I. Sector Landscape and Outlook

As per the Ministry of Business, Innovation and Employment, New Zealand has strong footprints across dairy products, meat, seafood, produce, processed and beverages. It exports five broad categories of dairy products such as Powders, casein/lactose similar, butter, cheese, and processed items, where powders, butter and cheese dominate dairy exports to most regions. Further, the country exports three broad classes of meat products where sheep and beef dominate meat exports to regions other than Australasia. Meanwhile, it exports six broad classes of seafood products where white fish, lobster, mussels, and squid are the leading seafood exports.

In line with this, the country exports four broad classes of fresh produce: (1) Kiwifruit, (2) Apples, (3) Emerging Fruit and (4) Vegetables, where kiwifruit clearly leads the export category. Besides, it exports a wide range of processed foods, broadly to Australia and Asia where China is leading the processed foods export growth. Finally, the country exports beverages across all six major product categories where wine dominates beverage exports to N. America and Europe; Australia and Asia take a more varied mix.

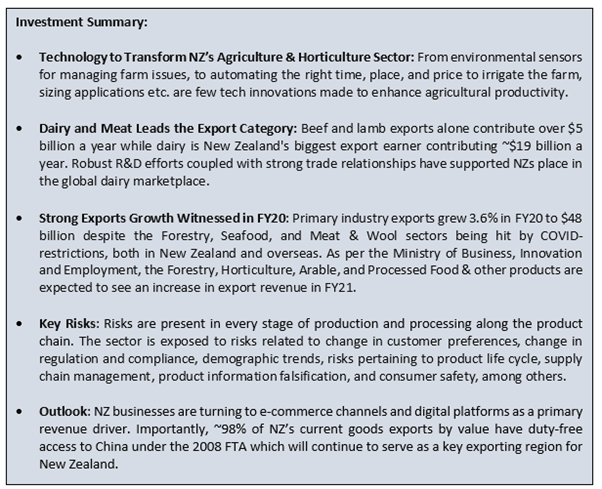

March 2021 CPI Growth is Close to Pre-COVID Level Witnessed in March 2020

The Consumers price index (CPI) grew 0.8% in the quarter ended March 2021 versus December 2020 as housing and household utilities increased 0.9%, led by actual rentals for housing (+1.0%) and home ownership (+1.2%). Followed by 1.6% rise in alcoholic beverages and tobacco category, due to increased prices for cigarettes and tobacco (+2.7%). Food prices grew 0.6%, on the back of grocery food (+0.9%) and restaurant meals and ready to eat foods (+0.9%). In addition, transport prices increased 3.9%, led by rise in prices for private transport supplies and services (+4.9%) and purchase of vehicles (+2.6%).

Exhibit 1: CPI, Quarterly Change, March 2017–March 2021

Data Source: stats.govt.nz, Chart Created by Kalkine Group

Dairy and Meat Leads the Export Value

Beef and lamb exports alone contribute over $5 billion a year while dairy is New Zealand's biggest export earner contributing ~$19 billion a year. The sector supplies mainly pasture-based farming, with large herds and large-scale value addition facilities. A phenomenal amount of research and development as well as strong trade relationships have supported New Zealand’s place in the global dairy marketplace. New Zealanders themselves are one of the biggest consumers of dairy milk and products, representing one of the highest domestic consumption of milk rates in the world.

Exhibit 2: New Zealand is Expanding Its Export Market across All Six Food Segments

Data Source: mbie.govt.nz, Chart Created by Kalkine Group

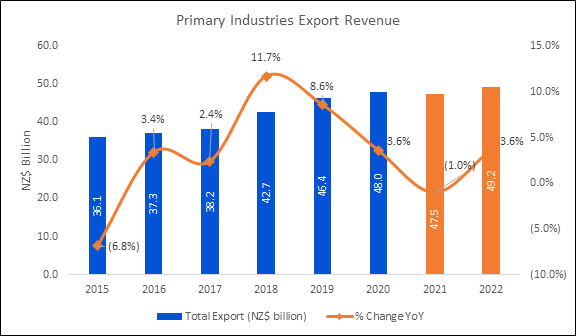

Processed Food is Expected to Lead Export Basket, Among Others

As per the Ministry of Primary Industry, processed food and other products are projected to reach $3.3 billion by June 2021 that indicates a rise of 9.2% YoY. The main growth drivers include increase in live animals, honey, innovative processed foods, and sugar and confectionery. Following this, forestry exports are projected to grow 8.1% to $6.0 billion by June 2021 on the back of resilient demand for logs from China and strong demand for sawn timber from the United States. In line with this, horticulture export revenue is projected to increase 9.1% by June 2021 to ~$7.1 billion led by robust harvests in early 2020 for most crops. Consumer demand for fresh fruit and wine grew despite COVID-19- with similar trends expected to continue.

