I. Sector Landscape and Outlook

As per the Ministry for Primary Industries (MPI), the stellar performance in the primary industry is expected to augment food and fibre export revenue to reach $52.2 billion for the year to 30 June 2022. Dairy export revenue is estimated to rise by 13% to reach $21.6 billion despite a projected decline in milk production of 4%. Further, the horticulture export revenue is anticipated to increase by 2% to $6.7 billion in the year to 30 June 2022, mainly led by large kiwifruit crops and improved export prices for wine. However, disruption due to the Russia-Ukraine war, elevated inflation, rise in key rates by central banks, lower corporate capital expenditure and tepid demand could provide some risk to future growth.

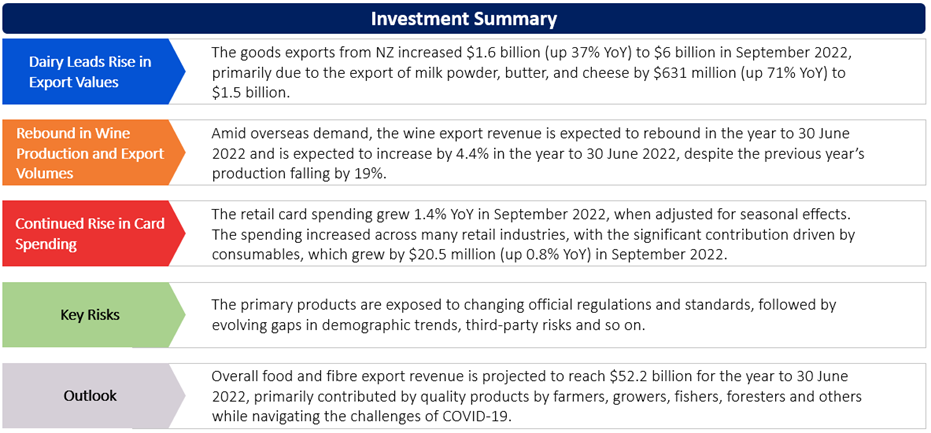

Dairy Leads Rise in Export Values in September 2022

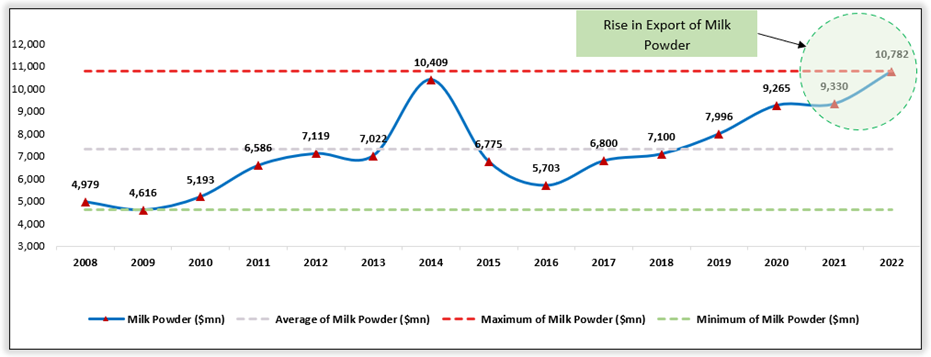

As per Stats.NZ, Goods exports from NZ increased $1.6 billion (up 37% YoY) to $6 billion in September 2022, primarily due to a rise in the export of milk powder, butter, and cheese by $631 million (up 71% YoY) to $1.5 billion. Among this, milk powder grew $221 million (up 48%) in value to $685 million, supported by a 21% rise in quantity and a 22% rise in the unit value. Meanwhile, cheese grew by $122 million (up 112% YoY) to $231 million, supported by a quantity rise of 59% and a unit value rise of 34%.

Exhibit 1: Trend in Milk Powder for the Year 2008-2022 (Year Ending September)

