I. Sector Landscape and Outlook

As per MBIE, the building and construction sector is a significant contributor to NZ’s economy as it contributed 6.7% of total GDP in FY19 and was the 4th largest employer, employing 275,600 people in FY21. In June 2021, the sector was the second-fastest growing industry in terms of employment, with 11,014 additional filled jobs than in June 2020.

As per the Reserve Bank of New Zealand (RBNZ), demand for housing has been vital and phenomenally contributed to the inflation of construction prices and prices of multiple other housing-related items, resulting in a rise in annual non-tradable inflation of 5.3% in the December 2021 quarter.

The Rise in Value of Building Work Continues in December 2021 Quarter

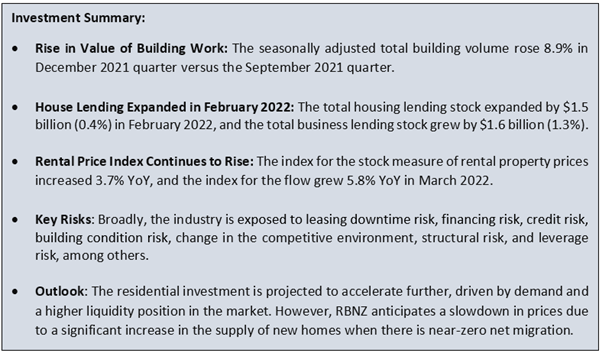

As per Stats.NZ, the seasonally adjusted total building volume increased 8.9% versus the September 2021 quarter, primarily driven by residential that increased by 5.2%, and non-residential by 16%. Meanwhile, the actual value of building work was $8.1 billion, up 17% from the December 2020 quarter, primarily driven by residential building work that increased by 19% to $5.6 billion, and non-residential work increased 13% to $2.5 billion.

Exhibit 1: Value of Building Work Put ($million), by Building Type, December 2020–2021 Quarters

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

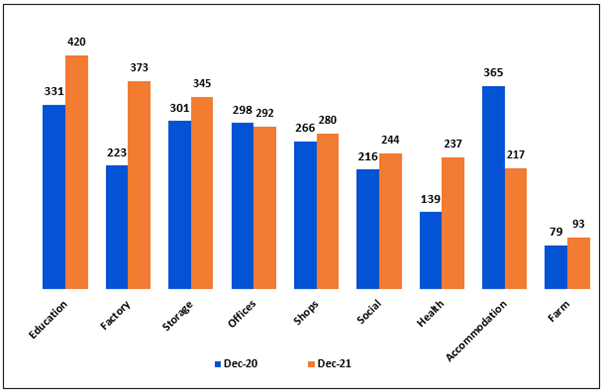

Housing Lending Continued to Accelerate in Banks and NBLIs Space

RBNZ's total housing lending stock expanded by $1.5 billion (0.4%) in February 2022, down on the $1.7 billion (0.5%) growth reported in January 2021. Annual growth continued to slow down to 9.5%, following ten months of double-digit growth. Meanwhile, the total personal consumer lending stock decreased by $69 million (-0.5%) in February 2022, down further on the -$158 million (-1.1%) decrease seen in January 2022. Annual growth remained unchanged at -6.7%. The total business lending stock increased significantly by $1.6 billion (1.3%) in February 2022, with its annual growth rising from 6.1% to 7.6%, which is the highest yearly growth rate since July 2019. Total agriculture lending stock decreased by $398 million (-0.6%) in February 2022. Annual growth further reduced from -1.1% to -1.3%.

Exhibit 2: Trend in Lending Since February 2020 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

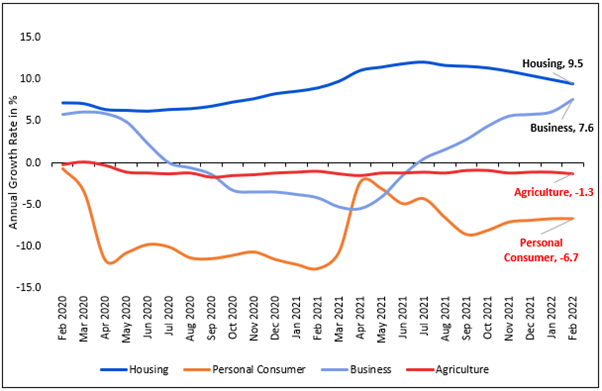

Rental Price Index Continues to Rise

As per Stats.NZ, the index for the stock measure of rental property prices, increased 0.4% MoM in March 2022. In line with this, the index for the flow measure of rental property prices grew 0.9% MoM in March 2022. Also, the index for the stock measure of rental property prices increased 3.7% YoY in March 2022, and the index for the flow measure of rental property prices grew 5.8% YoY in March 2022.

