I. Sector Landscape and Outlook

As per the Ministry of Housing and Urban Development (HUD), the government planned a $3.8 billion Housing Acceleration Fund (HAF) focused on scaling homebuilding. The focus is to develop a mix of private-sector and government-led developments in areas with the highest housing supply and affordability challenges.

As per HUD, an additional 278 transitional housing places became available in the September 2021 quarter, with 4,710 places secured for tenanting. Compared to September 2020, total public homes have grown by 2,490 homes. Further, the number of applicants from the Housing Register placed in public housing has fallen by 21% to 1,201 applicants. Meanwhile, the Housing Register has grown by less than 1% QoQ and 15% YoY.

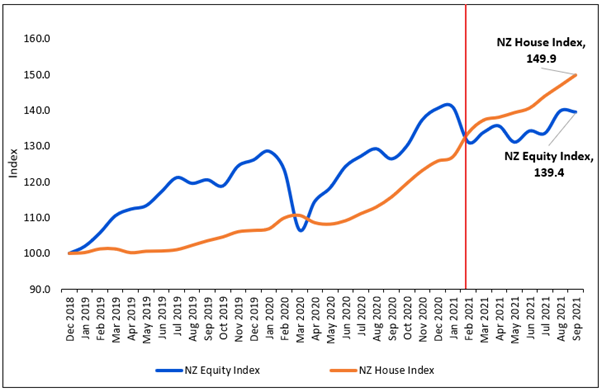

NZ Housing Index Continue to Surpass Equity Index in September 2021

As per the Reserve Bank of New Zealand (RBNZ), housing prices in NZ have continued to accelerate since the onset of COVID-19, indicating the international low-interest-rate environment, good domestic economic conditions, and persistent supply constraints. Market momentum has been retained at a solid level while at a slightly slower pace in recent months. Valuation metrics like price-to-rent ratios indicate that prices are vulnerable to fall as interest rates rise from their recent lows. The momentum in population growth and new housing supply suggests that housing market pressure at a high level over the past decade could soften. New building activity is picking the pace at record high levels, despite COVID-19 related circumstances, while population growth has slowed phenomenally since border restrictions were put in place.

Exhibit 1: Trend in Equity Index vs House Index in NZ – Since Dec 2018 to September 2021

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

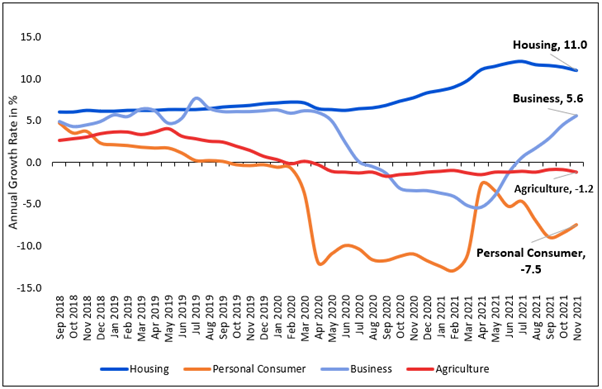

Housing Lending Again Surpassed Business and Other Lending in November 2021

RBNZ's total housing lending stock expanded by $2.5 billion (0.8%) in November 2021, including a $2.3 billion (0.7%) rise for banks & $152 million (3.2%) rise for NBLIs. Meanwhile, the annual increase in lending decreased from 11.4% to 11.0% in November 2021. In addition, the total personal consumer lending stock was up by $323 million (2.4%) in November 2021, and annual growth improved from -8.5% to -7.5%. Further, the entire business lending stock increased for the seventh consecutive month, up by $1.1 billion (0.9%) to $123.1 billion, and the annual growth rose to 5.6%. On the other hand, total agriculture lending fell by $177 million (-0.3%), with its yearly growth at -1.2% from -0.9% in November 2021.

