Company Overview:Kingfish Limited (NZX: KFL) is a New Zealand-based investment company. Westpac Banking Corporation (NZX: WBC) is a banking company that provides the range of consumer, business as well as institutional banking and wealth management services through the portfolio of financial services brands and businesses. Kalkine’s Sector Report covers the Key Financial Metrics, Risks, Outlook, Technical Analysis along with the Valuation, Target Price, and Recommendation on the stocks.

1. Sector Landscape and Outlook

Recently, the Monetary Policy Committee has decided to leave the Official Cash Rate (OCR) at 5.50%. The Reserve Bank of New Zealand stated that the level of interest rates are constraining spending as well as inflation pressure as expected and required. The Committee decided that the OCR would need to be at the restrictive level for the foreseeable future. This is required to make sure that consumer price inflation gets back to the 1% - 3% annual target range, while at the same time helping maximum sustainable employment.

As per the release by RBNZ, the global economic growth is weak as well as inflation pressures are easing. This follows the period of significant monetary policy tightening by central banks internationally. Notably, global inflation rates are declining, supported by the normalisation of international supply chains as well as the fall in shipping costs and energy prices. The weaker global growth resulted in lower export prices for NZ's goods.

Sector Lending Summary – Banks & NBLIs

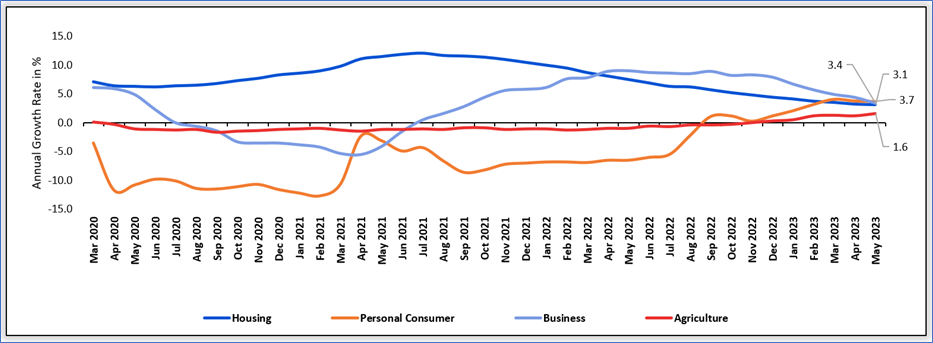

As per RBNZ, housing lending stock witnessed a rise of $799 Mn (or 0.2%) in the month of May 2023, reflecting a rise on the $577 Mn increase which was reported in the prior month, but down on the $1.2 Bn increase which was reported in May 2022. Notably, lending for non-banks witnessed a fall of $133 Mn (-2.3%) the largest monthly fall (break adjusted) on record. Total annual growth fell further from 3.2% to 3.1%.

Personal consumer lending stock fell $52 Mn (or -0.4%) in the month of May 2023, with the annual growth rate falling from 3.8% to 3.7%. The consumer annual growth is the highest across the 4 major lending sectors for the 1st time since June 2018. As per the release by RBNZ, the business lending stock witnessed a fall of $625 Mn (or 0.5%) in May 2023 after rising $627 Mn last month. The annual growth rate fell from 4.4% to 3.4%.

Exhibit 1: Lending Pattern– Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Credit Card Spending Patterns

RBNZ has released credit card summary report, wherein, seasonally adjusted domestic billings on NZ issued cards stood at $3.8 Bn in May, reflecting a fall of 1.9 percentage points from April 2023 as well as seasonally adjusted total billings in NZ declined 2.3 percentage points in May to $4.3 Bn. The overseas billings on NZ issued cards rose from $0.5 Bn to $0.6 billion in May 2023 month. This was the highest value recorded in a month since August 2019.

Total credit limits stood at $21.2 Bn (not seasonally adjusted) in the month of May. This was 0.9% lower than May 2022 as well as the lowest since April 2015. Notably, billings on overseas issued cards utilised in NZ fell from $0.5 Bn to $0.4 Bn, falling for the 2nd consecutive month.

Severe Weather Events- Impact on Insurance Sector

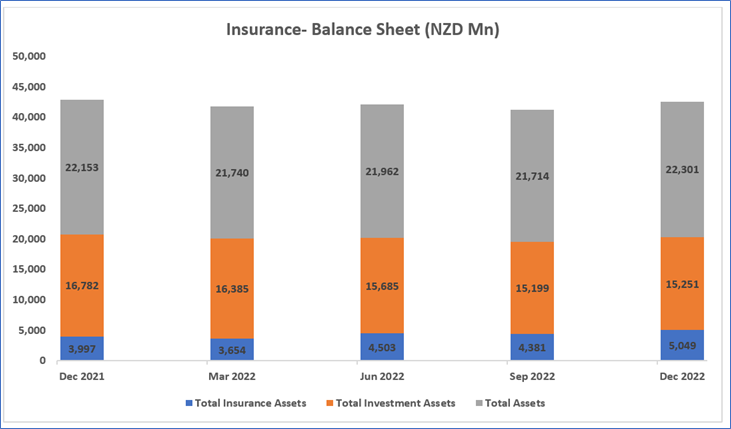

RBNZ, in their Financial Stability Report (May 2023), stated that NZ’s major financial market infrastructures are reflecting high availability as well as resilience, with no significant incidents recorded in the recent months. The insurance sector is still profitable and the solvency ratios are stable. However, some insurers were adversely affected by the severe weather events and investment losses.