Exhibit 3: Trend in Monthly Percent Change in Rental Price Indexes, Nov 2019–Mar 2022

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Real Estate (Sector) Index generated a 2-year return of ~24.21% versus ~17.05% by the S&P/NZX 50 Index. Therefore, NZX All Real Estate Index overperformed NZX50 Index by ~7.16% in 2-year.

Exhibit 4: S&P/NZX All Real Estate (Sector) vs S&P/NZX50 Index

Source: REFINITIV

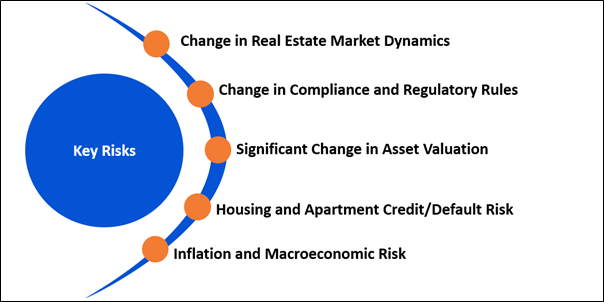

Key Risks and Challenges:

As per RBNZ, the robust demand for housing builds a price pressure and house price inflation, which is projected to slow down by December 2022. This will be driven by higher interest rates, increased home building, low net migration, changes to tax policy and tightened lending standards. Further, house prices are projected to decrease by ~9% from the end of 2021 to mid-2024, towards more sustainable levels. Falling house prices slash household wealth and weigh on consumption.

Exhibit 5. Key Risks in Real-Estate Sector:

Source: Analysis by Kalkine Group

Outlook:

As per RBNZ, there would be a decrease in house price inflation and a rise in interest rates, but the residential investment is projected to gain traction. Further, government policies and residential builds are projected to provide further medium-term support. Meanwhile, annual inflation for the construction of new houses has increased to 15.7%, reflecting robust housing demand and the higher costs of imported building materials. Global inflation is anticipated to peak during 2022 and then moderate as supply chain disruption gradually resolves.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Precinct Properties New Zealand Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.44 billion, Gross Dividend Yield: 4.258%)

Business Description:

Precinct Properties New Zealand Limited (NZX: PCT) is the largest owner and developer of premium inner-city business space in Auckland and Wellington.

Outlook

The company will continue to focus on leveraging the quality and resilience of its portfolio. The company identifies that third-party capital facilitates the participation of opportunities and delivers higher returns from the capital. The Board expects an FY22 dividend of 6.70 cps to be paid, indicating a 3.1% YoY growth in total cash dividends to shareholders. The dividend payout ratio is expected to exceed 100% of AFFO, primarily driven by the high degree of confidence in the AFFO profile.

On 14 April 2022, the company announced that it is planning an offer of secured, fixed-rate six-year green bonds for institutional investors and NZ retail investors that will be available from the week beginning 26 April 2022.

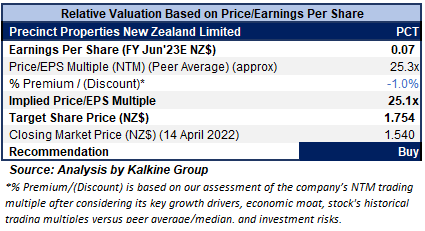

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight discount has been applied to P/E Multiple (NTM) (Peer Average), considering the company's challenges with the supply chain and sourcing of materials.

Considering the fact above, we give a “Buy” recommendation on the stock at the closing market price of NZ$1.54 per share, down 0.65% as of 14th April 2022.