Exhibit 2: Trend in Lending Since September 2018 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

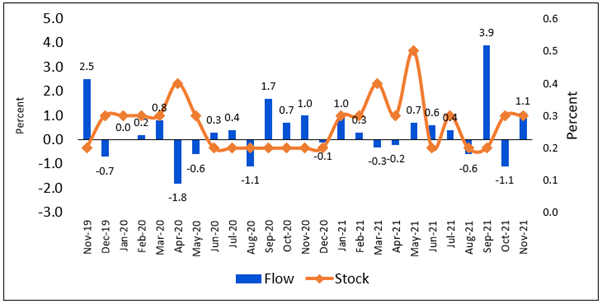

Rise in Rental Price Indexes – Changes in Prices That Households Pay for Housing Rentals

As per Stats.NZ, the index for the stock measure of rental property prices, increased 0.3% MoM in November 2021. In line with this, the index for the flow measure of rental property prices grew 1.1% MoM in November 2021. Also, the stock index rose by 3.5% YOY in November 2021, and the flow index increased by 5.9% YOY in November 2021. The flow measure captures the fluctuation in rental price only for dwellings that have a new tenancy started in the reference month, as it tends to be more volatile than the stock movement. This indicates rental price changes across the whole rental population, including renters currently in tenancies.

Exhibit 3: Trend in Monthly Percent Change in Rental Price Indexes, Nov 2019–Nov 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Real Estate (Sector) Index generated a 1-year return of ~2.38% versus ~-1.21% by the S&P/NZX 50 Index. Therefore, NZX All Real Estate Index overperformed NZX50 Index by ~3.59% in 1-year.

Exhibit 4: S&P/NZX All Real Estate (Sector) vs S&P/NZX50 Index

Source: REFINITIV

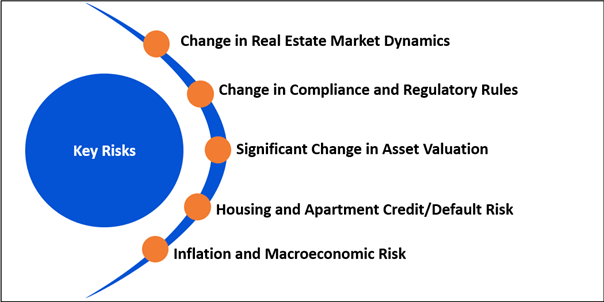

Key Risks and Challenges:

As per Stats.NZ, the seasonally adjusted total building volume in September 2021 quarter decreased 8.6% QoQ, residential volume decreased 6.4% QoQ, and non-residential decreased 12%. At the same time, total building value stood at $7.2 billion, up 5.2% QoQ. This indicates a slowdown in pace from previously high levels seen post COVID-19 pandemic outbreak. Also, in October 2021, the seasonally adjusted number of new dwellings consented decreased 2.0%, after sliding 2.0% in September 2021. However, in the year ended October 2021, the actual number of new dwellings consented stood at 47,715, up 26% YoY.

As per RBNZ, the robust demand for housing builds a price pressure, hurting borrowers’ pockets as they must borrow more relative to their income. Loan-to-value ratio (LVR) restrictions are the primary tool to address the housing market's risks. Vacancy rates have a modest rise, which could accelerate as current tenancies come up for reassessment, primarily for less attractive sites.

Exhibit 5. Key Risks in Real-Estate Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the ‘Homelessness Action Plan’, the government’s initiatives will provide shelter to over 10,000 individuals, families, and whanau who are at risk or experiencing homelessness. This initiative is backed by over $300 million government funding and built on phenomenal investment in the ‘Housing First’ programme and continued investment in public housing. Further, the action plan to address homelessness (from 2023) will continue to expand on the progress made, bridge the gaps, and ensure that all NZs have stable and affordable places to live.

As of 30 September 2021, public housing homes stood at 74,825, including 64,211 Kāinga Ora and 10,614 registered Community Housing Provider properties. During the quarter ended 30 September 2021, 1,248 of 3,968 households were accepted into the Housing First Programme.

