Comvita Limited (NZX: CVT) is a New Zealand engaged in the manufacturing and marketing of natural health products, apiary ownership and management. Foley Wines Limited (NZX: FWL) is involved in the producing, marketing and distribution of table wines.Kalkine’s Sector Report covers the Investment Highlights, Key Financial Metrics, Risks, Technical Analysis along with the Valuation, Target Price, Outlook and Recommendation on the stocks.

1. Sector Landscape and Outlook

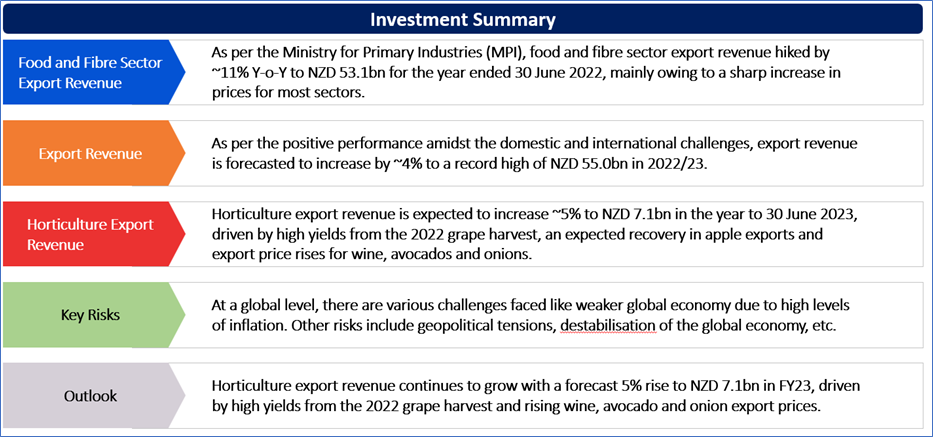

As per the Ministry for Primary Industries (MPI), food and fibre sector export revenue hiked by ~11% Y-o-Y to NZD 53.1bn for the year ended 30 June 2022, mainly owing to a sharp increase in prices for most sectors. As per the positive performance amidst the domestic and international challenges, export revenue is forecasted to increase by ~4% to a record high of NZD 55.0bn in 2022/23. The forecasted percentage has been an upgrade from previous judgement, primarily because of sector’s performance in the market and steep fall in the New Zealand dollar (NZD).

Export revenue for processed food & other products (Includes live animals, honey and processed food) sector is forecasted to reach NZD 3.3bn in the year ending to 30 June 2023, which is up ~3% on pcp basis (NZD 3.226bn). Innovative processed foods and cereal products were the main contributors to this growth.

On the contrary, for FY 2024, the export value is supposed to be declined to NZD 3.06 Bn, mainly owing to impending ban on live cattle exports via sea as of 30 April 2023.

Horticulture export revenue is expected to increase ~5% to NZD 7.1bn in the year to 30 June 2023, driven by high yields from the 2022 grape harvest, an expected recovery in apple exports and export price rises for wine, avocados and onions. On one hand, supply chain issues are easing for most exporters, on the other hand labour supply and rising input costs continue to be headwinds for the sector.