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

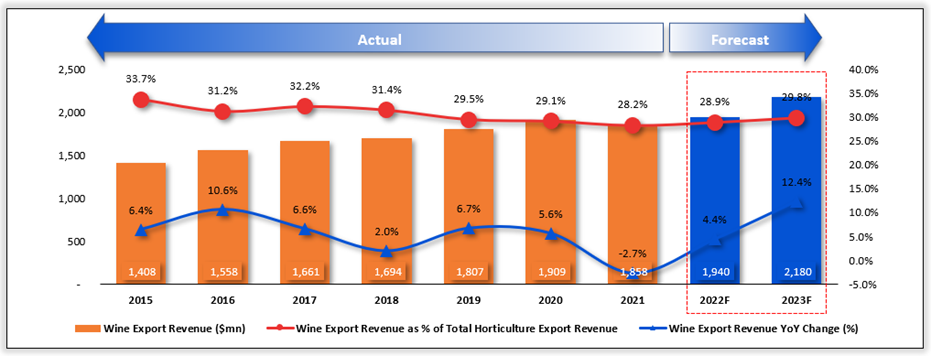

Rebound Expected in Wine Production and Export Volumes

As per MPI, amid overseas demand, the wine export revenue is expected to rebound in the year to 30 June 2022. Export revenue is expected to increase by 4.4% in the year to 30 June 2022 despite the previous year’s production falling by 19%. This is driven by wineries and exporters drawing down inventories to sustain sales volumes and the stiff supplies contributing to much higher prices. Overseas demand is anticipated to remain strong from the prime export destinations (US, UK, EU, Australia and Canada), which could increase export revenue by 12% in the year to 30 June 2023 to $2.2 billion.

Exhibit 2: Trend in Wine Export Revenue 2015–23Forecast (F) (Year to 30 June, NZ$ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

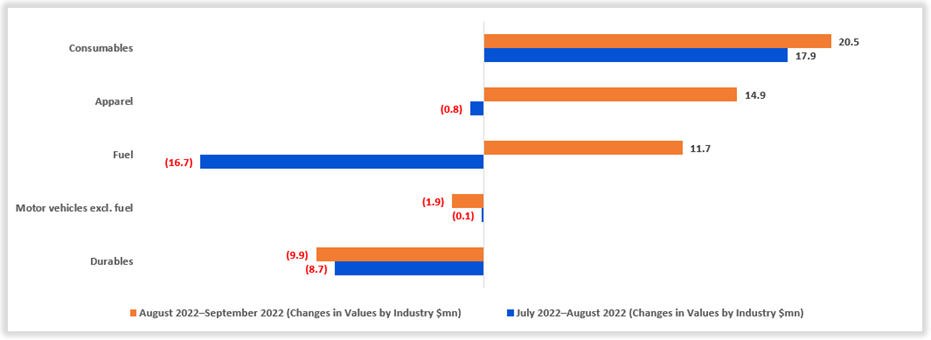

Continued Rise in Card Spending in September 2022

As per Stats.NZ, retail card spending grew 1.4% YoY in September 2022, when adjusted for seasonal effects. The spending increased across many retail industries, with the significant contribution driven by consumables, which grew by $20.5 million (up 0.8% YoY) in September 2022. Consumables comprised items like groceries (supermarkets) and liquor. Individuals continue to spend more on items like food and liquor, resulting in a third consecutive monthly rise for consumables. However, prices for a few food items have been increasing in the past few months, which can impact the momentum build in card spending on groceries.

Exhibit 3: Trend in Changes in Seasonally Adjusted Retail Card Transaction Values by Industry

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

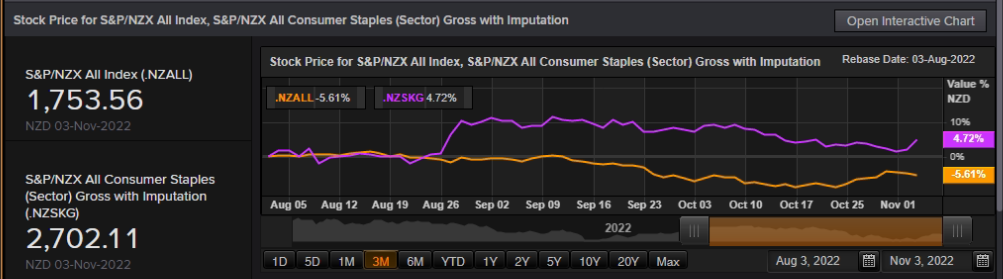

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 3-month return of ~4.72% versus ~-5.61% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~10.3% in 3 months.

Exhibit 4: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

Source: REFINITIV

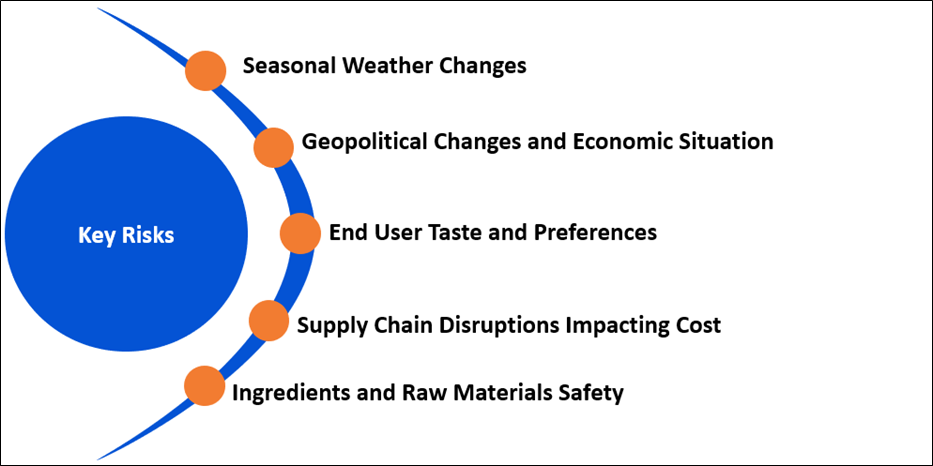

Key Risks and Challenges:

