Overview:

Heartland Group Holdings Limited (NZX:HGH) is the financial services group with operations in New Zealand and Australia. Templeton Emerging Markets Investment Trust Plc (NZX: TEM) is focused towards providing long-term capital appreciation for the investors, through investment in companies operating in emerging markets.

Kalkine’s Sector Report covers the Key Financial Metrics, Risks, Outlook, Technical Analysis along with the Valuation, Target Price, and Recommendation on the stock.

Sector Landscape and Outlook

As per the release by Reserve Bank of New Zealand dated 27th August 2024, the NZ commercial property market is soft because of increased interest rates, higher remote working and the continued rise in online shopping. The commercial properties – encompassing office, retail, and industrial spaces – are important for economic activity. Historically, the performance of the commercial property sector was sensitive to the broader economic cycle. The sector could amplify financial sector impacts during economic slowdown. However, the financial system is well-positioned to manage the risks. The enhanced regulatory requirements as well as improvements in lending standards reflect that NZ has a system which is more resilient than in the past.

It is of utmost importance for banks to stay vigilant and continue monitoring developments taking place in commercial property market. NZ’s annual consumer price inflation is returning to within the Monetary Policy Committee’s target band of 1% - 3%. The economic growth remains below trend as well as inflation is declining throughout advanced economies. Some central banks have started reducing their key policy interest rates. Notably, imported inflation into New Zealand has witnessed a decline to be more consistent with pre-pandemic levels.

The consumer price inflation in NZ is expected to remain near the target mid-point over the near future.

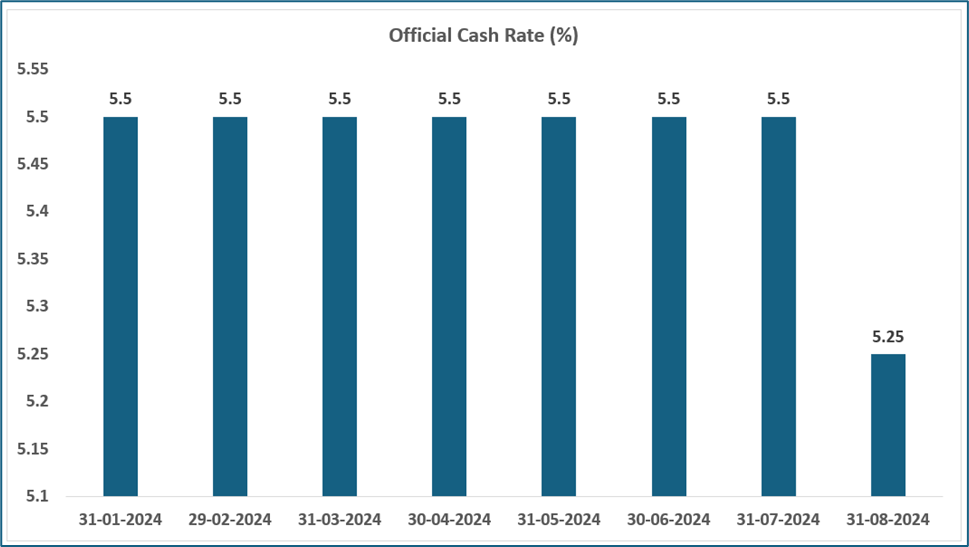

Exhibit 1: Official Cash Rate (OCR)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