NZ Export Contributors’ Bifurcation for the month of March 2023

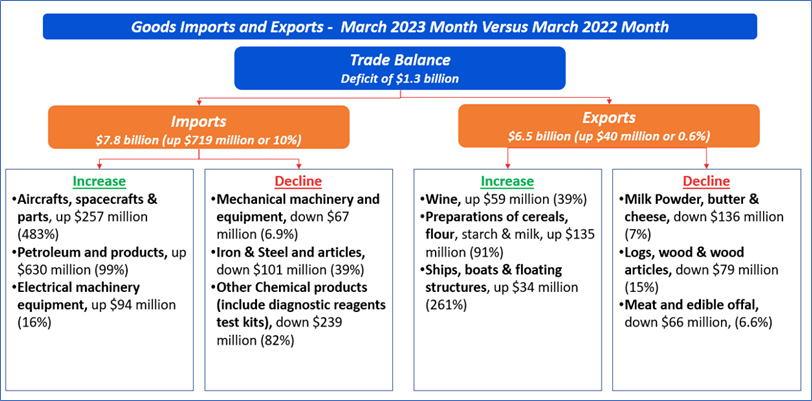

As per Stats.NZ, goods exports increased NZD 40 million (up 0.6% Y-o-Y) to NZD 6.5 billion in March 2023 versus March 2022, primarily driven by the rise in the export of milk powder, butter, and cheese, wine, preparations of cereals, flour, starch, and milk and others like logs, wood, and casein etc. The export rose with all the export partners except China & Japan. Australia led the export marathon by upscaling it to NZD 831mn (30% hike on pcp) in March Month 2023 and followed by EU (Europe Union) with 28% increase on pcp. The monthly trade balance remained as a deficit of NZD 1.3bn and annual deficit as NZD 16.4bn.

Exhibit 1: Detailed Monthly Import & Export Contributors of NZ with Trade Balance

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Horticulture and Honey Export Revenue

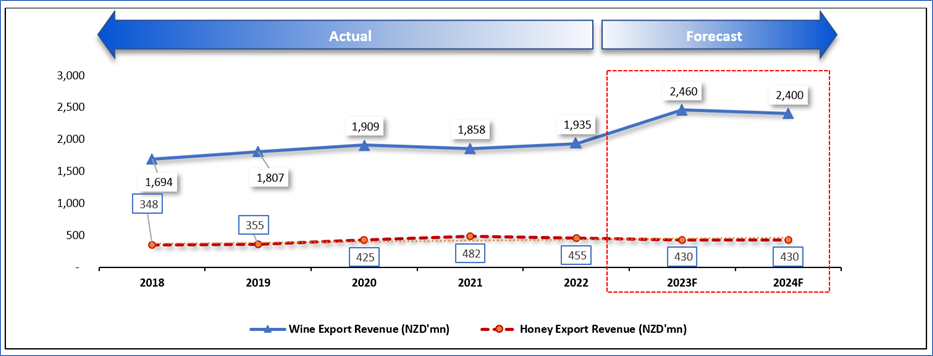

As per MPI, with the easing of supply chain issues, horticulture export revenue for the year ended 30 June 2022 grew ~2% to NZD 6.8 billion and forecast for the period ending 30 June 2023 is a further increase of ~5% rise to NZD 7.1 billion. This is expected mainly because of high yields from the 2022 grape vintage, an expected recovery in apple exports and forecast export price increases for wine, avocados, and onions. Apple and pear crop production for the 2023 is forecasted to recover to 580,000 tonnes (up ~12%) assuming average to unfavourable climatic conditions.

Despite the 7% increase in honey harvest, its export volume and revenue both declined by 11% to 11,320 tonnes and by 6% to NZD 455mn, respectively in FY22. A combination of high honey stocks, labour shortages, increased input costs and the future demand’s uncertainty has led to a reduction in the number of commercial and semi-commercial beekeepers and a reduction in the amount of hives. As a result, honey production is supposed to decline over the next couple of seasons with any gaps being filled by the surplus inventory.

Exhibit 2: Trend in Wine & Honey Export Revenue 2018–24Forecast (F) (Year to 30 June, NZ)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Key Risks and Challenges:

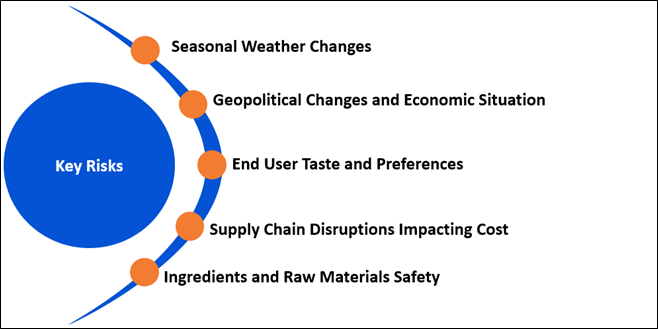

Farmers, growers, and fishers have been challenged by rapid changes in climate in the past years, disrupting the operations and the quality of output. Further, frequent changes in regulatory rules to preserve the environment and reduce carbon are challenging the businesses, warehousing and logistics, thereby impacting product margins without adding any value. Rising input costs, supply chain issues and tight labour environment are other factors that affect the businesses and their operations. Due to technological innovation, interdependency is increasing, resulting in the requirement for capital and technical know-how. For wine products, the land bank expansion is restricted due to the unavailability of fertile fields suitable for good harvesting.

At a global level, there are various challenges faced like weaker global economy due to high levels of inflation. As a result, this causes increase in the cost of living in many countries, destabilisation of the global economy caused by Russia’s conflict with Ukraine and a COVID-19 influenced slowdown in economic growth in China.

Exhibit 3. Key Risks in Consumer Staples Sector:

Source: Analysis by Kalkine Group

Outlook:

Driven from increasing global demand, sector’s in-market work, a strengthening United States dollar (USD) and high commodity prices, export revenue is expected to rise ~4% to NZD 54.9 Bn. Despite the forecast increases in the export revenue for all the sectors in 2022/23, the margins would be affected for most sectors due to high input costs. A further drop in shipping costs is anticipated as COVID-19 issues have resolved. The increased availability and falling costs of containers will aid New Zealand exports return to the markets, unlike previously non-competitive in past. The drop in prices would also enable a transfer of some of the gains across the supply chain both upstream to farmers and downstream to consumers.

Horticulture export revenue continues to grow with a forecast 5% rise to NZD 7.1bn in FY23, driven by high yields from the 2022 grape harvest and rising wine, avocado and onion export prices. The forecast for the year ending June 2024 is expected to increase to NZD 7.66 Bn, where wine is supposed to contribute NZD 2,400 Mn.

The overall honey export revenue is expected to decline by ~6% for the period ending 30 June 2023, because of consumers’ purchasing power deteriorating in key markets, which probably changes consumer appetite for premium honey to cheaper alternatives over the next few seasons. However, prices are expected to remain stable due to exporters’ willingness to hold inventory until demand returns rather than devaluing premium produce. The US became the largest importer of NZ honey in 2021/22, following the 27% rise in revenue to $95 Mn and an 18% rise in volume to 2,292 tonnes. Growth into the US is expected to continue with the falling NZD against the USD.

Apart from the sector-specific factors, an analysis on two NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1 ) Comvita Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 196.401 million), Annual Dividend Yield (TTM)1: 2.709%)

Business Description:

Comvita Limited (NZX: CVT) is a New Zealand engaged in the manufacturing and marketing of natural health products, apiary ownership and management. Its segments include Greater China, Australia and New Zealand (ANZ), Rest of Asia, North America, and Europe, Middle East and Africa (EMEA).

Outlook:

The company expects a double-digit growth of normalised EBITDA in FY23 with the assumption of growth in China market on the back of easing and re-opening of market. With the aim of profitable top and bottom-line growth in focus growth markets, channels and categories, CVT remains on a track to attain EBITDA of ~NZD 50 Mn in FY25. Besides, with the support of recent syndicated banking facility agreement of NZD 115mn with Westpac Bank and the ANZ Bank, the company is all set to launch skincare range with Caravan in 1HFY24. The total addressable market globally is forecasted to grow by over USD 6 Bn (+67%) by 2031.

