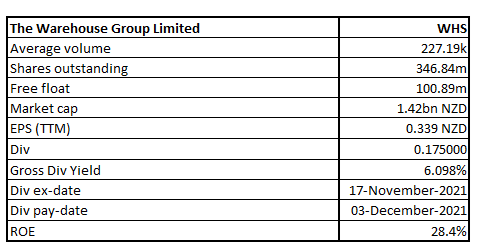

WHS Details

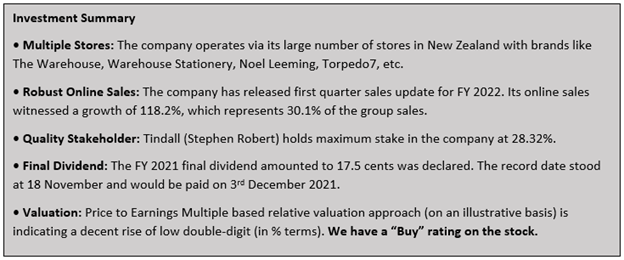

Company Overview: Warehouse Group Limited (NZX: WHS) consists of 6 core retail brands. These brands are The Warehouse, Warehouse Stationery, Noel Leeming, Torpedo7, 1-day and TheMarket. The company is having 260+ retail stores, online stores as well as distribution centres across NZ. Also, the company has 2 overseas sourcing offices which are located in China and India.

The Warehouse Group Limited (NZX: WHS) is one of the largest retailing groups in New Zealand. The market capitalisation of the company stood at ~$1.42 billion on 15th November 2021.

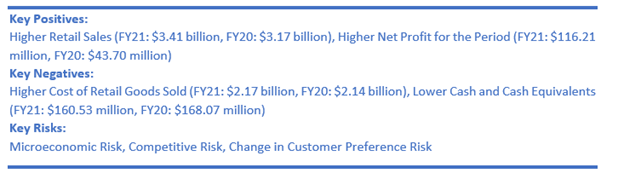

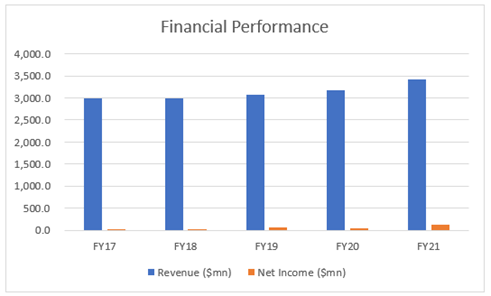

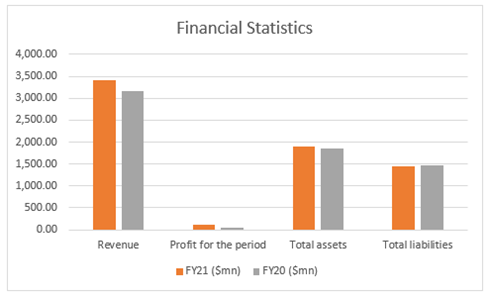

Looking at the past performance over FY17 to FY21, topline and bottomline of the company grew with a compounded annual growth rate (CAGR) of 3.46% and 54.98%, respectively. Total Revenue of the company improved from $3,172.8 million in FY20 to $3,414.6 million in FY21. Net Income of the company improved from $44.5 million in FY20 to $117.7 million in FY21.

Exhibit 1: Financial Performance

Source: Company Reports, Analysis by Kalkine Group

Result Performance (FY21 Ended 1 August 2021)

Exhibit 2: Financial Statistics

Source: Company Reports, Analysis by Kalkine Group

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 75.49% of the total shareholding. Tindall (Stephen Robert) and Tindall Foundation are holding maximum stake in the company at 28.32% and 21.31%, respectively, as provided in the table below:

Exhibit 3: Top 10 Shareholders

Source: Analysis by Kalkine Group

A Quick Look at Key Metrics: The company’s gross margin, EBITDA margin and net margin for FY21 stood at 36.4%, 12.7% and 3.4%, better than the FY20 result of 32.6%, 7.9% and 1.4%, respectively implying decent fundamentals.

ROE for FY21 stood at 28.4%, better than the FY20 result of 10.4%, implying that the company generated better return for its shareholders. Current ratio for FY21 stood at 1.13x, better than the FY20 result of 1.03x, implying that the company possesses better capabilities to meet its short-term obligations than the previous year.

Its Debt-to-Equity ratio for FY21 stood at 1.97x, lower than the FY20 result of 2.48x, depicting reasonable leverage position of the company.

Exhibit 4: Key Metrics

Source: Analysis by Kalkine Group

Recent Update:

Outlook:

During the financial year 2021, the company gathered confidence over its customer-led strategy. It is seeing the benefits of its transformation programme. Its investment in digital systems is expected to improve legacy systems and enable it to provide better experience to its customers. In FY21, the company introduced a new mobile-first Group eCommerce platform with The Warehouse the first brand to be migrated, and with other brands following in FY22.

The company agreed the $70 Mn Sustainability-Linked Loan with Westpac in the month of October that further extended The Warehouse Group’s commitment towards the environment.

Risks:

The company’s expose it to various financial risks including, liquidity risk, credit risk and market risk. Its overall risk management programme focuses on the uncertainty of financial markets and seeks to minimise potential adverse effects on its financial performance. Also, the company is exposed to the risks related to the COVID-19 as well as related lockdowns.

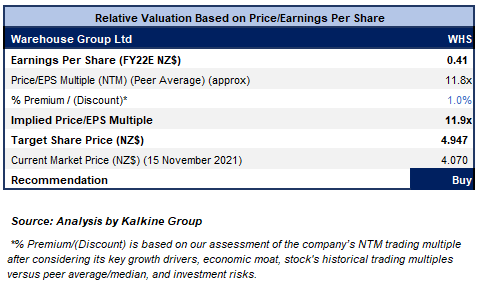

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

_(1).png)

Chart:

Source: REFINITIV

Note: Purple Color Line Reflects RSI (14-Period)

Stock Performance:

The company has recently launched the new MarketClub and MarketClub+ loyalty programmes, which will provide its customers a more convenient and multiple ways to save money. Moreover, it is in a strong stock position across all brands and the company is well placed and ready to meet peak period Christmas and summer demand.

The stock has been valued using P/E multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to Price/EPS Multiple (NTM) (Peer Average) considering decent outlook as well as higher net profit in FY 2021 on the YoY basis.

Considering the aforesaid facts, we give “Buy” recommendation on the stock at the current market price of NZ$4.070 per share (New Zealand Time: 4:43 PM (GMT +12)) on 15th November 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

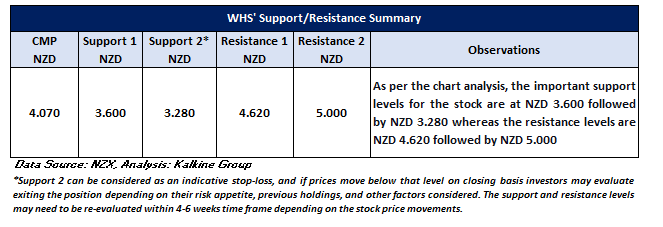

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...