As per RBNZ, the household sector has survived the pandemic quite well. However, the level and trajectory of house prices is unsustainable and creating risks for recent buyers. In property development, enhanced threats are emerging, especially for small and medium-scale residential projects.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Stride Property Ltd & Stride Investment Management Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.11 billion, Gross Dividend Yield: 6.045%)

Business Description:

Stride Property Ltd & Stride Investment Management Ltd (NZX: SPG) consists of Stride Investment Management Limited (SIML) and Stride Property Limited (SPL). SIML is an investment manager and staff employer for the group company, and SPL owns the property portfolio and has an ownership interest in each of the Stride portfolios.

Outlook

The company’s investment management strategy will continue to achieve further growth across its investment management business. To achieve this growth, the company will strengthen its existing products and enhance these portfolios and investor returns. Further, the company aims to reduce LVR to 29.8% after the successful completion of the capital raising offer. Meanwhile, the company’s board forecast a combined cash dividend per share for SPL and SIML for FY22 of 9.91 cps.

On 16 December 2021, the company announced the completion of refinancing bank debt facilities across a consortium of six banks, which increased total facilities available from $455 million to $600 million.

On 15 December 2021, the company advised that its $20 million retail offer was oversubscribed, that received applications for $23.9 million. The company has decided to accept all additional applications.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering proper guidance for FY22 and a solid focus to enhance the portfolios and investor returns.

For relative valuation, peers like Kiwi Property Group Ltd (KPG.NZ), Precinct Properties New Zealand Ltd (PCT.NZ), and Argosy Property Ltd (ARG.NZ), among others, have been considered.

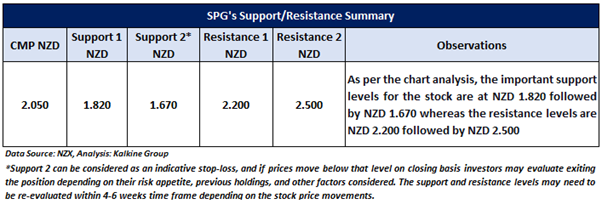

Considering the factors above, we give a “Buy” recommendation on the stock at the current market price of $2.05 per share as of 23rd December 2021 (New Zealand Time: 1:35 PM (GMT +12).

2) Asset Plus Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$110.63 million, Gross Dividend Yield: 7.077%)

Business Description:

Asset Plus Limited (NZX: APL) is a listed property investment management company that manages a property portfolio of commercial and industrial buildings in major cities of NZ.

Outlook

As per the management, the trend in the occupancy market will be a key focus area for the year ahead. The quality portfolio is sound, and its balance sheet is conservatively geared. Further, the company has sufficient funds for green Value Add opportunities. The focus area in the business in FY22 will be on the core operational elements – including addressing key expiries and remaining rent reviews, leasing up remaining vacancies and developments. As outlined in the FY21 annual results, starting 1 April 2022, the policy will be to pay dividends between 85-100% of AFFO.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

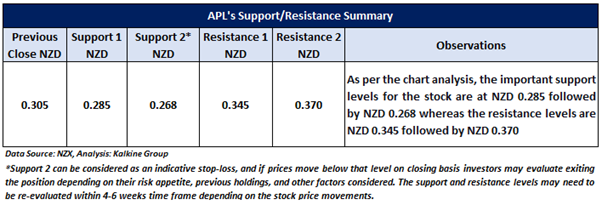

Considering the factors above, we give a “Buy” recommendation on the stock at the closing market price of $0.305 per share as of 23rd December 2021.

3) Goodman Property Trust (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.57 billion, Gross Dividend Yield: 2.512%)

Business Description:

Goodman Property Trust (NZX: GMT) is engaged in owning, developing, and managing industrial real estate globally, including logistics facilities, warehouses, and business parks.

