I. Sector Landscape and Outlook

Global economic and financial instruments are quickly retaining their stable levels than anticipated during COVID-19 days. New Zealand’s key export prices showed resilience, amid dairy prices at their peak. However, supply chain management and border restrictions have phenomenally impacted some businesses. Importantly, rigorous domestic fiscal and monetary policy, and successful public health measures have supported many businesses and restricted rise in unemployment levels, which could have underlined the financial system. Further, New Zealand’s economic growth depends on the global containment of the COVID-19 epidemic and on the confidence in trading partner economies.

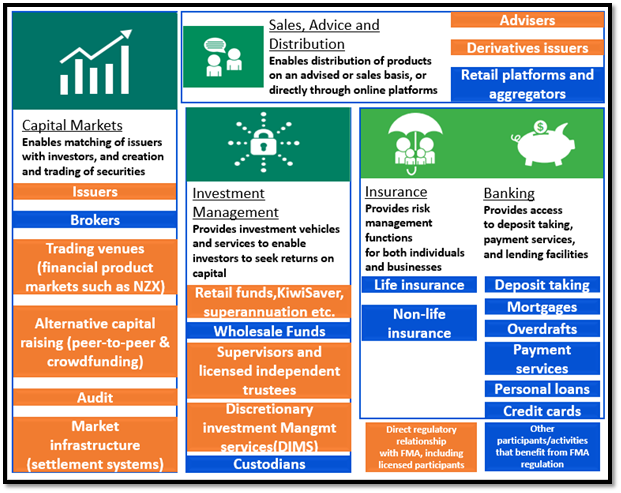

Sector Highlights by Financial Market Authority (FMA)

Exhibit 1: Sector Overview

Data Source: fma.govt.nz, Chart Created by Kalkine Group

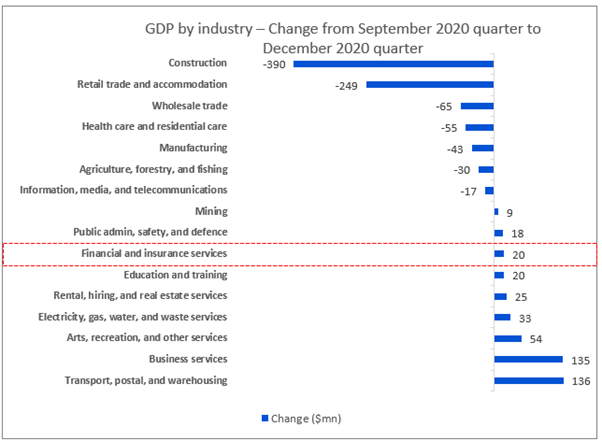

Positive Contribution by Financial & Insurance Services in December 2020 GDP

Service industries increased its contribution to GDP by 0.1% in the December 2020 quarter. Further, transport, postal, and warehousing, and business services, grew 7.0% and 2.0% respectively in the December 2020 quarter. In value terms, the Financial and insurance services industry reported a growth of $20 million in the December 2020 quarter over the September 2020 quarter driven by the positive sentiments of the market participants that were under pressure due to COVID-19 restrictions.

Exhibit 2: Financial & Insurance Services Reported Growth in December 2020 Quarter GDP

Data Source: stats.govt.nz, Chart Created by Kalkine Group

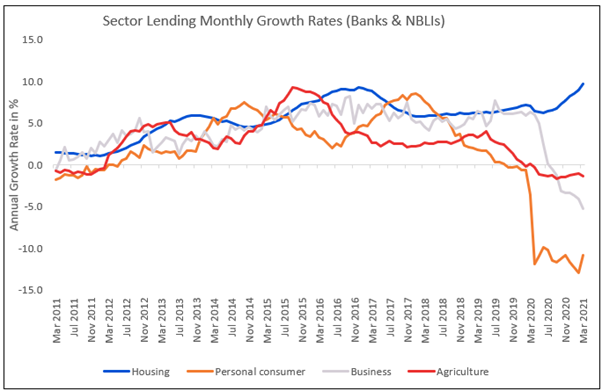

Big Rise in House Lending on the Back of Low Rates

As per the Reserve Bank of New Zealand, the housing lending from Banks and non-bank lending institutions grew by $3.7 billion (1.2%) in March 2021, indicating the largest monthly percentage increase since April 2007. Further, the annual growth jumped to 9.7% from 9.0%, its highest level since April 2008. Meanwhile, total consumer lending stock decreased by $243 million (-1.7%) in March 2021 and annual growth remained strongly downside, at -10.8% in March 2021. In line with this, the total business lending stock grew by $198 million (0.2%) in March 2021 and annual growth fell to -5.2%. Importantly, agriculture lending stock fell by $63 million (-0.1%), with its annual growth decreasing to -1.3%. This volatility indicates the requirement of funds from various industries is under pressure on the back of COVID-19.

