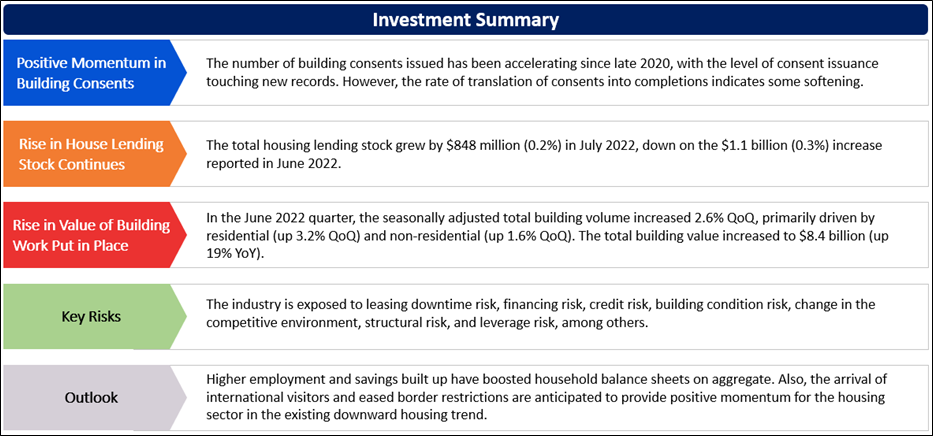

As per the Reserve Bank of New Zealand’s (RBNZ) ‘Monetary Policy Statement’ in August 2022, the inflation levels are elevated in most countries due to shared international influences, with similar economic patterns across inflation subcomponents such as food, transport, and housing. Further, the aggregate demand has pushed inflation to a new high across a broad range of goods and services, followed by supply-chain and war-related disruptions, which are adding to the future path of inflation. Meanwhile, house prices are anticipated to slow the household spending growth due to the fall in wealth and higher mortgage interest payments. Further, it expects house prices to fall back to April 2021 levels, while the size and speed of the fall are highly uncertain.

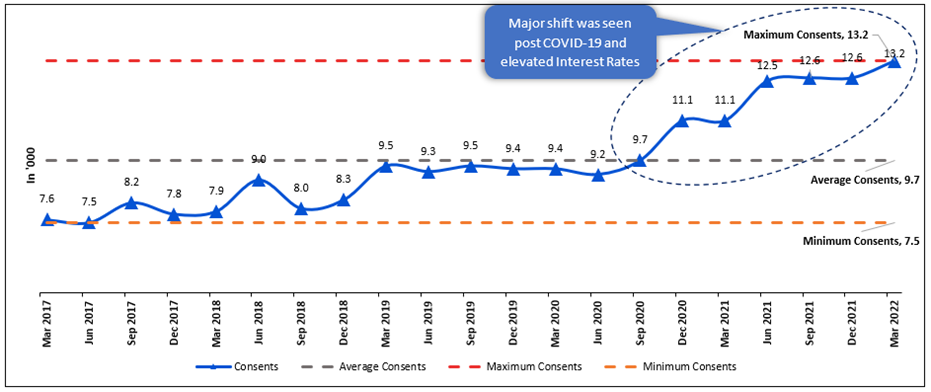

Momentum in Building Consents Touching New Highs

As per RBNZ, the number of building consents has been accelerating since late 2020, with consent issuance touching a new record. However, the translation rate of consents into completions indicates some softening, and the level of new consents has fallen slightly in recent months. Further, the construction sector's acute labour and materials shortfall has limited activity and added to inflationary pressures.