Outlook

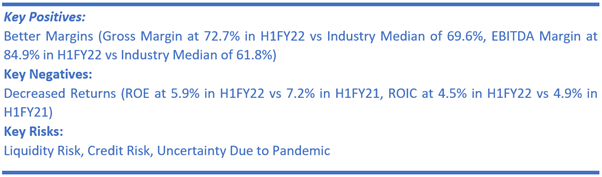

The company has adapted to the ongoing circumstances of COVID-19 and delivered another robust operating result in H1FY22. However, the economic outlook is still uncertain, and the company remains well established for sustainable long-term growth. A superior-quality portfolio focused on urban logistics is expected to benefit from the structural trends that are growing demand for distribution facilities close to consumers. With a minimal loan to value ratio of 17.5% and only partially drawn debt facilities as of 30 September 2021, the company retains over $300 million of available liquidity for future investment.

On 23 December 2021, the company announced that it had acquired a 3.2-hectare infill site in Albany and secured a development agreement with NZ Post. The new site has a 17,992 sqm parcel processing centre, to be developed on Bush Road in Albany.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

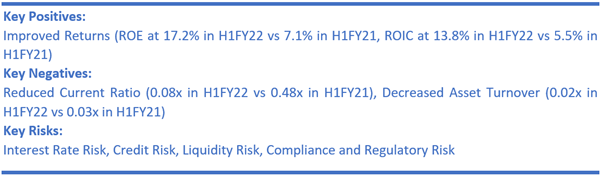

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight discount has been applied to P/E Multiple (NTM) (Peer Average), considering a decrease in gross margin at 83.4% in H1FY22 versus 85.1% in H1FY21 and missing clear guidance for FY22.

For relative valuation, peers like Precinct Properties New Zealand Ltd (PCT.NZ), Asset Plus Ltd (APL.NZ), and PEXA Group Ltd (PXA.AX), among others, have been considered.

Considering the fact above, we give a “Hold” recommendation on the stock at the closing market price of NZ$2.555 per share, down 1.73% as of 23rd December 2021.

4) Argosy Property Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.33 billion, Gross Dividend Yield: 4.336%)

Business Description:

Argosy Property Limited (NZX: ARG) is involved in investing and managing properties, including office, industrial and retail properties across New Zealand.

Outlook

The company's quality portfolio remains in good shape, and its balance sheet is conservatively geared. The company has sufficient facility headroom to develop near-term projects and act on strategic opportunities. The key focus for the rest of FY22 includes emphasis on the business's core operational elements, such as addressing key expiries and remaining rent reviews, leasing up remaining vacancies, and developments. Further, it will advance its green Value Add projects pipeline and focus on driving earnings and capital growth. Besides, the company has reconfirmed the FY22 dividend forecast of 6.55 cents per share with the new dividend policy to start from 1 April 2022.

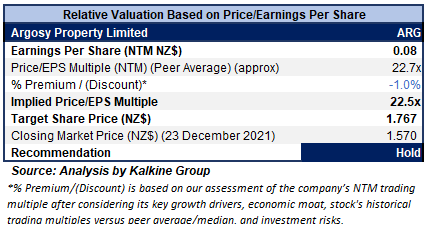

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

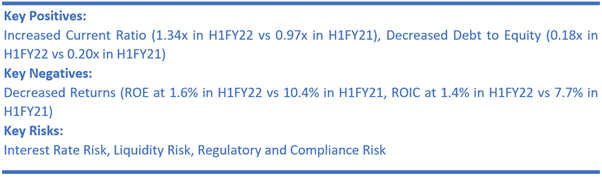

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight discount has been applied to P/E Multiple (NTM) (Peer Average) considering a lower current ratio at 0.26x in H1FY22 versus the industry median of 0.67x and higher Debt to Equity at 0.51x in H1FY22 versus the industry median of 0.41x.

For relative valuation, peers like Property for Industry Ltd (PFI.NZ), Kiwi Property Group Ltd (KPG.NZ), Precinct Properties New Zealand Ltd (PCT.NZ), among others, have been considered.

Considering the factors above, we give a “Hold” recommendation on the stock at the closing market price of NZ$1.57 per share, down 0.63% as of 23rd December 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...