Exhibit 3: 10 Year Lending Growth – Banks and NBLIs

Data Source: rbnz.govt.nz, Chart Created by Kalkine Group

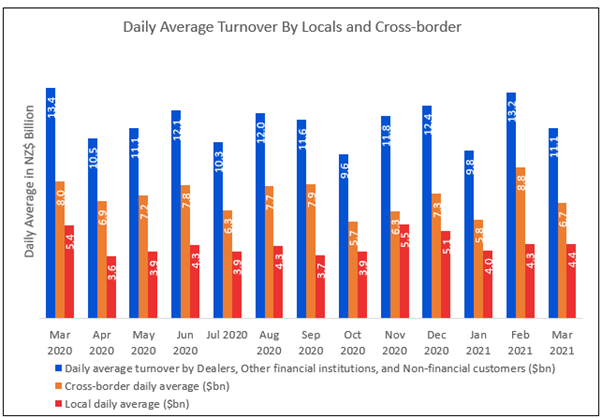

Foreign Exchange Turnover Returning to Pre-Covid Levels

As per the Reserve Bank of New Zealand, the average daily foreign exchange from Dealers, Other financial institutions, and Non-Financial Customers stood at $11,111 million, up 5.9% YoY mainly driven by the average daily foreign exchange by Local bodies that reported at $4,377 million, up 20.7% YoY that was partially offset by a decline in average daily foreign exchange by cross broader agencies to the tune of 1.9% YoY to $6,734 million.

Importantly, the broader international markets have recovered partially with restricted travel due to Covid-19 circumstances and the similar momentum is expected further. Hence, it can be anticipated that the much of negative market catalysts may have been factored in the current transaction levels.

Exhibit 4: Daily Average Foreign Exchange Turnover Grew 5.9% YoY in March 2021:

Data Source: rbnz.govt.nz, Chart Created by Kalkine Group

Continued Rise in Fund Under Management in New Zealand

As per the Reserve Bank of New Zealand, the total value of funds under management grew to $227 billion, up 4.9% QoQ as of 31 December 2020, with YoY growth at 6.0% driven by a rise in the value of Short-term debt securities by 17.4% QoQ with a record high of $11.3 billion.

Following this, Units in trusts grew by 19.4% QoQ with the fund at $24.8 billion and a staggering jump in Derivatives in a net asset position, which increased in triple-digit by 154.6% QoQ to $965 million. Meanwhile, Kiwisaver and Other Superannuation schemes increased further by 5.5% and 7.0% QoQ respectively, with Kiwisaver reaching a high of $77.2 billion.

Exhibit 5: Managed Funds Survey – December 2020

Data Source: rbnz.govt.nz, Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Financials (Industry Group) Index generated a 1-year return of ~60.90% as compared to ~15.20% by the S&P/NZX 50 Index.

Exhibit 6: S&P/NZX All Financials Index outperformed NZX50 Index by whooping ~45.70% in one year period:

Source: Refinitiv (Thomson Reuters)

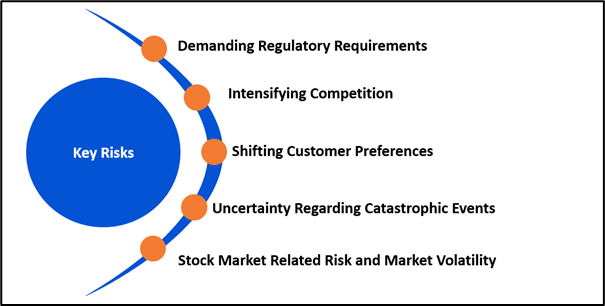

Key Risks and Challenges:

As per the Reserve Bank of New Zealand, the country is less impacted than previously feared, vulnerabilities in the financial system continue as some businesses remain vulnerable. The government is also looking into low global interest rates following an increased risk-taking capacity and higher asset prices. Further, a high percentage of new lending has had elevated debt-to-income and loan-to-value ratios (LVR). Resulting, more vulnerability for recent borrowers against an increased mortgage rate and uncover households and the financial system to a fall in house prices. Meanwhile, the outlook for office space is under pressure, as the new norm of working-from-home arrangements resulted in tenants to reassess their long-term floor space needs.

