1. Sector Landscape and Outlook

As per the Monetary Policy Committee, the existing stimulatory level of monetary settings will be unchanged, keeping the Official Cash Rate (OCR) at 0.25% for now. This was considered after the Government imposed Level 4 COVID restrictions on activity across New Zealand. Moreover, the Committee will monitor the inflation and employment outlook regularly, before deciding on reducing or altogether removing monetary stimulus. Meanwhile, the global monetary and fiscal policies remain accommodative thereby strengthening domestic spending and investment and ensuring larger stability and growth in the economy and financial system.

Stronger Economic Growth in New Zealand than Anticipated

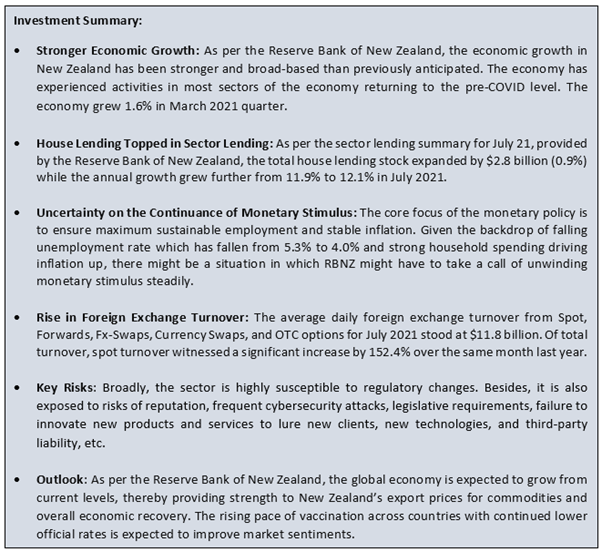

As per the Reserve Bank of New Zealand, the economic growth in New Zealand has been stronger and wider than previously anticipated (Exhibit 1). The economy grew 1.6% in March 2021 quarter, despite a lack of international tourists during what is normally the peak tourism season. However, activity in the retail, healthcare, and construction sectors has been exceptionally stronger. Activity in most sectors has been around pre-COVID-19 levels, with exception of mining and those most exposed to the loss in international visitors (Exhibit 1).

Exhibit 1: Trend in Quarterly Production GDP & Production GDP by Industry

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

House Prices are Above Sustainable Level – Reserve Bank

As per the Reserve Bank of New Zealand, the house prices are above their sustainable level, given the outlook for the supply of, and demand for, housing. The key drivers of housing supply and demand have taken a big shift. The underlying demand for housing has decreased phenomenally, driven by low population growth since the outbreak of COVID-19 last year. Also, the house buildings are at record levels and mortgage interest rates are increasing. The Reserve Bank anticipates house price inflation to moderate in the coming period.

Sector Lending – House Lending Increased in July 2021

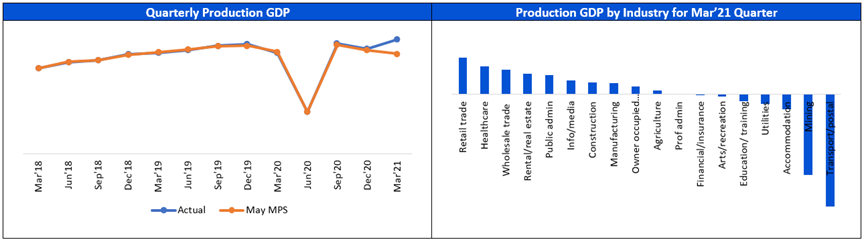

As per the Reserve Bank of New Zealand, total housing lending stock expanded by $2.8 billion (0.9%). Also, the annual growth in lending increased further from 11.9% to 12.1%, whereas total consumer lending stock was down for the third consecutive month by $107 million (-0.8%) and the annual growth increased marginally but remained negative at -4.7%. Meanwhile, the total business lending stock increased for the third consecutive month, up by $323 million (0.3%) and the annual growth moved into positive territory for the first time since Jul’20, rose to 0.6%. Total agriculture lending stock increased by $235 million (0.4%), with its annual growth remaining negative at -1.1%.

