I. Sector Landscape and Outlook

As per ‘New Zealand Immigration,’ a part of the Ministry of Business, Innovation, and Employment (MBIE), the technology sector is diverse and advanced. It has developed itself to the global industry standards and competes successfully on the world platform. The industry is a critical and growing business in NZ, contributing ~8% for GDP and employing 5% of the workforce. Moreover, the exports have grown to reach $7.4 billion in 2019, making tech the country’s third-largest export sector.

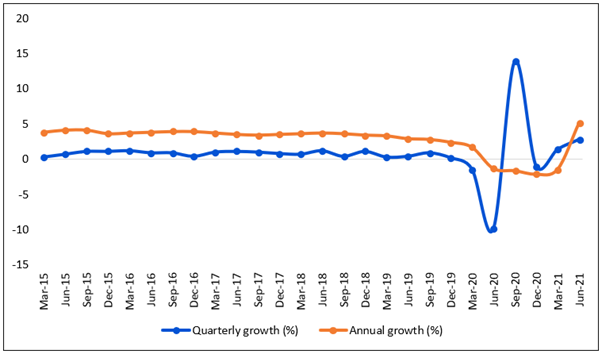

Service Industry Continue to Lead the June 2021 Quarter GDP Growth Momentum

As per Stats.NZ, GDP for June 2021 quarter versus March 2021 quarter grew by 2.8%, mainly contributed by primary industries that increased 5.0%, followed by service industries' growth of 2.8%, which make up ~2/3rd of the economy. In addition, business services increased 4.8% in the June 2021 quarter, mainly driven by increased scientific, architectural, and engineering services. This growth was the fourth back-to-back quarter of growth for the business services industry.

Exhibit 1: GDP Quarterly and Annual Rates, March 2015 – June 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Accelerating Demand for IT Professionals in NZ

According to New Zealand Immigration, NZ’s tech sector has over 20,000 firms, primarily small businesses, employing over 114,000 people. According to the industry study, employers forecast that they will require 4k-5k new digital technology professionals every year in the near future. As a result, employers have highly depended on attracting people from overseas to access the digital skills they require. As per the report, ~3,683 immigrants were granted visas for IT occupations in 2019, reflecting over 80% of new digital technology jobs created. Further, in 2014-19, 27,057 visas were granted for professionals entering NZ to work in ICT occupations.

Deployment under MBSF is forecasted to increase geographic mobile coverage by 20-30%

As per MBIE, the mobile coverage currently includes areas where 95%+ of NZ’s live and work. However, the existing geographic coverage is ~50%. The deployment under Mobile Black Spot Fund (MBSF) is anticipated to increase geographic mobile coverage by 20-30%, up from 50%. In addition, private network operators offer mobile and broadband coverage.

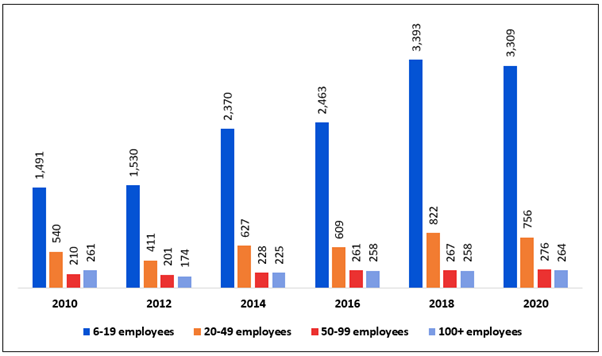

Rising Trend in Both dial-up (ISDN and Analog) and Broadband Connections by Business Size

As per Stats.NZ, the dial-up (ISDN and Analog) and broadband connections by business size having 6-19 employees grew from 1,491 in 2010 to 3,309 in 2020, followed the businesses having 20-49 employees that increased to 756 in 2020 from 540 in 2010. Further, the businesses having 50-99 employees grew to 276 in 2020 from 210 in 2010, followed by the growth in businesses having 100+ employees to 264 in 2020 from 261 in 2010. This growth momentum indicates a significant increase in smaller firms than a business having 100+ employees.

Exhibit 2: Trend in Both dial-up (ISDN and Analog) and Broadband Connections

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Index Performance:

The S&P/NZX, All Information Technology Index, generated a 2-year return of ~43.61% compared to ~20.17% by the S&P/NZX 50 Index.

