I. Sector Landscape and Outlook

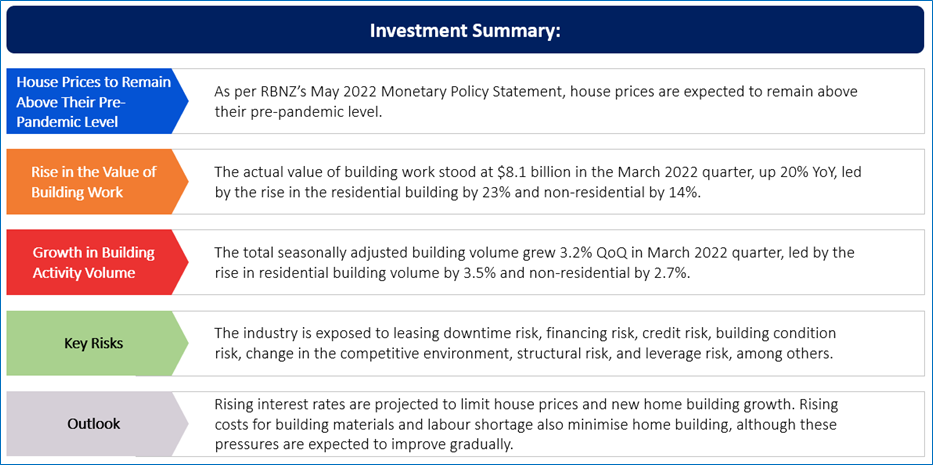

As per the Reserve Bank of New Zealand’s (RBNZ) ‘Financial Stability Report’ May 2022, house prices are projected to slow household spending growth due to the fall in wealth and higher mortgage interest payments. Further, it expects house prices to fall back to April 2021 levels, while the size and speed of the fall are highly uncertain. Despite the recent fall in house prices, the pricing levels remain above the justified levels based on economic fundamentals. These fundamentals include but are not limited to the supply of houses, yields from rents, the opportunity costs of other investments, the tax treatment of housing, and interest rates.

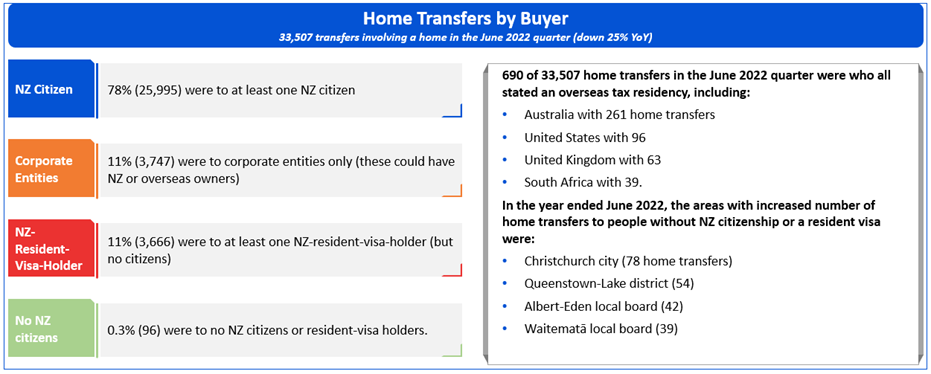

Momentum in Home Transfers

As per Stats.NZ, the property transfers stood at 42,396 including 33,507 home transfers, in the June 2022 quarter. Of this, 0.3% of home transfers were to people without NZ citizenship or resident visas in the June 2022 quarter, unchanged from the June 2021 quarter. Meanwhile, there were 143,931 home transfers (down 21% YoY) during year ended June 2022.