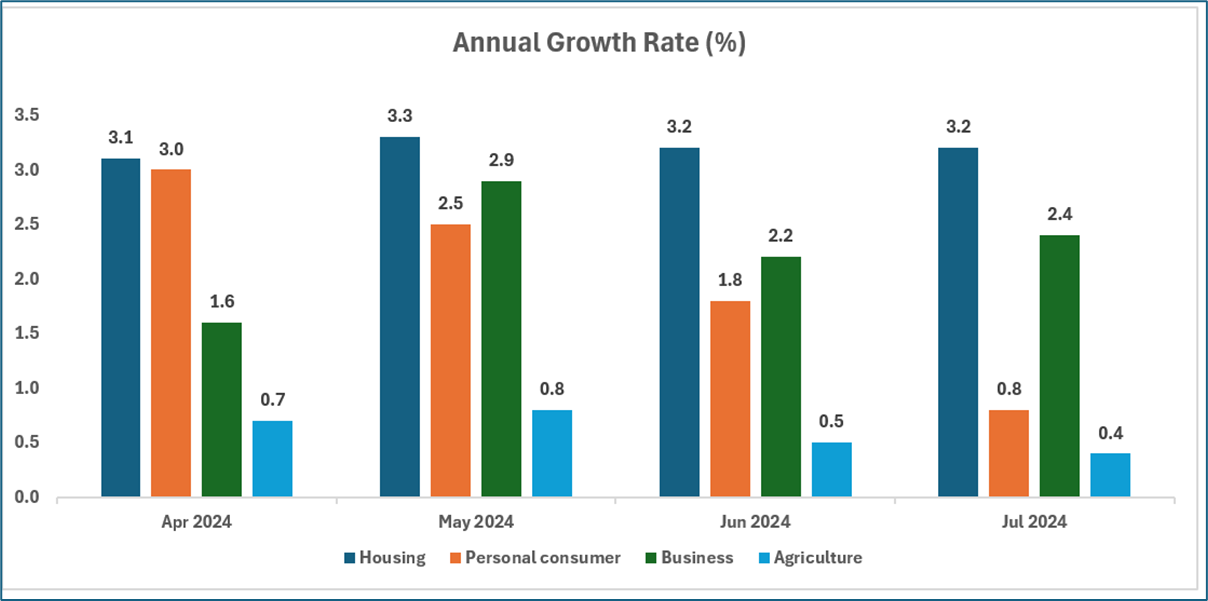

Sector Lending Summary – Banks & NBLIs (July 2024)

As per RBNZ, the housing lending stock rose by $623 Mn (0.2%) in the month of July 2024, which was down on the $908 Mn increase witnessed last month. The annual growth rate was constant at 3.2%. The personal consumer lending stock witnessed a fall of $109 Mn (or -0.8%) in July 2024. The annual growth rate declined from 1.8% to 0.8%, marking the lowest rate since the month of August 2022. The Business lending stock declined by $782 Mn (or -0.6%), which was largest monthly decline since July 2023 month. The annual growth rate increased from 2.2% to 2.4%.

The agriculture lending stock rose by $206 Mn (0.3%) in month of July 2024, down on the $376 Mn rise witnessed last month. The annual growth rate fell from 0.5% to 0.4%, marking the lowest rate since December 2022 month.

Exhibit 2: Annual Growth Rate (%)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Seasonally Adjusted Total Billings Fell Marginally

As per the credit card summary (July 2024), the seasonally adjusted total billings in NZ remained at $4.3 Bn in July 2024, reflecting a fall of 0.4% from June 2024, and down 3.8% from July 2023. The seasonally adjusted domestic billings on NZ issued cards amounted to $3.7 billion in July 2024, down by 0.3% from June 2024, and down by 4.6% from July 2023. The billings in New Zealand on overseas issued cards rose by 19.1% from last month to $0.5 Bn. Annually, billings on overseas issued cards rose 4.9%. As per the release, unadjusted total credit card advances outstanding declined to $6.0 Bn in July-24. After seasonal adjustment, the total advances outstanding stood at $6.1 Bn, 1.2% lower as compared to July 2023.

The total credit limits stood at $21.0 Bn (not seasonally adjusted) in July 2024, this was similar to June-24. Notably, this is the lowest value since the month of January 2015.