Exhibit 7: Key Risks in the Financial Services Sector:

Sources: Analysis by Kalkine Group

Outlook:

KiwiSaver has effectively formed a collection of domestic savings. Since inception, it has provided virtually all participants positive investment returns, amidst some promising recent developments in cutting fees and innovating products. Moreover, stronger than expected recovery was witnessed throughout the commercial real estate, banking and capital markets, commodity market, and investment management sectors in recent times as the investments in these domains have been considered as preferred sectors amidst recovery in the economy. This could grow further in the coming periods, with minor hiccups.

2021 will reflect a widespread recovery in the financial domain in terms of transforming operations to power success by changing preferences towards investors and adding new clients. Further, AUM growth and regulatory effort to cut costs for customers are being seen as growth drivers by the investors as they would want to join the investment basket when regulators are monitoring the operations of the service providers.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance, and potential as expected to be delivered in the near to medium term.

1) F&C Investment Trust PLC (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$8.77 billion, Gross Dividend Yield: 1.413%)

Business Description:

F&C Investment Trust PLC (NZX: FCT) is an investment trust company that aims to grow the capital and income over the long term. It had £5.1 billion of total asset as of 31 March 2021.

Outlook

As per the management, years ahead will be challenging due to COVID-19 circumstances as it possesses a phenomenal threat to near-term growth prospects. The stock market-related investments are volatile resulting direct impact on NAV. However, the company also expects better growth as the year progresses, and a follow-on improvement in corporate earnings. Having said that, equity markets have already discounted much of the positive factors about respective companies.

Meanwhile, valuations are being buoyed by monetary and fiscal measures. The company stated that it expects support for some time to come, but disappointment on earnings delivery or on inflation could result in volatility as well as a sharp setback in the stock markets.

However, the company remains focused on the longer-term horizon. Meanwhile, net assets per ordinary share (prior charges at market value) ex-income stood at 884.00 pence and cum-income stood at 884.92 pence.

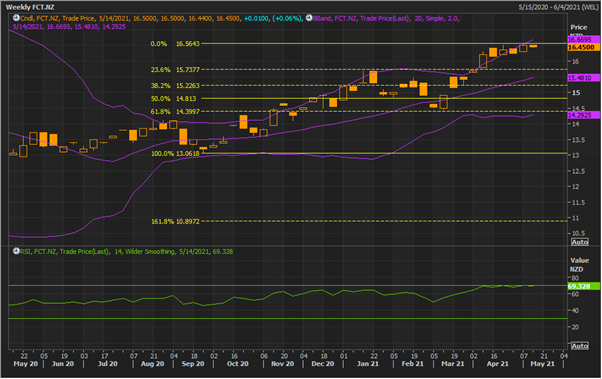

Technical Analysis

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

While remaining in a winning streak, the stock has given a softer close for the ongoing week at $16.45, forming a ‘Bearish Harami’ pattern on the chart, signaling the potential downside for it. The technical indicator RSI with a reading around 69 and a flattish curve at the end, suggests that the stock is in the overbought zone with momentum flattening.

Going forward, the stock may have resistance around the upper Bollinger band of $16.67 whereas support could be around the 23.6% retracement level of $15.74.

Stock Recommendation

The stock has a 52-week low and high of $12.95 and $16.50 respectively and is currently trading above the average of 52-week high-low range. The stock reported a rise of ~18.8% in 9 months, and ~24.6% in 1 year.

Considering the current trading levels, bluechip clients, over 150 years of experience in financial market, and organic growth in key markets, we give a “Hold” rating on the stock at the current market price of $16.45, up 0.06% on 13th May 2021.