Exhibit 2: Trend in Lending Since 2017 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Impact of Official Interest Rates Change on Mortgage Rates

Home loan borrowers start to realize the initial impact of an increase or decrease in official interest rates within a month. However, the highest impact on mortgage rates could take roughly six months. This analysis done by the Reserve Bank of New Zealand indicates that a 1% change in the Official Cash Rate (OCR) ideally moves average two-year mortgage rates by 0.34% within one month. The shift in monetary policy increases over the length of time, with the highest impact on mortgage rates about 6 months after the change in the OCR. At that point, approximately 0.80% (percentage points) of the initial 1% change in the OCR is ideally passed through in higher or lower mortgage rates.

Strong Recovery in Foreign Exchange Turnover

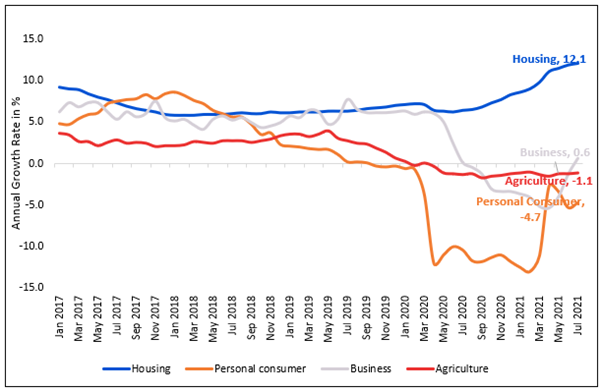

As per the Reserve Bank of New Zealand, the average daily foreign exchange transactions from Dealers, Other financial institutions, and Non-Financial Customers in July 2021 stood at $11,847 million, against $10,277 million in the same month last year. This was mainly driven by a sharp rise in spot transactions. Broadly, the recent recovery in the financial market, improved consumer sentiments, better economic data, controlled COVID-19 circumstances, aggressive vaccination, and easing of border restrictions, helped the continued inflow of foreign exchange in the New Zealand market, which has helped stabilise and grow the economy.

Exhibit 3: Daily Average Foreign Exchange Turnover Trend since July 2020 to July 2021

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Financials Index generated a 1-year return of ~59.65% versus ~11.57% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~48.08% in 1-year.

Exhibit 4: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

Key Risks and Challenges:

The Monetary Policy Committee stated the uncertainty about the emergence of new cases of COVID-19 in the community and the move back into Alert Level 4. The government’s Wage Subsidy Scheme and COVID-19 Resurgence Support Payments are anticipated to buffer the loss of income associated with the lockdown.

Further, the Committee accepts that capacity limitations are building in the economy. Difficulties are especially acute in the labour market, where job vacancies remain high despite a decline in unemployment. Reducing unemployment offers a greater level of confidence on spare capacity is being absorbed. Employment is indicated as at or above its maximum sustainable level in the current environment.

Meanwhile, the Reserve Bank of New Zealand anticipates vulnerabilities in the financial system. The regulator is seeing the impact of lower global interest rates resulting in the higher risk-taking appetite of the consumers and higher asset prices, most visible in higher house prices.

Exhibit 5. Key Risks in Banking and Financial Services Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the Reserve Bank of New Zealand, the economic recovery in New Zealand has been stronger and broader than earlier expected. Activity in most sectors of the economy has returned to pre-COVID-19 levels. However, the recent rise in delta variants of the pandemic might limit economic activities which in turn, depends on the time horizon for restrictions in place and the responses of households and businesses.

Most of the economic growth in recent times has been led by significant spending by households and continued strong demand for commodity exports. Also, multiple small and big businesses are also indicating higher confidence to invest and hire more workers. These factors are expected to strengthen further and provide sustainable growth to the economy and companies, thereby building higher returns on investments for individuals and companies.

As per the Reserve Bank of New Zealand, the global economic outlook continues to better, supporting New Zealand’s export prices for commodities. Broadly, the global monetary and fiscal stimulus remains accommodative to support domestic recovery. Meanwhile, rising vaccination rates across countries are expected to boost confidence in investors communities to undertake investment programme which will give rise to Capex activities thereby sustainable growth to the economy. As of now, aggregate economic activity is above its pre-COVID-19 level in New Zealand, where household spending and construction activity are at elevated levels and are anticipated to continue to grow further.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

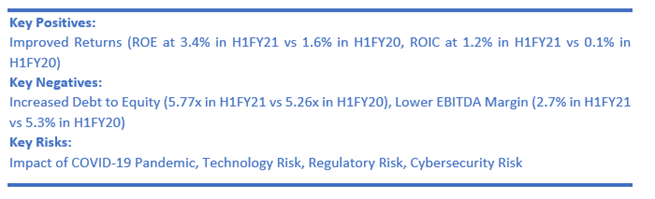

1) AMP Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.88 billion, Gross Dividend Yield: 9.462%)

Business Description:

Founded in 1849, AMP Limited (NZX: AMP) is a wealth management company with an accelerating retail banking business and a growing international investment management business.