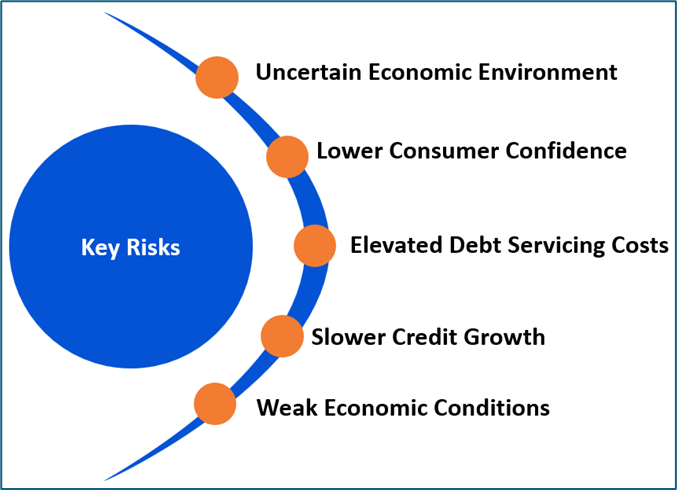

Key Risks and Challenges:

Notably, the slow fall in domestic inflation poses a risk to inflation expectations. Overall, the broader financial sector in NZ might get impacted from the uncertain macro-economic environment and geopolitical tensions.

The growth in China was softer than anticipates, because of the depressed property market as well as weak consumer demand. While the US growth remained firm, some indicators reflect emerging weakness. The recent volatility in global asset markets implies nervousness about the US economic prospects, geopolitical risks as well as outlook for the international trade policy.

As per the Committee, the global inflation continued to decline but remains elevated in certain parts of the services sector in several countries. Also, with higher debt servicing costs as well as weak economic conditions, there are households and businesses witnessing financial stress.

Exhibit 3. Key Risks in Financial Sector:

Source: Analysis by Kalkine Group

Outlook:

The Committee highlighted that central banks have started cutting the policy interest rates, implying reduced core inflation, weaker activity as well as softer labour markets. Therefore, NZ’s economic activity and near-term inflation indicators now resemble those in countries where central banks have initiated cutting the policy rates. While discussing the fiscal policy, the Committee mentioned that government expenditure has been declining as the share of the broader economy, with contractionary impacts already felt as well as anticipated to continue. However, whether or not tax cuts would boost consumption is more uncertain. While tax cuts might stimulate demand, it is also possible that households become more cautious regarding spending in the current economic environment.

The inflation declined considerably in the quarter ended June, mainly because of lower tradables inflation, while domestic inflation fell in line with anticipations. The members were encouraged that surveyed business inflation expectations returned to ~2% at medium and longer-term horizons. All measures of core inflation declined and components of CPI which are sensitive to monetary policy have further witnessed a decline. The recent indicators provide confidence that inflation would be returning sustainably to the target within reasonable time frame.

Apart from the sector-specific factors, an analysis on 2 NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