Exhibit 1: Trend in Building Consents Since March 2017

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

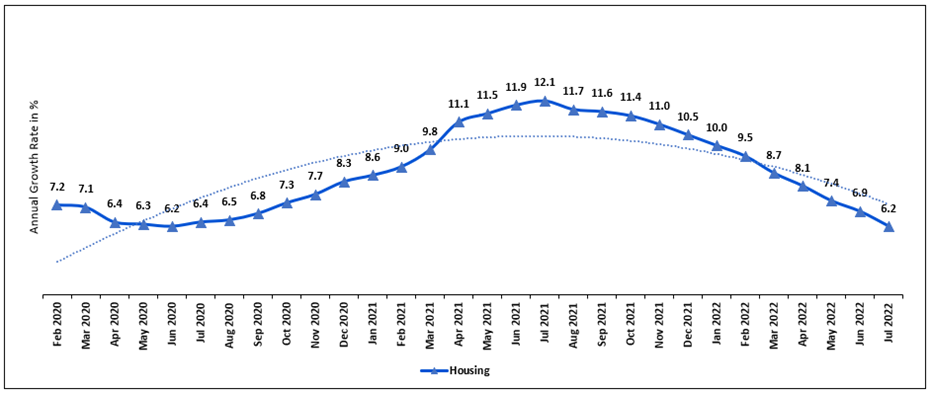

House Lending Stock Continued to Growth in July 2022

As per RBNZ, the total housing lending stock grew by $848 million (0.2%) in July 2022, down on the $1.1 billion (0.3%) increase reported in June 2022. Annual growth continued to slide to 6.2%, from 6.9% reported in the previous month, the twelfth consecutive month of weak annual growth. The decline in the housing sector is primarily led by elevated inflation for the past 18 months, which is expected to remain high in the near term. Inflation directly drives interest rates, which govern the lending and borrowing market.

Exhibit 2: Trend in Housing Lending Stock

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

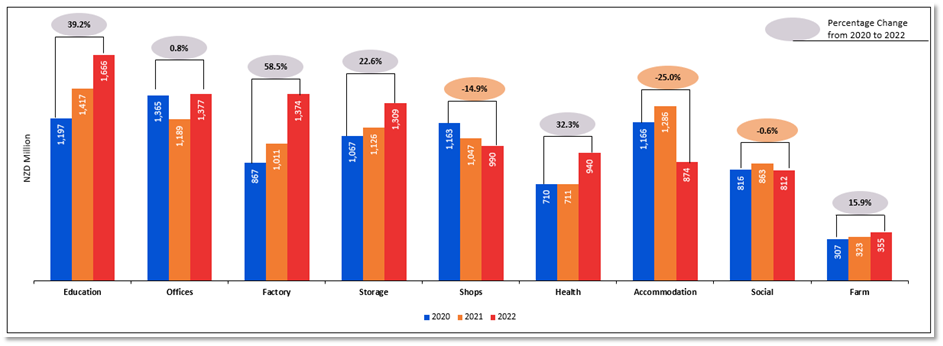

Rise in Value of Building Work Put in Place

As per Stats.NZ, in the non-residential building types with the most work put in place (by value), the education buildings stood at $1.7 billion (up 18% YoY for the year ended June 2022). Similar growth was posted by the offices, administration, and public transport buildings, which stood at $1.4 billion (up 16% YoY). The factories and industrial buildings stood at $1.4 billion (up 36%), and storage buildings stood at $1.3 billion (up 16%). Construction sector activity has remained high, despite a feeble demand outlook led by continuing uncertainty on economic growth.

Exhibit 3: Trend in Value of Building Work Put-in-Place for Non-Residential Buildings, Year Ended June 2020–2022

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Real Estate (Sector) Index generated a 5-year return of ~42.63% versus ~30.05% by the S&P/NZX All Index. Therefore, NZX All Real Estate Index overperformed S&P/NZX All Index by ~12.58% in 5-year.

