken peers like Investore Property Ltd. (IPL.NZ), Asset Plus Ltd. (APL.NZ), and Precinct Properties New Zealand Ltd. (PCT.NZ).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $2.42 per share on 1st July 2021.

Comparative Price Chart

Source: REFINITIV (at 12:09 pm Auckland, New Zealand Time)

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...