Exhibit 3: Trend in Primary Industries Export Revenue 2015-22:

Data Source: Ministry for Primary Industry, Chart Created by Kalkine Group

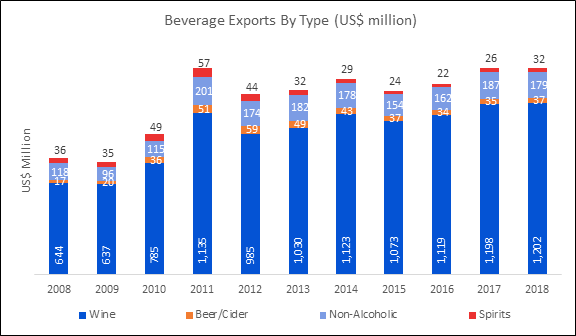

NZ Exports across All Six Major Beverage Categories, Albeit Wine is a Clear Winner

The beverage processing industry reported a revenue of $5,230 million in 2017, comprising 39% of export revenue at $2,040 million and 61% of domestic revenue at $3,190 million. Major product categories include wine, juices, soft drinks, water, Beer & cider, and spirits. The big companies in the NZ’s beverage industry are focused on beer and soft drink at the same time creating new jobs and new business units. Further, the industry is relatively fragmented as smaller wineries are privately owned, although attracting foreign investment.

Exhibit 4: Rising Trend in Beverages Export: From US$815 million in 2018 to US$1,451 million in 2018

Data Source: mbie.govt.nz, Chart Created by Kalkine Group

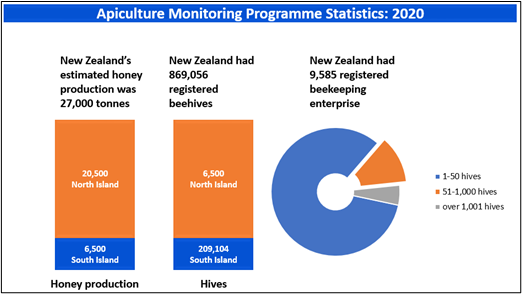

Rise in Honey Production Led by Rise in Number of Beekeepers

The honey production for the year ended June 2020 was estimated at 27,000 tonnes, up 4,000 tonnes YoY, on the back of favourable weather in most parts of the regions. Further, the national average honey yield grew by 24% to 31.1 kilograms per hive. However, average honey prices in 2019/20 continue to decrease for most honey types. For non-mānuka honey price fell by ~50%. Meanwhile, the number of beekeepers with over 50 hives decreased 5% to 1,271 beekeepers, while beekeeper count continued to increase in the hobbyist category. A total net rise of 303 beekeepers (3%) was reported in 2019/20 season. In line with this, the number of wintering hives fell by 50,000 while apiary number rose by 1,015 (up 2%).

Exhibit 5: Apiculture Monitoring Programme 2020

Data Source: mpi.govt.nz, Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Consumer Staples (Industry Group) Index generated a 5-year return of ~94.31% as compared to ~84.86% by the S&P/NZX 50 Index.

Exhibit 6: The All Consumer Staples (Industry Group) outperformed NZX 50 Index by ~9.45% in five years period:

Source: Refinitiv (Thomson Reuters) as on the close of 6th May 2021

Key Risks and Challenges:

Consumer staple products are exposed to risk in every stage of production and processing along the product chain. For instance, marine environment is exposed to ocean acidification and warming-up from greenhouse gas emissions, disappearance fear for some marine birds and mammals, and tainted costal marine habitats and ecosystems. Further, the result of climate change has increased the risk of drought, pests and diseases and costs related with shifting land-use activities which otherwise would have resulted an increase in productivity.

As per the Minister for Trade and Export Growth as well as Minister of Agriculture, in lieu of COVID restrictions, the country’s export to China fell by 1% in 2020 over 2019 whereas dairy exports to China grew while forestry and seafood exports were under pressure. There is a risk of downside export momentum in FY21 due to COVID restrictions.