Outlook:

The management provided FY21 guidance:

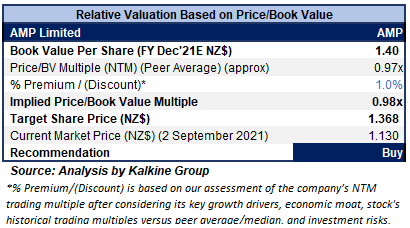

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/BV multiple-based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight premium to its peers’ average, considering the rise in Australian wealth management (AWM) assets under management (AUM) to A$131.2 billion in H1FY21 and a decent outlook for FY21.

For the valuation purposes, we have taken peers such as Tower Ltd. (TWR.NZ), Harmoney Corp Ltd. (HMY.NZ), and Insurance Australia Group Ltd. (IAG.AX) to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $1.13 per share, down 0.88% on 2nd September 2021.

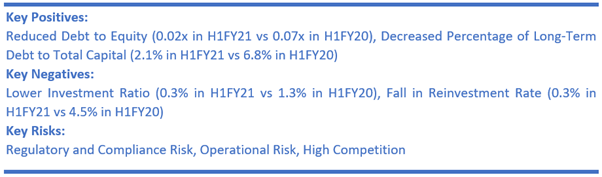

2) Tower Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$290.94 million, Gross Dividend Yield: 3.623%)

Business Description:

Tower Limited (NZX: TWR) is a New Zealand-based insurance company that operates across New Zealand and the Pacific Islands. It is engaged in providing insurance for houses, cars, content, businesses, and more.

Outlook

As per the release dated 28 July 2021, Trade Me plans to continue its six-year partnership with Tower Insurance for at least additional five years. Together these companies will continue to offer insurance to Trade Me’s millions of members and will invest further in new products and digital services.

On the claims front, the company, on 22 July 2021, released an update on claims received following the flood in the West Coast, Wellington, Marlborough, and Auckland regions. The financial impact of previous large events over the year has reached $14 million, this event will be covered by reinsurance to the tune of $7.5 million.

As per the H1FY21 result update, the company anticipates underlying NPAT in the range of $25-$27 million for the year ended 30 September 2021.

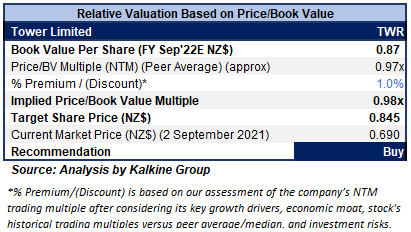

Valuation Methodology: Price/Book Value Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/BV multiple based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight premium to its peers’ average, considering business growth and ongoing reduction in management expenses. Also, the technology and distribution strategy continue to deliver growth with the insurer increasing gross written premium (GWP).

For the valuation purposes, we have taken peers such as Harmoney Corp Ltd. (HMY.NZ), AMP Ltd. (AMP.NZ) and Suncorp Group Ltd. (SUN.AX) to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $0.69 per share, on 2nd September 2021.

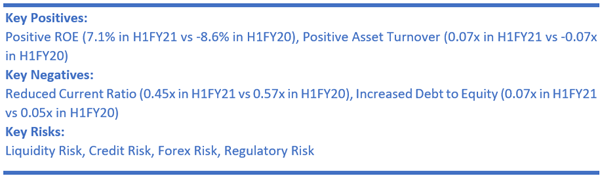

3) Henderson Far East Income Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$965.49 million, Gross Dividend Yield: 7.088%)

Business Description:

Henderson Far East Income Limited (NZX: HFL) aims to offer shareholders an increasing total annual dividend per share, as well as capital appreciation, from a diversified portfolio of investments from the Asia Pacific region.