Farmers, growers, and fishers have been challenged by gradual changes in climate in the past years, thereby impacting the quality of items and customers. Further, challenges at warehousing and logistics are pushing up the cost for items, thereby impacting product margins without adding any value. For wine products, in Marlborough, land bank favourable for conversion to viticulture is gradually scarce, restricting further expansion opportunities.

Exhibit 5. Key Risks in Consumer Staples Sector:

Source: Analysis by Kalkine Group

Outlook:

As per MPI, overall food and fibre export revenue for the year to 30 June 2022 is estimated to touch $52.2 billion. All dairy product categories except infant formula are anticipated to outperform their 5-year average in terms of export earnings. Similarly, the wine industry is expected to spur due to relatively better export demand. After the maturity of the 2022 vintage, exports are projected to increase as quickly as congested supply chains allow, with export volumes estimated to reach a record 318 million litres. The strategy is focused on improving the value-added goods and capturing new export destinations.

Apart from the sector-specific factors, an analysis on three NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1. The a2 Milk Company Limited (Recommendation: Hold, Potential Upside: High-Single-Digit) (M-Cap: NZ$4.45 billion)

Business Description:

The a2 Milk Company (NZX: ATM) is the dairy nutritional company, fuelled by the purpose to pioneer the future of dairy for good.

Outlook

The company advised that the United States (US) Food and Drug Administration (FDA) notified ATM that it has exercised its discretion to allow ATM to import infant milk formula (IMF) products into US. The company is of the view that the US represents huge opportunity to develop its brand in the IMF category over the long term. The company made positive start to the year and Q1 FY 2023 sales are expected to be slightly ahead of plan which is mainly implying the benefit of favourable foreign exchange due to depreciation of NZD.

Valuation Methodology: Price/EPS Multiple Based Relative Valuation (Illustrative)

.png)

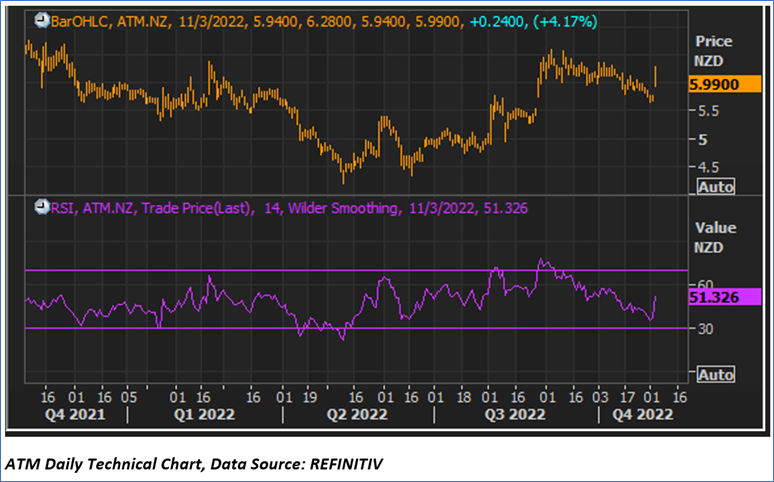

Technical Overview

Daily Price Chart

Stock Recommendation

The stock has been valued using Price/EPS multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of high-single-digit (in % terms). A slight premium has been applied to Price/EPS Multiple (NTM) (Peer Average) considering the decent outlook as well as the recent FDA approval.

Considering the aforementioned factors, a ‘Hold’ recommendation has been assigned on the stock at the closing market price of NZ$5.990 per share, up by 4.17% as on 3rd November 2022.

2. Delegat Group Limited (Recommendation: Buy, Potential Upside: Low Double-digit) (M-Cap: NZ$1.00 billion, Annual Dividend Yield (TTM1): 2.78%)

Business Description:

Delegat Group Limited (NZX: DGL) operates in the global wine industry. It has established Oyster Bay as a leading global Super Premium wine brand as well as owns Barossa Valley Estate in Australia.

Outlook

The company is planning to grow sales by 21% to 4,080,000 cases over the time span of next 3 years. The main driver of the planned growth is Oyster Bay sales in North America. With regards to the 2023 year, it is planning to increase sales by 9% to 3,672,000 cases as well as is forecasting Operating Net Profit after Tax to be between $60 Mn - $64 Mn. DGL would continue to monitor as well as manage the potential impact of ongoing supply chain disruption.