Figure 7. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

New Zealand businesses are turning to e-commerce channels, as a forward-looking practice to ensure their products are delivered to their customers in the most convenient manner. Due to travel restrictions real investments are made in retaining businesses and growing their association to market either through digital platforms or local business partners. Importantly, ~98% of New Zealand’s current goods exports by value have duty-free access to China under the 2008 FTA and an upgrade will result in tariff-free access for 99% of New Zealand’s nearly $3 billion wood and paper trade to China.

The Minister for Trade and Export Growth and Minister of Agriculture has set four strategies around focused areas. (1) Retooling exporter aids, by facilitating with tools, support, and market intelligence to businesses, particularly to those who may not be able to be physically exist in the market due to travel restrictions. (2) Reinvigorating international trade architecture to those trade rules and organisations who have become more important than earlier. Extending negotiations on important new trade agreements, including FTAs with the European Union and the United Kingdom. (3) Refreshing key trade relationships to enable the businesses have many overseas market options. (4) Learning lessons of COVID-19 to build New Zealand’s future resilience against economic shocks.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Scales Corporation Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$650.74 million, Gross Dividend Yield: 5.762%)

Business Description:

Scales Corporation Limited (NZX: SCL) is engaged in agribusiness that is spread across geographies. It has exposure to unique and separate components of the New Zealand primary sector.

Outlook:

Amid continuing disruptions in global supply chains (specifically port side delays and costs), the management has revised its forecasted underlying net profit in the ambit of $27.5-$33.5 million while underlying EBITDA in the range of $46.5-$53.5 million. The company is seeing a phenomenal lower levels of stone fruit exports from the Otago region. Further, the Tasman region is anticipating a drastic lower level of pip fruit exports impacting on third party export volumes for Mr Apple and Fern Ridge. Importantly, ongoing interruptions in shipping is resulting a higher port side charges providing pressure on business units.

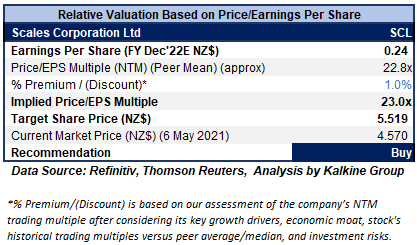

Valuation Methodology: Price/Earnings per Share Based Relative Valuation (Illustrative)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation

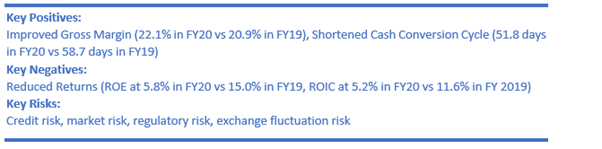

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/E Multiple (NTM) (Peer Average) considering improved gross margin in FY20 at 22.1% over 20.9% in FY19 and strong cash position that could help the company in tackling challenges.

For this purpose, we have taken peers such as A2 Milk Company Ltd (ATM.NZ), Delegat Group Ltd (DGL.NZ), New Zealand King Salmon Co Ltd (NZK.NZ), to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $4.57 per share, down 0.22% on 6th May 2021.

2) Foley Wines Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$115.04 million, Gross Dividend Yield: 2.328%)

Business Description:

Foley Wines Limited (NZX: FWL) is an integrated wine company. It has a pool of iconic wineries and brands from New Zealand’s best acclaimed wine regions.

Outlook

The company is committed to the strategy of building brands which satisfy the requirements of the discerning retailers as well as restaurants throughout the world.

FWL announced that it has completed the harvest for the 2021 vintage and the results reflect that the 2021 vintage was down on the prior years in the major growing regions. Notably, the harvest totalled 5,582 tonnes throughout the Marlborough, Martinborough and Mt Difficulty wineries, implying an overall decrease of 28% on previous year’s harvest of 7,803 tonnes.

The company is working on the premiumisation strategy and there are expectations that the work done on this along with securing new channels at the higher price points would be helping in mitigating the impact of costs of the higher vintage costs.

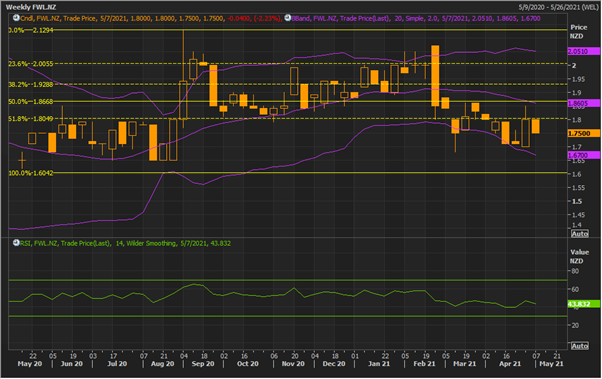

Technical Overview:

Weekly Chart

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock rose from its low of $1.60 to the high $2.13. But it could not sustain with the positive momentum and came under selling pressure with sporadic bounces. For the ongoing week, it has given a softer close at $1.75. The technical indicator RSI with a reading around 44 suggests neutral momentum for the stock.