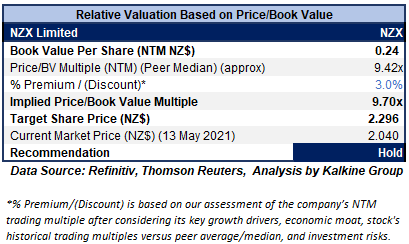

2) NZX Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$570.36 million, Gross Dividend Yield: 4.215%)

Business Description:

NZX Limited (NZX: NZX) is a New Zealand’s exchange that owns Smartshares, New Zealand’s only issuer of listed Exchange Traded Funds, and KiwiSaver provider SuperLife. It also offers wealth management services via Wealth Technologies business.

Outlook

As per the management, operating earnings are expected to be in the range of $32.0 million to $35.5 million for FY21 driven by volume growth, value traded, funds under management, and funds under administration. In FY20, the strength of the company was indicated by the 149% jump in the volume traded and a 42% rise in the value traded. NZX is constantly looking for global partners. On this thread, BNP Paribas is anticipated to become a General Clearing Participant in 1H21 and Heads of Agreement with Singapore Exchange is expected to increase NZX’s dairy derivatives market together. There has been a successful launch of EEX, the first auction under NZ Emissions Trading Scheme, on 17th March 2021.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

We have applied Price/Book Value (P/BV) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/BV Multiple (NTM) (Peer Average) as the management is constantly looking to expand the business through organic way, signing partnership agreement, and technological advancement. Smartshares Funds Under Management (FUM) increased 28% in FY20 and had $5 billion at year-end, exceeding 2023 goal in growth strategy. Further, it attracted over $800 million in net investor cash flows.

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $2.04 per share, up 1.49% on 13th May 2021.

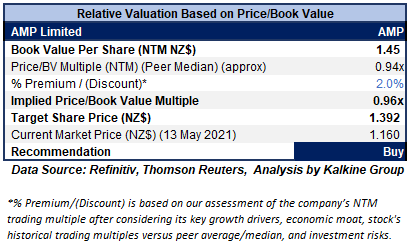

3) AMP Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.99 billion, Gross Dividend Yield: 9.379%)

Business Description:

Founded in 1849, AMP Limited (NZX: AMP) is a wealth management company with an accelerating retail banking business and a growing international investment management business.

Outlook:

The company, in its media release dated 11th February 2021, announced NZWM will shift to an index-based investment approach in H1 FY 2021, offering a simpler and more cost-effective investment plan, focused to improve performance for clients.

Further, reinventing wealth management in Australia revolves around developing best-in-class retail super business, where there has been a successful delivery of next phase of superannuation simplification program that reduced the number of products from ~70 to 11. In line with this, there has been a focus to grow a successful platform business where it is continuously enhancing functionality and products.

Importantly, its plan is on track to report A$300 million annual run-rate savings (ex AMP Capital) by the end of FY22. The company continued to deploy A$100 million (pre-tax) investment initiative to further strengthen risk management, internal controls, and governance.

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

We have applied Price/Book Value (P/BV) based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/BV Multiple (NTM) (Peer Average) driven by reversing A$2.5 billion loss in FY19 to statutory NPAT of A$177 million and better margins.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $1.16 per share, up 0.87% on 13th May 2021.

4) Harmoney Corp Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$195.77 million)

Business Description:

Harmoney Corp Limited (NZX: HMY) is a personal loan provider, having facilitated ~$1.6 billion in loans to ~50,000 customers on both sides of the Tasman.

Outlook

The company is riding on strong fundamentals and robust customer inquiry that stood at $7.4 billion. Importantly, the company is focused on ~A$150 billion AU personal lending market and ~$15 billion NZ personal lending market.

This is reflected in the Q3FY21 result update where the company’s loans to new customers increased 60% to NZ$44.1 million in Q3FY21, up from NZ$27.5 million in Q2FY21.

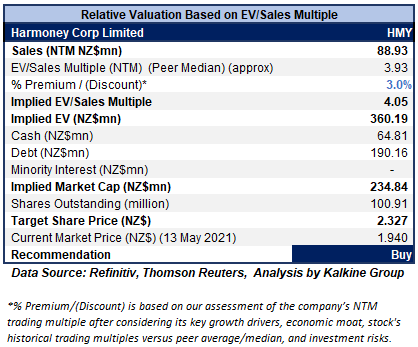

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

We have applied EV/Sales based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to EV/Sales Multiple (NTM) (Peer Average) considering $1 billion p.a. Australian origination target, attractive revenue profile, loan book and robust market position.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $1.94 per share, up 10.23% on 13th May 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Note: Investment decision should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...