Exhibit 1: Home Transfers by Buyer

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

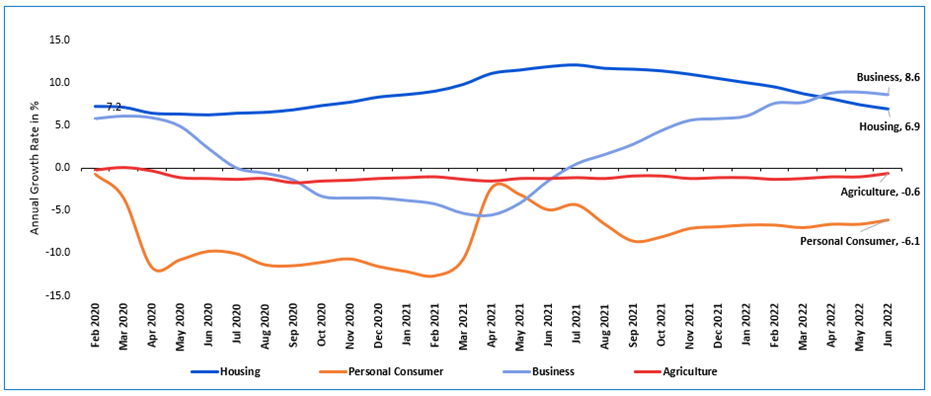

Rise in House Lending Continued in June 2022

As per RBNZ, the total housing lending stock grew by $1.1 billion (0.3%) in June 2022. Annual growth continued to slide to 6.9%, from 7.4% reported the previous month, the eleventh consecutive monthly decrease. Total personal consumer lending stock fell by $29 million (-0.2%) in June-22. Annual growth grew to -6.1% from -6.6% the previous month. The total business lending stock grew by $1.0 billion (0.8%) in June 2022, with its annual growth falling from 8.9% to 8.6%, following last month, which was the highest annual growth rate since Feb-09. Total agriculture lending stock grew by $310 million (0.5%) in June-22. Annual growth grew to -0.6% from -1.0% in the previous month.

Exhibit 2: Trend in Lending – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

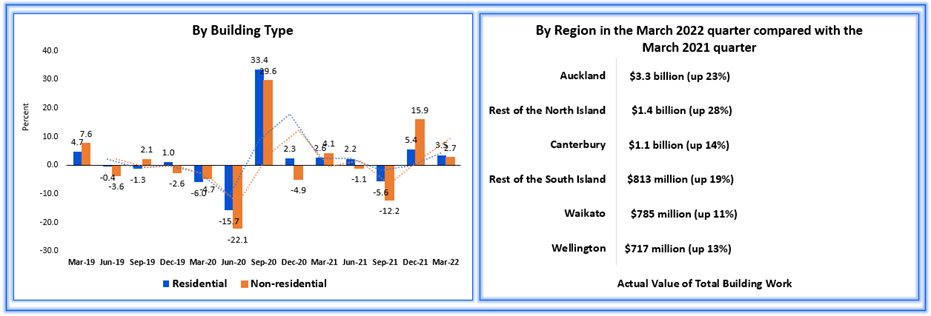

The Rise in Building Activity Volume

As per Stats.NZ, the seasonally adjusted total building volume increased 3.2% QoQ in the March 2022 quarter, driven by the rise in residential by 3.5% and non-residential by 2.7%. Meanwhile, the total building value stood at $8.1 billion, up 20% YoY during the March 2022 quarter, driving the rise in residential building work by 23% to $5.6 billion and non-residential work by 14% to $2.5 billion.

Exhibit 3: Trend in Volume of Building Work Put in Place, By Building Type, March 2019–2022 quarters

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Real Estate (Sector) Index generated a 5-year return of ~52.35% versus ~47.23% by the S&P/NZX 50 Index. Therefore, NZX All Real Estate Index overperformed NZX50 Index by ~5.12% in 5-year.