Going forward, the stock may have resistance around the converging point of 50% retracement level and 20 periods SMA of $1.87 whereas support could be around the previous week’s low of $1.70.

Stock Recommendation

Considering current trading levels, strong product line and fundamentals as well as strong balance sheet and decent outlook, we give a “Buy” recommendation on the stock at the current market price of $1.75 per share, down 2.23% on 6th May 2021.

3) Fonterra Co-operative Group Limited (Recommendation: Hold, Potential Upside: Low Double-Digit (M-Cap: NZ$7.36 billion, Gross Dividend Yield: 2.193%)

Business Description:

Fonterra Co-operative Group Limited (NZX: FCG) is a dairy company and its brands include Anchor, Anmum, Anlene, NZMP and Farm Source.

Outlook

As per the management, farmgate milk prices will be in the range of $7.30-7.90 per kgMS in H2FY21 and expects normalised earnings of 25-35 cents per share. Further, the dairy business has seen resilient performance in a COVID-19 world as the product is stapled in consumer’s diets around the world and demand is robust. The mid-point of $7.60 per kgMS would contribute over $11.5 billion to the New Zealand economy. However, rise in raw milk prices will put pressure on sales margins in H2FY21.

Also, Fonterra has commenced the consultation process in order to seek farmer feedback on the potential options to change the capital structure which could give the farmers financial flexibility.

Technical Overview:

Weekly Chart

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock came under selling pressure after it made a ‘Double Top’ at $5.15 pushing it down to $4.35, correcting close to 50% retracement level of $4.07. For the ongoing week, it has given a softer close amidst low volatility at $4.56. Technical indicator RSI with a reading around 49 and a flattish curve at the end, suggests flattening of bullish momentum for the stock.

Going forward, the stock may have resistance around $4.90 whereas support could be around the 38.2% retracement level of $4.48.

Stock Recommendation:

Considering the current trading levels, restructuring of business strategy for future period, wide presence of business across geographies and current business momentum, we give a “Hold” rating on the stock at the current market price of $4.56, on 6th May 2021.

4) T&G Global Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$355.37 million, Gross Dividend Yield: 2.835%)

Business Description:

Located in 13 countries, T&G Global Limited (NZX: TGG) is engaged in fresh fruit and vegetables business. It has ~2,500 people who grow and partner with over 1,200 growers to market, sell and distribute fresh produce to customers in over 60 countries.

Outlook

Amid persistent challenges due to COVID-19 circumstances, the company was able to build on the foundations laid over the previous 2 years and reported a strong profit result for the financial year ended 31st December 2020. In December, the company announced the sale and leaseback of 8.03 hectare Nelson coolstore and packhouse site. The sale proceeds were reported at $50.5 million that will be used for growing business in global markets, developing and acquiring new genetics, and investing in physical assets and technology.

Despite the fact that the industry is vulnerable to the turmoil of extreme weather condition, the company is confident that the investments done in people and systems will establish a strong platform for future long term growth.

Technical Overview:

Weekly Chart

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has been trading in a ‘Rectangle Channel’ pattern provided by the previous high of $3.00 on the upside and a 23.6% retracement level of $2.88 on the downside with the potential breakout at upside for the past several weeks. For the ongoing week, the stock has given a softer close at $2.90. The technical indicator RSI with a reading around 50, suggests bullish momentum for the stock.

Going forward, the stock may have resistance level around $3.00 whereas support could be around $2.88.

Stock Recommendation

The stock has a 52-week low and high of $2.51 and $3.00, respectively. The stock has increased by ~8.2% in 6 months and ~3.6% in 9 months. Further, revenue grew at a compound annual growth rate (CAGR) of 9.8% over FY17-FY20, with cash and cash equivalent at $44.7 million as on 31 December 2020.

Considering resilient business model, strong product penetration across geographies, prudent capital management, and decent outlook, we give a “Hold” recommendation on the stock at the current market price of $2.90 per share, down by 1.36% on 6th May 2021.

Note: Investment decision should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...