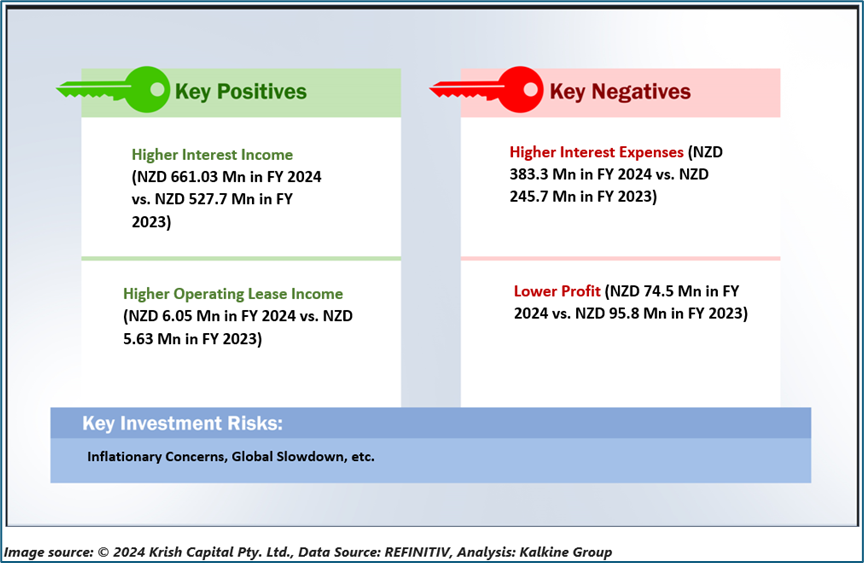

1) Heartland Group Holdings Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 977.08 million, Annual Dividend Yield (TTM)1: 9.04%)

Business Description:

Heartland Group Holdings Limited (NZX:HGH) is the financial services group with operations in New Zealand and Australia.

Outlook:

HGH stated that significant strategic milestones are setting the foundation to achieve FY 2028 growth ambitions. It has completed the acquisition of Challenger Bank Limited as well as rebranded the authorised deposit taking institution (or ADI) to Heartland Bank Australia Limited. It was able to successfully complete a $210 Mn equity raise to finance the acquisition, with robust investor support. Heartland Bank’s core banking system has been upgraded, allowing increased digitalisation and automation.

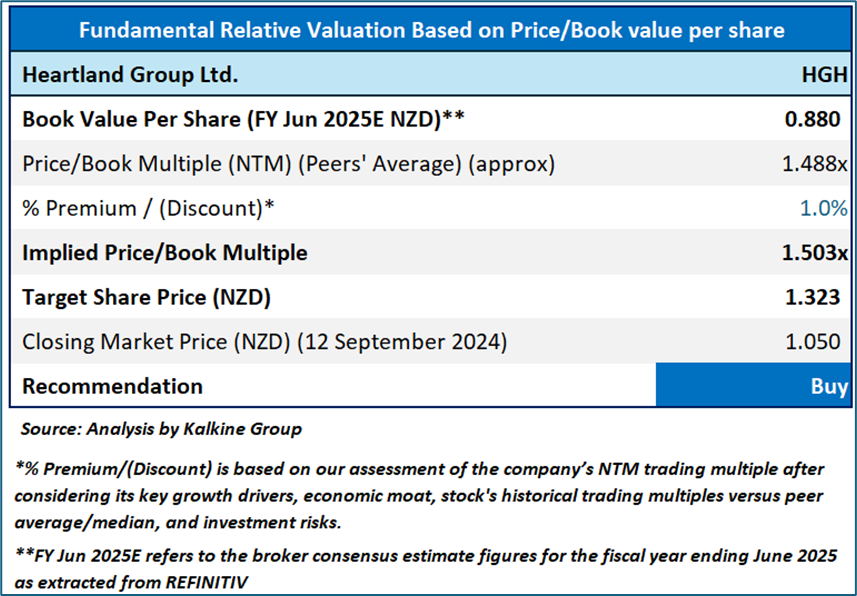

Valuation Methodology: Price/BV Per Share Based Relative Valuation (Illustrative)

Technical Overview:

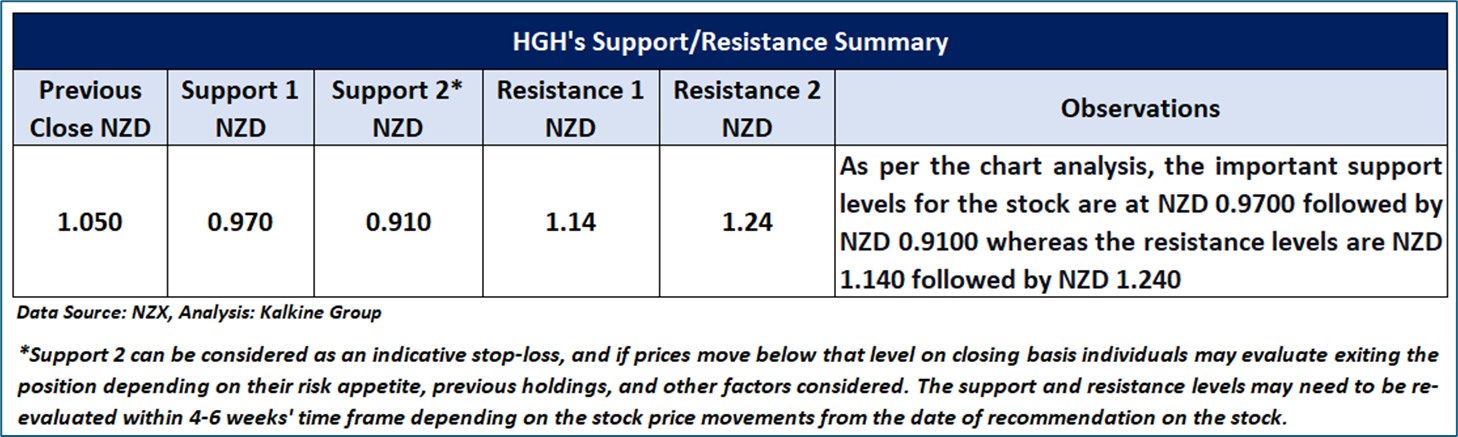

HGH Daily Technical Chart, Data Source: REFINITIV

Technical Commentary

While experiencing a downtrend, HGH’s stock prices have developed a Head and shoulders pattern, suggesting that the stock might resume its current downtrend if the pattern’s Neckline at NZD 1.03 is penetrated. Moreover, the momentum oscillator RSI (14-period) is trading below the midpoint, adding further evidence to the previous analysis. Prices are trading between its previous peak and trough, which might function as resistance and support levels for the stock, respectively. A significant support level for the stock is positioned at NZD 0.97, while critical resistance level is located at NZD 1.14.

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 1.05 per share as on 12th September 2024.

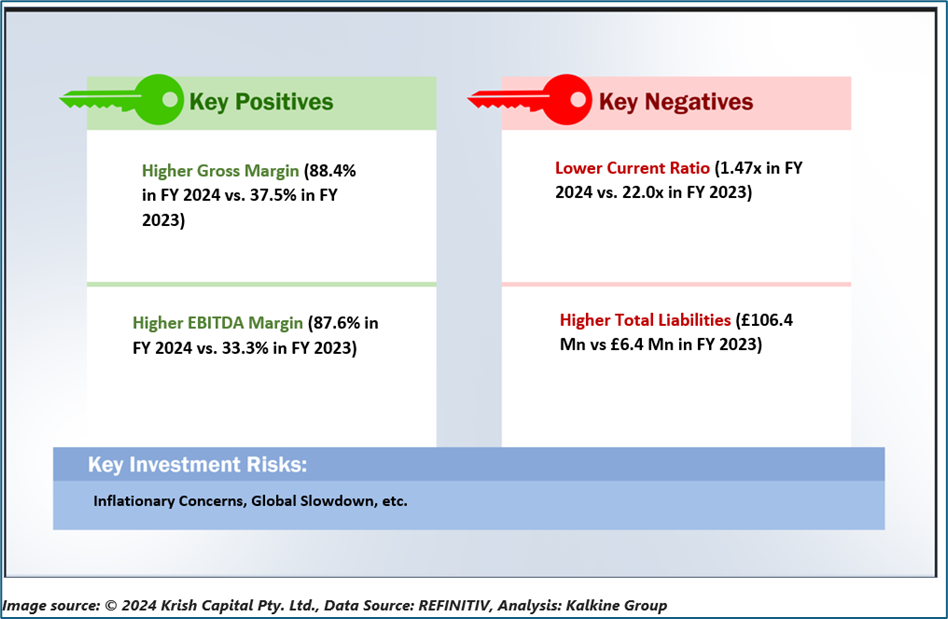

2) Templeton Emerging Markets Investment Trust Plc (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZD 3.5 Bn, Annual Dividend Yield (TTM)1: 3.08%)

Business Description:

Templeton Emerging Markets Investment Trust Plc (NZX: TEM) is focused towards providing long-term capital appreciation for the investors, through investment in companies operating in emerging markets.