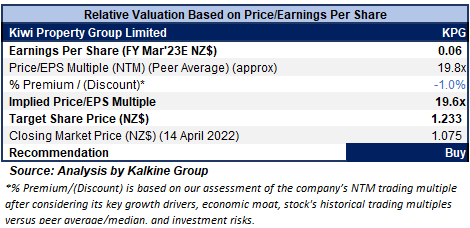

2) Kiwi Property Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.69 billion, Gross Dividend Yield: 6.472%)

Business Description:

Kiwi Property Group Limited (NZX: KPG) is investing in New Zealand real estate. The Company's primary assets are investment properties, and its reportable segments are Mixed-use, Retail, Office and Other.

Outlook

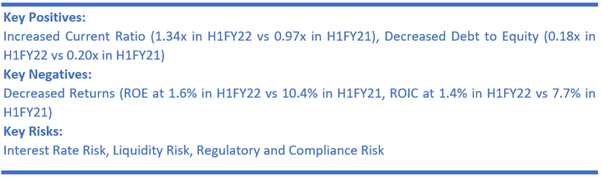

The company is on track to deliver its strategy in the future. The focus is to maintain its pace of execution, combined with the continuation of unlocking further growth and development opportunities. However, it understands the impacts of COVID-19 will adapt to accommodate these disruptions and ultimately strive to create long-term value for its shareholders and other stakeholders. The company confirmed its dividend guidance of 5.3 cents per share for FY22.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight discount has been applied to P/E Multiple (NTM) (Peer Average), considering the challenging business environment due to recent lockdowns and concern over tighter liquidity conditions to cap inflation.

Considering the factors above, we give a “Buy” recommendation on the stock at the closing market price of $1.075 per share as of 14th April 2022.

3) Asset Plus Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$105.19 million, Gross Dividend Yield: 6.203%)

Business Description:

Asset Plus Limited (NZX: APL) is a listed property investment management company that manages a property portfolio of commercial and industrial buildings in major cities of NZ.

Outlook

As per the management, the trend in the occupancy market will be a key focus area for the year ahead. The quality portfolio is sound, and its balance sheet is conservatively geared. Further, the company has sufficient funds for green Value Add opportunities. The focus area in the business in FY22 will be on the core operational elements – including addressing key expiries and remaining rent reviews, leasing up remaining vacancies and developments. As outlined in the FY21 annual results, starting 1 April 2022, the policy will be to pay dividends between 85-100% of AFFO.

On 13 April 2022, the company announced the sale of 35 Graham Street, Auckland, for $65 million, which translates into a premium to the carrying value of $62.6 million. The shareholders will meet on 3 June 2022 to approve the sale.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the factors above, we give a “Buy” recommendation on the stock at the closing market price of $0.29 per share, down 4.92% as of 14th April 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

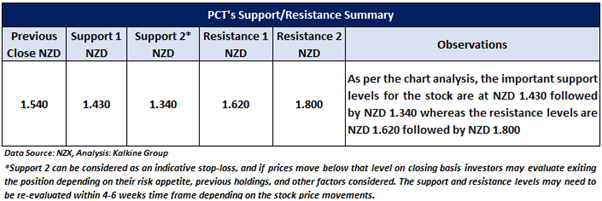

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

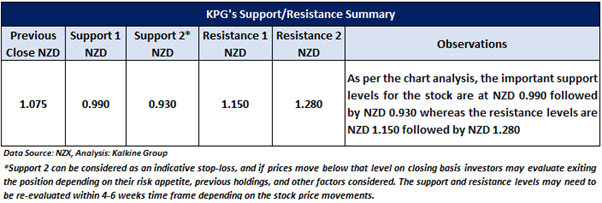

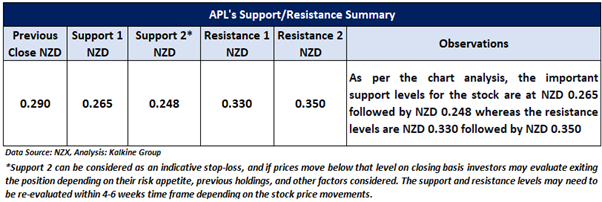

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...