Insurers are playing important role in supporting households as well as businesses with the risk management. When 2023 started, there were 2 severe weather events: the Auckland Anniversary floods as well as Cyclone Gabrielle. Since property insurers need to hold reinsurance for the 1-in-1000 year earthquake, which is much more severe than recent weather events, much of the insurance claim costs for these events are covered by reinsurance.

However, insurer profits would be reduced from the reinsurance excesses as well as additional reinsurance premiums would reinstate cover for any future events. The reinsurance premiums at renewal might be much higher, resulting in insurers charging increased premiums to customers. Despite the investment losses as well as the impacts of recent disasters, in aggregate insurers remained profitable, with net profits of $0.7 Bn in the year ended September 2022. In the previous 3 years, annual net profits were about $1.1 Bn.

Exhibit 2: Insurance Balance Sheet (NZD million)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

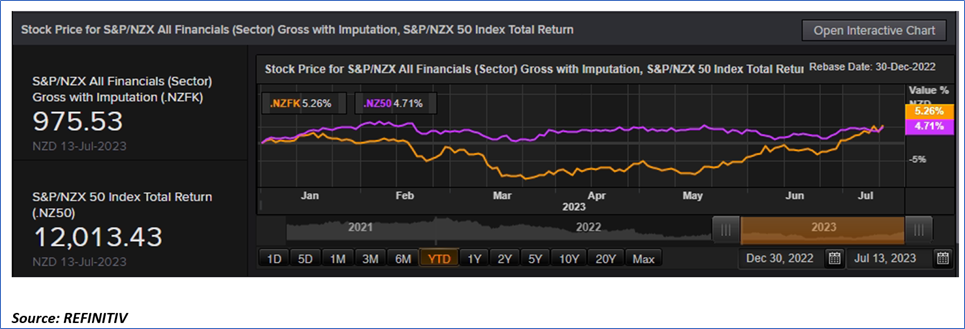

The S&P/NZX All Financials Index generated a YTD return of ~5.26% versus ~4.71% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~0.55% on the YTD basis.

Exhibit 3: S&P/NZX All Financials Index vs S&P/NZX 50 Index

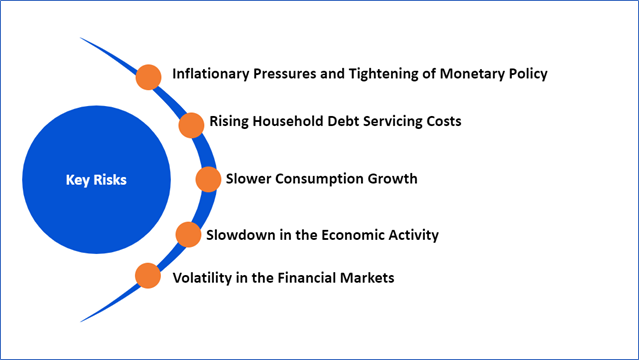

Key Risks and Challenges:

As per RBNZ, increased number of downside risks to the global economic outlook are present. According to the recent release by RBNZ, the global economic growth remains below the trend for most of the trading partners, partly because of significant monetary policy tightening by the central banks internationally. Notably, the global growth is expected to weaken further. Economic growth is moderating more rapidly in China and the recent data suggested a slowing in broader economic momentum.

Exhibit 4. Key Risks in Financial Sector:

Source: Analysis by Kalkine Group

Outlook:

The sound as well as efficient financial system with the capability to absorb shocks is fundamental to the health of the broader NZ economy. Financial institutions remained resilient in the past 6 months. Bank profitability continued to recover as well as capital levels are being increased in preparation for the upcoming regulatory requirements. However, banks are expecting greater pressure on borrower debt serviceability in the coming year, driven by weaker economic conditions as well as higher interest rates. Positively, the financial system is well positioned to withstand higher credit losses and continue to supply credit.

In New Zealand, inflation is anticipated to continue to fall from its peak, and with it measures of inflation expectations. Core inflation is anticipated to fall as capacity constraints ease. Even though employment is above the maximum sustainable level, there are signs of labour market pressures dissipating and vacancies declining. The repair and rebuild underway in the regions of the North Island because of severe weather events would be helping economic activity in the near term. Broader government spending is expected to fall in inflation-adjusted terms as well as in proportion to GDP. The Committee remained confident that with interest rates staying at restrictive level for some time, consumer price inflation would return to within its target range of 1 - 3% per annum, while supporting maximum sustainable employment.