Outlook:

While there has been significant deterioration when it comes to geopolitical environment, the Board believes that the equity markets in which TEMIT invests are less expensive as compared to those of developed markets, while the prospects for economic growth in emerging markets are superior. These 2 factors are expected to make emerging market equities appealing for long-term investment. The company expects that shareholders would be rewarded with the returns they were earning from investing in the fastest growing economies in the world.

Technical Overview:

Technical Commentary

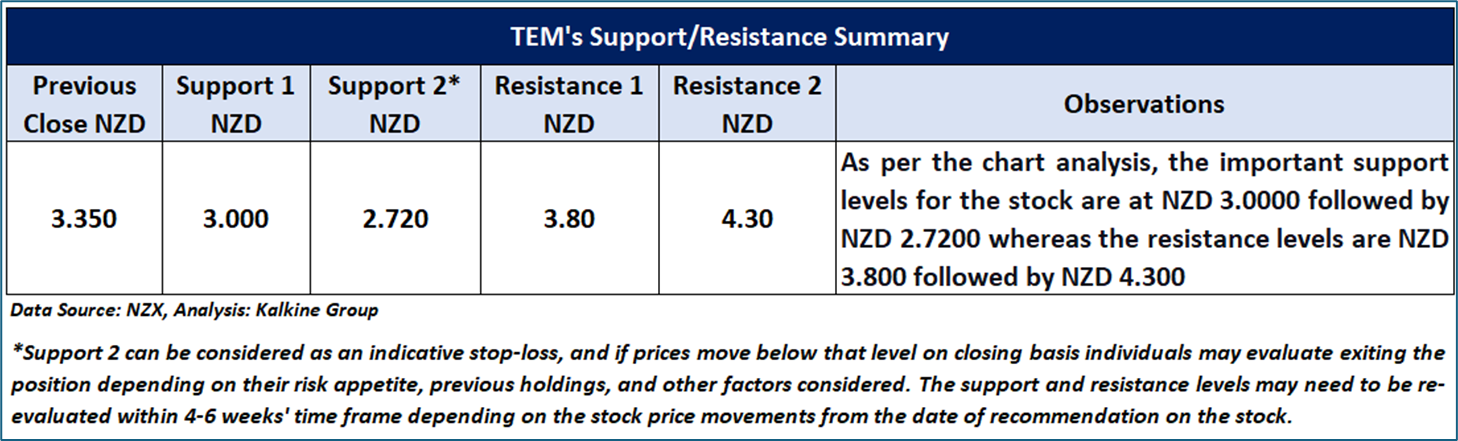

On the daily chart, TEM’s stock prices are trading near the upper boundary of a trading range established since September 2023, anticipating for a potential minor correction to the lower boundary of the mentioned sideways period. Moreover, the momentum oscillator RSI (14-period) is trending southward, adding more evidence to the previous observation. Prices are fluctuating between the range’s upper and lower boundaries, which might serve as resistance and support levels for the stock, respectively. A critical support level for the stock is positioned at NZD 3.0, while critical resistance level is located at NZD 3.80.

TEM Daily Technical Chart, Data Source: REFINITIV

Stock Recommendation

Considering the facts above, a ‘Hold’ recommendation on the stock has been provided at the closing market price of NZD 3.35 per share as on 12th September 2024.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is September 12, 2024. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer This report has been issued by Kalkine New Zealand Limited (FSP691351) (NZBN:9429047678101) (“Kalkine”). Kalkine is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity securities, managed funds and other managed investment schemes and other financial advice products. The recommendations and opinions in this report and on Kalkine website do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...