Valuation Methodology: Price/Cash Flow Per Share Multiple Based Relative Valuation (Illustrative)

.png)

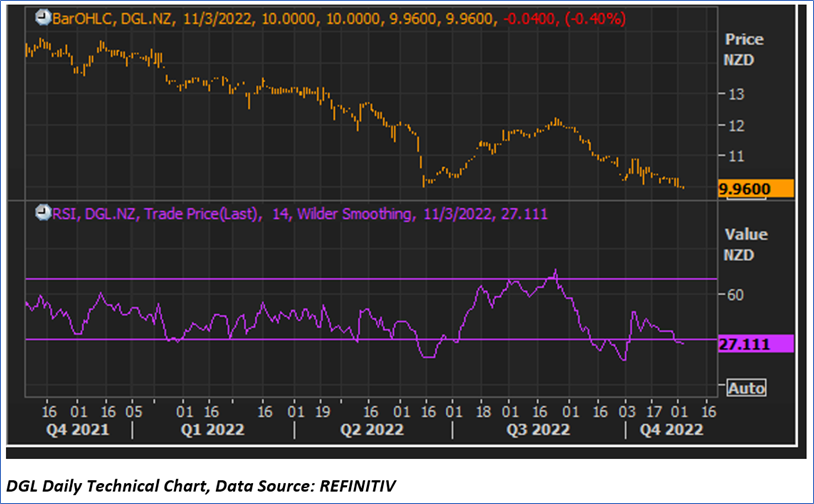

Technical Overview

Daily Price Chart

Stock Recommendation

The stock has been valued using Price/Cash Flow per share multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low-double-digit (in % terms). A slight premium has been applied to Price/Cash Flow per share Multiple (NTM) (Peer Average) considering the decent outlook as well as expectations to increase sales.

Considering the aforementioned factors, a ‘Buy’ recommendation has been assigned on the stock at the closing market price of NZ$9.960 per share, down by 0.40% as on 3rd November 2022.

3. Foley Wines Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-digit) (M-Cap: NZ$89.4 million, Annual Dividend Yield (TTM1): 4.15%)

Business Description:

Foley Wines Limited (NZX: FWL) is the collection of iconic wineries as well as brands from NZ’s most acclaimed wine regions.

Outlook

FWL’s premiumisation strategy is the critical success factor in uncertain times. However, FWL is well-positioned to continue to build on the platform set as it has good inventory levels as well as some exceptional global relationships. At the same time, the company has been seeking out new opportunities in NZ and around the world. Its new development in Martinborough at the Te Kairanga winery is the major investment which is expected to have a significant influence on the profitability.

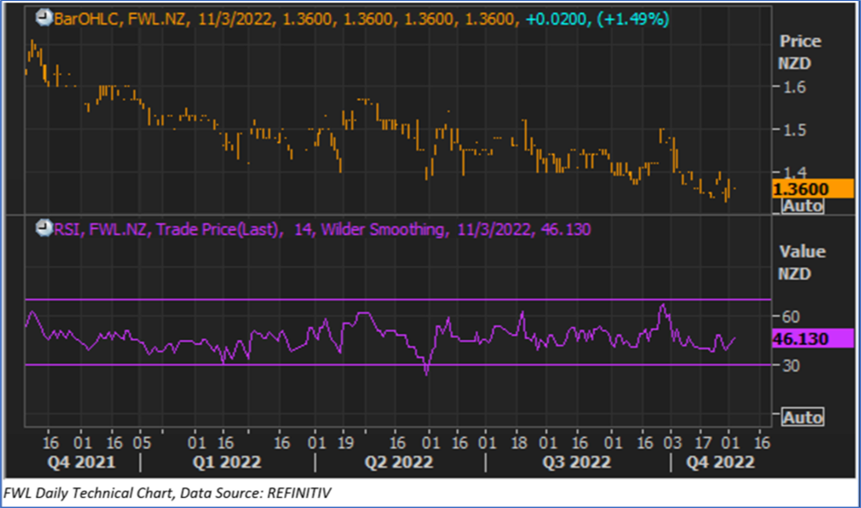

Technical Overview

Daily Price Chart

Stock Recommendation

FWL’s 55-hectare purchase of the Zebra Bendigo Vineyard in Central Otago takes it to the total of 644 hectares which is either owned or leased. FWL is continuing to deploy towards vineyard productivity. FWL firmly believed that the execution of its premiumisation strategy would support in mitigating the consequence of the economic impact.

Considering the aforementioned factors, a ‘Speculative Buy’ recommendation has been assigned on the stock at the closing market price of NZ$1.360 per share, up by 1.49% as on 3rd November 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is November 3, 2022. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Transitional FAP license issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...