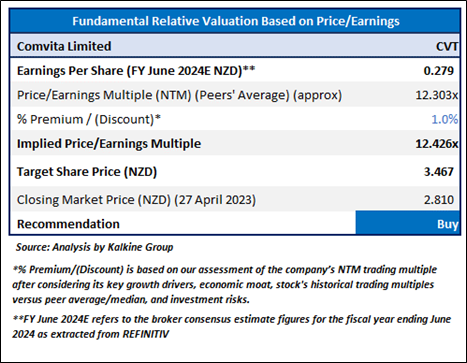

Fundamental Valuation:

P/E Multiple Based Relative Valuation

Technical Overview:

Daily Price Chart

CVT Daily Technical Chart, Data Source: REFINITIV

Note: Purple color line reflects Relative Strength Index (14-Period)

Technical Commentary

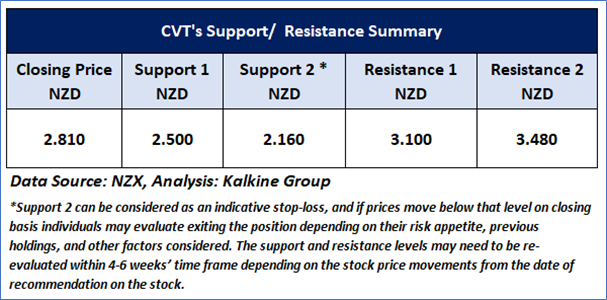

On the daily chart, CVT prices are trading above the falling trendline support level and taking the support from the same. Moreover, the momentum oscillator RSI (14-period) is showing a reading of ~17.453 level. However, the prices are trading below the trend-following indicators 21- period SMA, which may act as resistance zone. An important support level for the stock is placed at NZD 2.50 while the key resistance level is placed at NZD 3.10.

Stock Recommendation

Considering the facts above and undervaluation as indicated by the relative valuation, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 2.810 per share, down by 0.35% as of 27 April 2023.

2 ) Foley Wines Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 86.772 million, Annual Dividend Yield (TTM)1: 4.241%)

Business Description:

Foley Wines Limited (NZX: FWL) is involved in the producing, marketing and distribution of table wines. It deals into New Zealand and various export markets. The Company offers various wine brands, including Martinborough Vineyard, Te Kairanga, Lighthouse Gin, Vavasour, Grove Mill, Mt Difficulty, Goldwater, Dashwood, Russian Jack and Sauvignon Blanc.

Outlook:

Over the years, FWL has built some material global partnerships and focus on finding new routes to that will aid in navigating through the head winds in the global economy, and in particular those partners who can sell a premium portfolio. FWL focuses on quality underpinned by its premiumisation strategy. The company is soon going to open the development in Martinborough in the coming months, which will be acting as a key strategic initiative in the journey of building the Te Kairanga, Martinborough Vineyard and Lighthouse Gin brands.

Technical Overview:

Daily Price Chart

FWL Daily Technical Chart, Data Source: REFINITIV

Note: Purple color line reflects Relative Strength Index (14-Period)

Technical Commentary

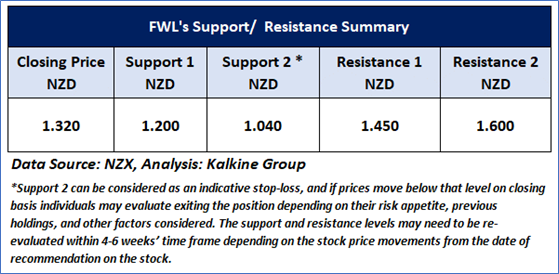

On the daily chart, FWL prices are trading above the horizontal trendline support level. Moreover, the momentum oscillator RSI (14-period) is showing a reading of ~44.041 level. Further, the prices are trading below the trend-following indicators 21- period SMA, which may act as a support zone. An important support level for the stock is placed at NZD 1.20 while the key resistance level is placed at NZD 1.45.

Stock Recommendation

As per TTM valuation by using EV/Sales method, the stock is trading at a multiple of 2.5x, lower than industry mean of 3.0x (consumer non-cyclicals). Considering the facts above and undervaluation as indicated TTM valuation method, a ‘Speculative Buy’ recommendation on the stock has been provided at the closing market price of NZD 1.320 per share, up by ~0.76% as of 27 April 2023.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is neither an indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is April 27, 2023. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...