Exhibit 4: S&P/NZX All Real Estate (Sector) vs S&P/NZX50 Index

Source: REFINITIV

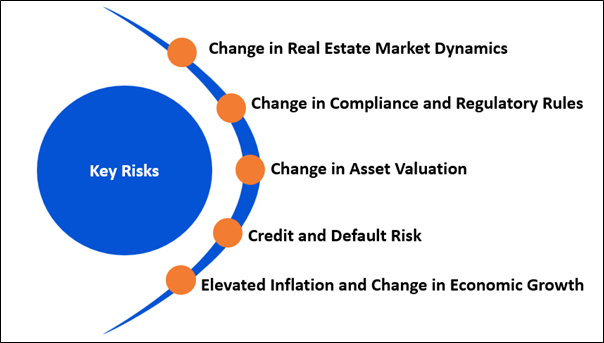

Key Risks and Challenges:

As per RBNZ, the rise in the interest rate and fall in house prices could negatively impact construction-sector activity. This could lead to more developers applying for insolvencies and many incomplete or cancelled projects. This would result in a profound fall in residential investment and present downside risks to the outlook of housing prices. Due to banks' tighter lending rules, home buyers find it increasingly complicated to borrow at higher debt-to-income ratios. Further, lower migration is expected to reduce additional housing demand.

Exhibit 5. Key Risks in Real-Estate Sector:

Source: Analysis by Kalkine Group

Outlook:

As per treasury.NZ, the demand from the construction sector is easing rapidly, with falling new home consents and feeble industry sentiment, although the pipeline of work remains large. Demand for building new homes decreased by 2.3% in June 2022 versus May 2022 and 14% down from June 2021. In the 12 months ended June, consents issuance attained a new high of 50,736, which is expected to trend down. The substantial pipeline of consents to be completed, supply chain disruptions and labour shortages are impacting the housing industry. Meanwhile, in June 2022 versus May 2022, the index for the stock measure of rental property prices grew 0.4%, and the index for the flow measure of rental property prices grew 0.4%.

Apart from the sector-specific factors, we have also analysed three NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Precinct Properties New Zealand Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.27 billion, Annual Dividend Yield (TTM)1: 4.52%)

Business Description:

Precinct Properties New Zealand Limited (NZX: PCT) is the largest owner and developer of premium inner-city business space in Auckland and Wellington.

Outlook

The liquidity and the company's balance sheet position are expected to improve, which could enhance its earnings. Further, it will continue to leverage the quality as well as the resilience of the portfolio.

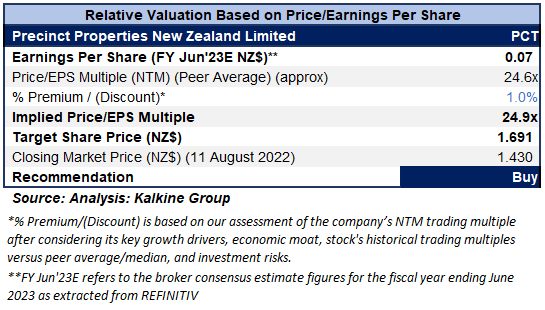

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

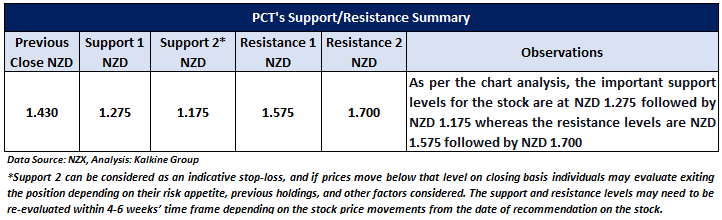

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering a diversified revenue stream and decent outlook.

Considering the above factors, a ‘Buy’ recommendation on the stock has been provided at the closing market price of $1.43 per share, down 2.72% as of 11 August 2022.