Exhibit 4: S&P/NZX All Real Estate (Sector) vs S&P/NZX All Index

Source: REFINITIV

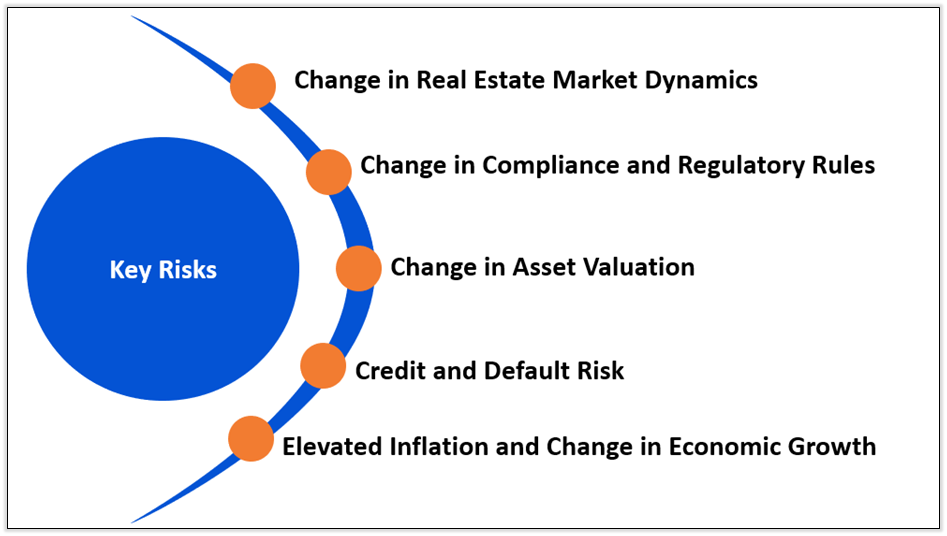

Key Risks and Challenges:

As per RBNZ, house prices decreased by 7.9% post-touching monthly in November 2021. This declining trend is anticipated to continue throughout 2022 and much of 2023, led by sales volumes. Meanwhile, the interest rates are expected to ease, and the population continues to grow, which could support the housing sector to some extent. Higher interest rates are expected to slash house price growth and the incentive for new home building over the coming time horizon. Increasing building materials and labour costs are also cutting down the home building activities. However, these pressures are projected to ease gradually depending on economic policies and international growth momentum.

Exhibit 5. Key Risks in Real-Estate Sector:

Source: Analysis by Kalkine Group

Outlook:

As per Stats.NZ, in the June 2022 quarter, the seasonally adjusted total building volume increased 2.6% QoQ, primarily driven by residential (up 3.2% QoQ) and non-residential (up 1.6% QoQ). The total building value increased to $8.4 billion (up 19% YoY). Further, the residential construction prices rose 4.2% in the June 2022 quarter, followed by non-residential prices that grew 3.6% (as measured by the capital goods price index). This fresh set of data indicates continued strength in the sector. High employment and savings built up have boosted household balance sheets on aggregate, which could provide some support to the housing sector. International visitor arrivals indicate that international tourism has strengthened since the border restrictions eased, providing an additional boost to near-term growth. Meanwhile, it is expected that, on average, in the coming five years, house prices will increase by a cumulative 6.5%.

Apart from the sector-specific factors, an analysis on three NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1. Goodman Property Trust (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.09 billion, Annual Dividend Yield (TTM)1: 3.10%)

Business Description:

Goodman Property Trust (NZX: GMT) owns, develops, and manages industrial real estate globally.

Outlook

The group anticipates a rise in FY23 cash earnings by 4% to ~6.9 cents per unit, with a 7% increase in cash distributions to ~5.9 cents per unit. Further, it is anticipated that the sound capital position would deliver robust underlying growth in cashflows. The future development pipeline (greenfield and brownfield sites) is estimated to be over 400,000 sqm of urban logistics space.

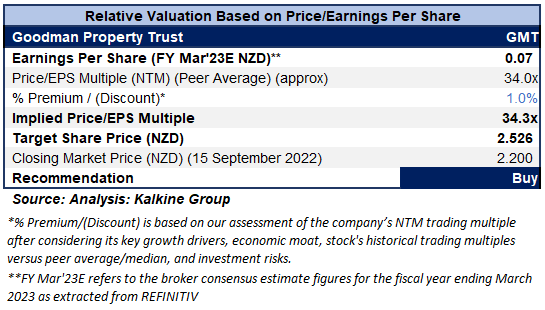

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

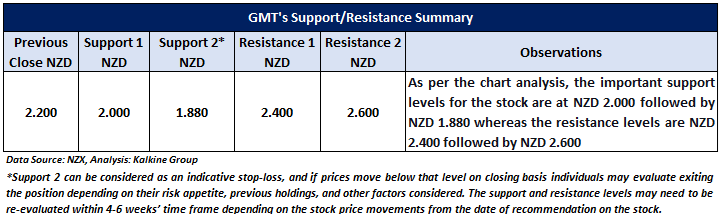

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering its effective operating performance and record statutory profit in FY22, sustained rental growth and continued demand.