Outlook

As per the H1FY21 results, announced on 27 April 2021, the management stated a positive outlook for two primary reasons. Firstly, the IMF anticipates growth of 8.6% this year for Emerging and Developing Asia following a decline of 1.0% in 2020. Secondly, the company anticipates a sharp global cyclical recovery that should benefit value shares at the expense of growth shares, perhaps reversing the trend.

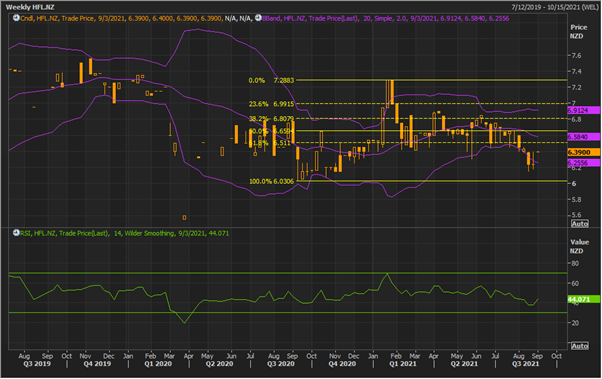

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

Consistent with the previous week of bullish reversal chart pattern of an ‘Inverted Hammer’, the stock gave a gap-up opening for the ongoing week. However, there have been no changes in the stock price, since then. The technical indicator RSI with a reading around 44 and a curve at the end pointing up, suggests the gaining of bullish momentum.

Going forward, the stock may have resistance around the 50% retracement level of $6.66 whereas support could be around $6.20 where a gap on the chart has been created.

Stock Recommendation

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $6.39 per share, on 2nd September 2021.

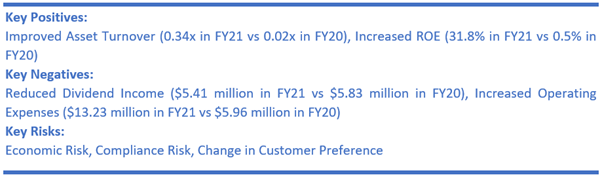

4) Kingfish Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$656.65 million, Gross Dividend Yield: 7.011%)

Business Description:

Kingfish Limited (NZX: KFL) is an investment company with a focus on growing investors' capital through portfolio management and offering regular dividends.

Outlook

As per the management, the company has reported a year of recovery after the COVID impactful performance in FY20. Its focus on investing in agile and prospering companies has again proven the benefits of active investment management and provided shareholders with robust returns. Therefore, the same strategy is expected to continue in the future period.

On 23 August 2021, the company announced a quarterly dividend of 3.52 cents per share with an ex-dividend date of 08 September 2021 and a payment date of 24 September 2021.

As per the July 2021 monthly update, released on 13 August 2021, the company’s gross performance return was down (0.1%), and the adjusted NAV return was down (0.3%).

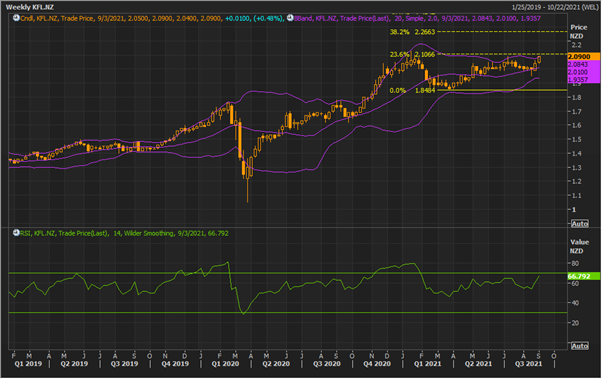

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci projection lines which measure potential price reversal. https://www.bollingerbands.com/

Taking a cue from the previous week of strong closing, the stock opened stronger and has given close at its weekly high of $2.09 for the ongoing week thereby demonstrating resilience. The technical indicator RSI with a reading around 67 and a curve at the end pointing a sharp up, suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around the 38.2% Fibonacci projection level of $2.27 whereas support could be around 20 periods SMA of $2.01.

Stock Recommendation

Driven by the optimism by the management, rebound in market sentiments, current trading levels, and positive long-term outlook, we recommend a ‘Hold’ rating on the stock at the current market price of $2.09 per share, up 0.48% on 2nd September 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...