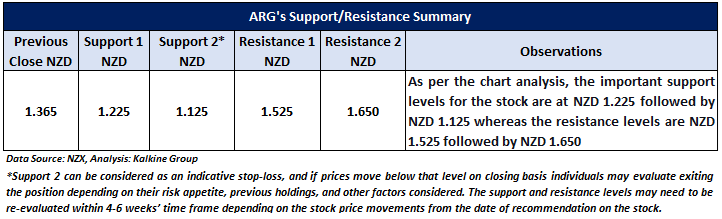

2) Argosy Property Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.16 billion, Annual Dividend Yield (TTM)1: 5.18%)

Business Description:

Argosy Property Limited (NZX: ARG) is involved in investing and managing properties, including office, industrial and retail properties across New Zealand.

Outlook

A solid balance sheet and low gearing offer flexibility to the company to fund its green developments and strategic prospects. Further, the emphasis in FY23 will be on delivering healthy operational results, meeting key expiries, leasing up outstanding vacancies, finishing the key green developments, and starting fresh ones. It forecasts FY23 dividend guidance of ~6.65 cents per share, an increase of 1.5% from the prior year.

On 5 August 2022, the company advised that it has increased and extended its syndicated bank facilities with ANZ Bank of New Zealand Limited, Bank of New Zealand Limited, Hongkong and Shanghai Banking Corporation, Commonwealth Bank of Australia and Westpac New Zealand Limited.

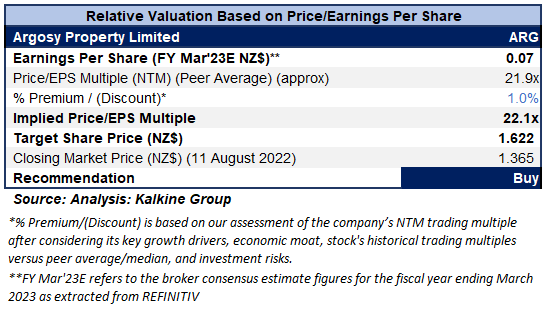

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering its sound capital position, decent portfolio and foundations for the current year and beyond, and decent property fundamentals in critical markets.

Considering the above factors, a ‘Buy’ recommendation has been provided on the stock at the closing market price of $1.365 per share, down 0.36% as of 11 August 2022.

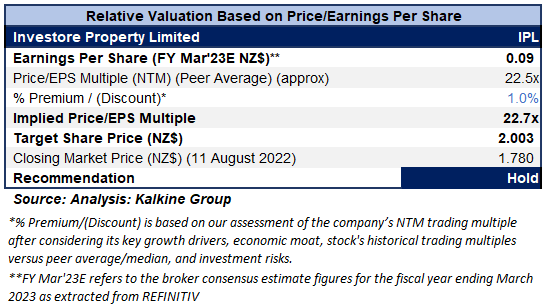

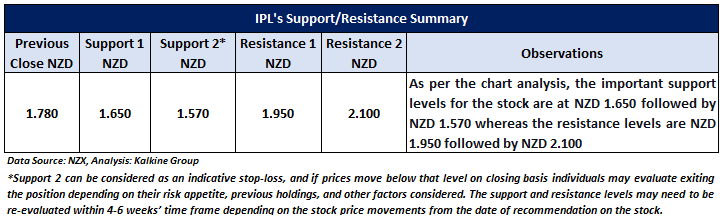

3) Investore Property Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$654.53 million, Annual Dividend Yield (TTM)1: 5.19%)

Business Description:

Investore Property Limited (NZX: IPL) invests in quality, large format retail properties throughout New Zealand and manage shareholders’ funds to maximise total returns over the medium to long-term.

Outlook

The company plans to focus on targeted growth to augment the portfolio and maximise returns. Also, it intends to grow Investore’s portfolio and income through improved portfolio management. It plans a cash dividend of 7.90 cents per share for FY23.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering a decent outlook and cash dividend for FY23.

Considering the above factors, a ‘Hold’ recommendation has been provided on the stock at the closing market price of NZ$1.78 per share, as of 11 August 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is August 11, 2022. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...