Exhibit 3: The NZX, All Information Technology Index, overperformed NZX50 Index by ~23.44% in a 2-year period:

Source: REFINITIV

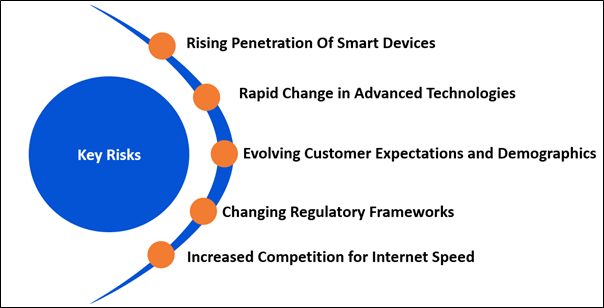

Key Risks and Challenges:

The information technology industry is exposed to risks that include cybersecurity, information security, IT systems development projects, IT governance, outsourced IT services, social media use, mobile computing, IT skills among internal auditors, emerging technologies, board, and audit committee technology awareness.

Further, with the risk of monopolistic behavior in the telecommunications sector, the NZ Commerce Commission plays a crucial regulatory role. The regulatory policies have evolved in recent years to mirror technological changes and have regulatory frameworks for areas such as wholesale fibre services or copper line wholesale services.

Exhibit 4. Key Risks in IT and Communication Services Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the Wellbeing budget 2021, the government has assigned $44 million for ‘Small business digital training, advisory and support programme’. This initiative will facilitate a partnership with the private sector to provide a two-year nationwide program to supply core digital business skills training to NZ small businesses.

As per the report by MBIE, artificial intelligence (AI) has the potential to increase NZ’s GDP by up to $54 billion by 2035. This is because the AI can read vast amounts of data, automate the same type of work, speed & accuracy in decision making, cost reduction, and optimize business processes, among other factors.

Meanwhile, the fear of COVID-19 related circumstances worked in favor of fixed broadband providers, which are expected to reach more miniature cities and towns in NZ now. Average fixed broadband usage per month grew by 77GB this year to 284GB, as per ‘Commerce Commission New Zealand.’ This indicates an increase of 37% compared to 2019, when the growth rate was 15%. In 2020, 14% of residential on-account subscribers bought uncapped ‘endless’ or ‘unlimited’ mobile bundles, increasing 7% in 2019. Similarly, 8% of business on-account subscribers purchased uncapped mobile bundles in 2020, up 2% in 2019.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Chorus Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.86 billion, Gross Dividend Yield: 5.494%)

Business Description:

Chorus Ltd (NZX: CNU) is a telecommunications infrastructure company. It is engaged in building and managing an open-access internet network and rolling out ultra-fast broadband for phone and broadband providers by providing access to its network to deliver its products and services.

Outlook

The company extends its focus to enhance its fibre network. As a result, it is witnessing steady progress towards achieving 1 million fibre connections by 2022 compared to 871,000 active fibre connections in FY21. In addition, the UFB2 rollout remains ahead of schedule, with the fibre network currently 95% complete. Meanwhile, the company expects its FY22 EBITDA to stay in the ambit of $640-$660 million and capital expenditure between $550-$590 million in FY22. Moreover, it has guided for an initial dividend of 26 cents per share for FY22.

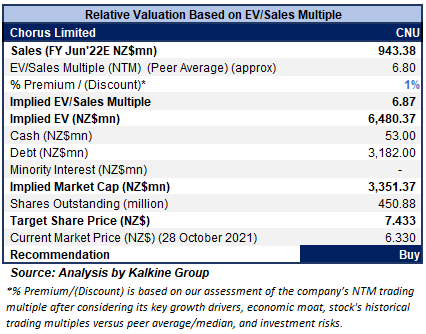

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using EV/Sales based relative valuation (on an illustrative basis), and the target price so arrived reflects a rise of low double-digit (in % terms). In addition, a slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average), considering its higher EBITDA margin at 69.0% in FY21 versus the industry median at 32.3% and continued acceleration in fibre uptake.

For relative valuation, peers like Spark New Zealand Ltd (SPK.NZ), Swoop Holdings Ltd (SWP.AX), and Uniti Group Ltd (UWL.AX), among others, have been considered.

Considering the aforementioned factors, a “Buy” recommendation has been assigned on the stock at the current market price of $6.33 per share as of 28th October 2021 (New Zealand Time: 12:29 PM (GMT +12).

2) PaySauce Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$42.23 million)

Business Description:

PaySauce (NZX: PYS) is a SaaS employment solutions provider which allows business owners to pay and manage employees accurately and efficiently with the help of iOS, web, and Android applications.