The labour shortages have started to ease, partly in response to the recent arrival of migrants. Firms have reported that it is becoming easier to find labour and economy-wide vacancy rates have declined. The committee judged that after the recent falls, house prices are around sustainable levels. Notably, house prices stabilised in recent months and the Committee mentioned that the outlook for the housing market is more balanced.

Higher net migration has been supporting the demand for housing but increased interest rates continue to put downward pressure on housing demand.

Apart from the sector-specific factors, an analysis on two NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Kingfish Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 445.4 Mn, Annual Dividend Yield (TTM)1: 9.04%)

Outlook:

Notably, FY 2023 was yet another challenging period for the NZ share market. Notwithstanding the changeable market conditions, the directors of the company are confident in the strategy of focusing towards well-managed, quality businesses, whose sustainable competitive advantages allow them to adapt as well as respond to ever-changing environment over the medium to long term. The company’s portfolio companies continued to focus towards positioning themselves to create future value for the shareholders.

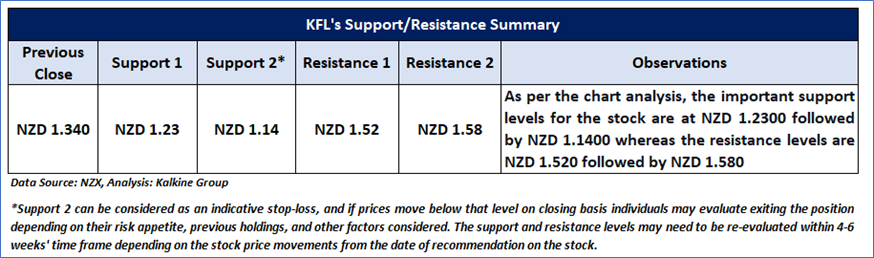

Technical Overview:

Technical Commentary:

On the daily chart, KFL stock price witnessed a breakout of the falling trendline resistance zone. Moreover, the momentum oscillator RSI (14-period) is showing a reading of ~53.167 level, indicating positive momentum. Further, the prices are trading above the trend-following indicators 21-period SMA, which may act as a support zone. An important support level for the stock is placed at NZD 1.23 while the key resistance level is placed at NZD 1.52.

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 1.340 per share as on 13th July 2023.

2) Westpac Banking Corporation (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 81.2 Bn, Annual Dividend Yield (TTM)1: 6.89%)

Outlook:

With respect to H2 FY 2023 considerations, the bank is focused towards maintaining cost discipline as well as is expecting risk and regulatory costs, wages and inflation to remain elevated. WBC is having conservative balance sheet settings and is expecting to maintain capital above operating range. This would also provide for the future capital management. The bank is having robust financial position which provides it flexibility and the focus is towards cost reset. At the macro level, the loan portfolios are healthy. Most mortgage customers are ahead on repayments and the offset balances were little changed and mortgage delinquency levels are low.

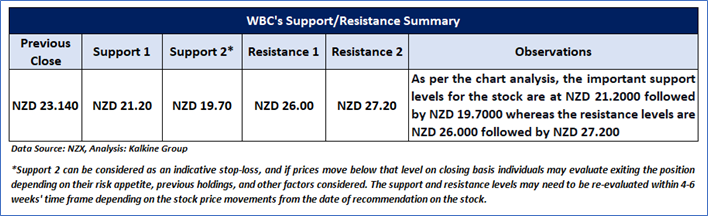

Technical Overview:

Technical Commentary:

On the daily chart, WBC prices are trading near the rising trendline support zone. Moreover, the momentum oscillator RSI (14-period) is showing a reading of ~53.730 level. Further, the prices are trading above the trend-following indicators 21-period SMA, which may act as a support zone. An important support level for the stock is placed at NZD 21.2 while the key resistance level is placed at NZD 26.0.

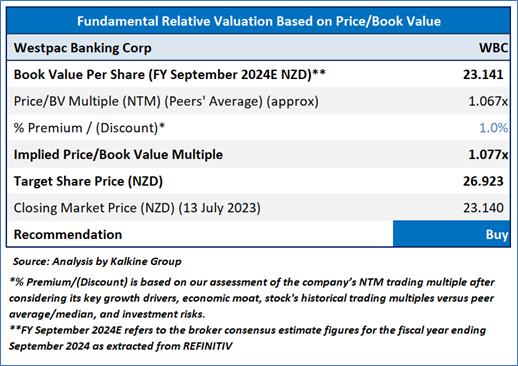

Fundamental Valuation:

Price/BV Based Relative Valuation

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 23.140 per share, up by 0.17% as on 13th July 2023.

Disclaimer: Kalkine New Zealand Limited’s (Kalkine) Director Kunal Sawhney owns shares of Westpac Banking Corporation since December 2021. Kalkine has recommended Westpac Banking Corporation in its report as general advice only (under FSP Number FSP691351).

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is July 13, 2023. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...