Considering the above factors, a ‘Buy’ recommendation on the stock has been provided at the closing market price of $2.20 per share, up 1.85% as of 15 September 2022.

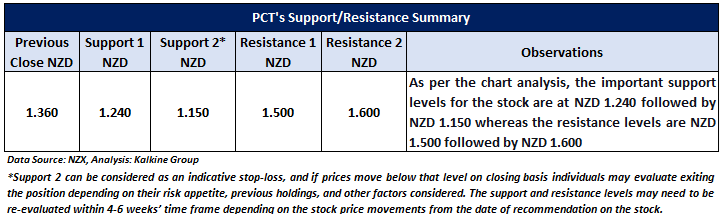

2. Precinct Properties New Zealand Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.16 billion, Annual Dividend Yield (TTM)1: 5.02%)

Business Description:

Precinct Properties New Zealand Limited (NZX: PCT) is the largest owner and developer of premium inner-city business space in Auckland and Wellington.

Outlook

The company will continue to focus on three key pillars, people and partners, operational excellence, and development in the future. Also, it expects to maintain portfolio occupancy, leverage development capability, and partner with direct investors. It is well positioned to create additional value for shareholders and capital partners and expects to provide a dividend of no less than 6.70 cents per share for FY23.

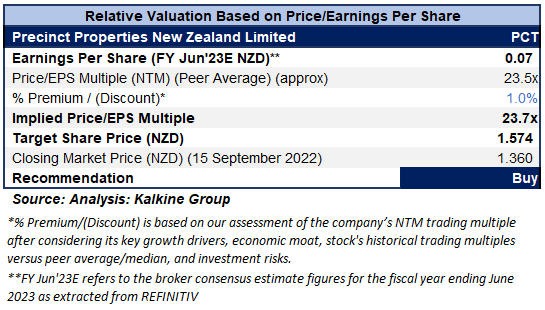

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering a diversified revenue stream and decent outlook.

Considering the above factors, a ‘Buy’ recommendation on the stock has been provided at the closing market price of $1.36 per share, up 1.87% as of 15 September 2022.

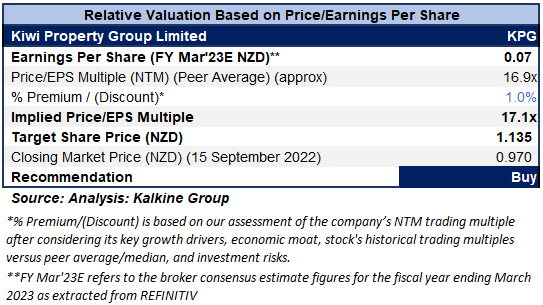

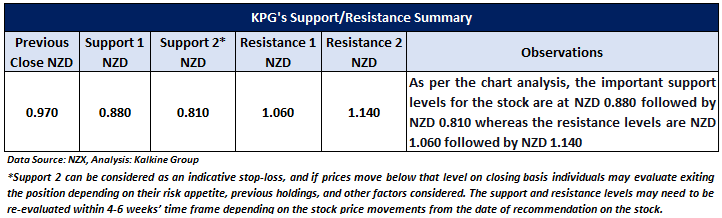

3. Kiwi Property Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.52 billion, Annual Dividend Yield (TTM)1: 7.15%)

Business Description:

Kiwi Property Group Limited (NZX: KPG) is a property company that owns and manages a real estate portfolio comprising retail and office buildings. The company provides a reliable investment in New Zealand property through the ownership and active management of a diversified, high-quality portfolio.

Outlook

The company’s key focus for FY23 will be on launching the CBD office co-investment platform, progressing well on the Sylvia Park BTR and 3 Te Kehu Way developments and managing its assets towards growth. Further, it will also emphasise advancing capital recycling activity in FY23. Meanwhile, it plans a cash dividend of no less than 5.70 cents per share for FY23.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering its healthy FY22 financial results, strategic growth priorities, and healthy balance sheet.

Considering the above factors, a ‘Buy’ recommendation has been provided on the stock at the closing market price of $0.97 per share, down 0.51% as of 15 September 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is September 15, 2022. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Transitional FAP license issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...