Outlook

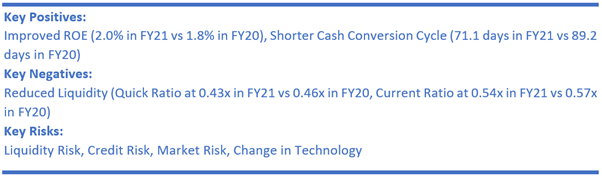

The company has revived its strategies in the last 12 months, which is expected to bring rewards to it in the coming years. It has introduced more innovative systems, made intelligent, data-driven choices, and expanded its product significantly with the addition of Rosters. Moreover, it plans to continue its transition from payroll app to fintech and pursue opportunities to accelerate growth in new and existing markets.

As per the September 2021 quarter, recurring revenue grew 44% YoY and 22% QoQ. Also, it added over 300 customers to the PaySauce platform in the September quarter and processed over $100 million of payroll in September 2021.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

.png)

Stock Recommendation:

Considering the facts above and future development plans, we give a “Speculative Buy” recommendation on the stock at the closing market price of $0.305 per share, down 4.69% as of 28th October 2021.

3) Vital Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$23.68 million, Gross Dividend Yield: 4.789%)

Business Description:

Vital Limited (NZX: VTL) offers a wide range of innovative services and enables critical communications across New Zealand. The company aims to provide the most connected, seamless, integrated networks and absolute coverage at locations.

Outlook

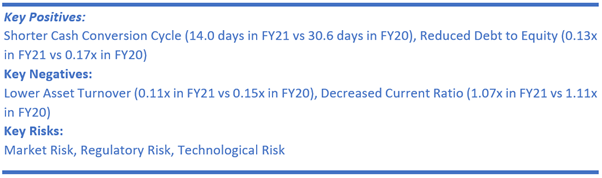

The management is pleased with the growth in both revenue and profit in FY21, despite subdued H2FY21 versus H1FY21. Capital expenditure for FY21 was $8.28 million, including the upgrade of the St John Ambulance radio network. Further, the company expects capital spending to the tune of $5.3 million, with $3.0 million of this funded by customers in FY22. Meanwhile, debt increased to $14.39 million in FY21 from $12.14 million in FY20, which is forecasted to increase 3-5% over the next 12 months.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

.png)

Stock Recommendation

Considering the aforesaid facts, current trading level, and risks associated with the stock we give a “Speculative Buy” recommendation on the stock at the closing market price of $0.57 per share, down 1.72% as of 28th October 2021.

4) Smartpay Holdings Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$200.16 million)

Business Description:

Smartpay Holdings Limited (NZX: SPY) is Australia and New Zealand’s largest independent full-service EFTPOS (Electronic Funds Transfer at Point of Sale) provider.

Outlook

As per the Q2FY22 trading update, Australian acquiring transactional revenue extended to show strong growth in the September quarter, reflecting an upside of 58% YoY. In addition, the consolidated revenue for H1FY22 was up 45% YoY to $21 million, with Australian acquiring transactional revenue up 99% YoY to $12.6 million.

The management expects the transacting terminals and associated revenues to grow further in the post-COVID-19 era. The company looks forward to ongoing improvement in Australian acquiring revenues driven by easing restrictions and returning customers to trading.

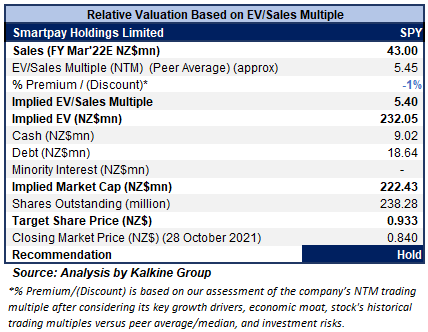

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using EV/Sales based relative valuation (on an illustrative basis), and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight discount has been applied to EV/Sales Multiple (NTM) (Peer Average), considering a negative ROE at -80.8% in FY21 versus the industry median of +0.4% and a negative EBITDA margin at -18.2% in FY21 versus the industry median of 20.3%.

For relative valuation, peers like Pushpay Holdings Ltd (PPH.NZ), Computershare Ltd (CPU.AX), and Rhipe Ltd (RHP.AX), among others, have been considered.

Considering the aforementioned factors, a “Hold” recommendation has been assigned on the stock at the closing market price of $0.84 per share, down by 3.45% as of 28th October 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

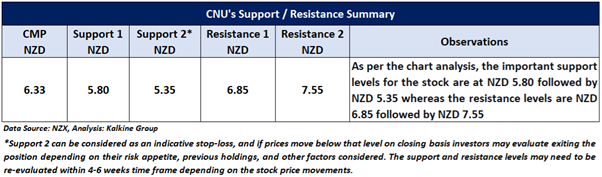

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...