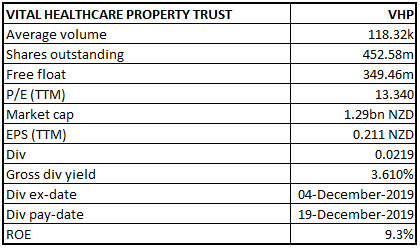

VHP Details

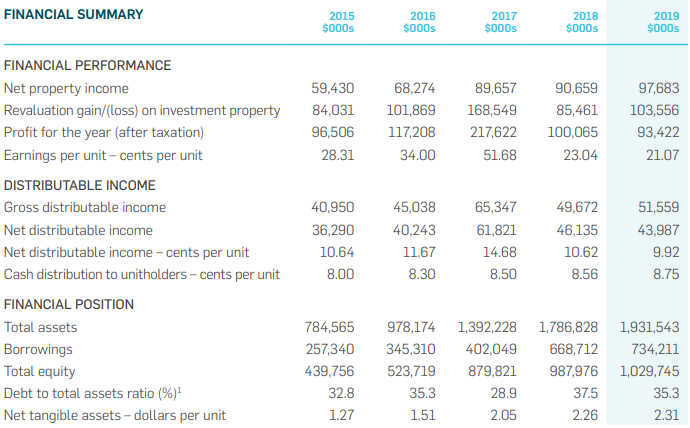

Top-line grew at CAGR of 13.26% for FY15-19: Vital Healthcare Property Trust (NZX: VHP) invests in high-quality healthcare related properties in New Zealand and Australia. It also provides a wide range of medical and health services. The principal objectives of the company involve acquiring, designing, building, managing and enhancing properties associated with the provision of healthcare services; building the Trust’s capital base and increase property values through rental growth and sound asset management. Looking at the past performance over FY15 to FY19, total revenue of the company has grown at a CAGR (compounded annual growth rate) of 13.26%. Group’s total revenue improved from $67.7 Mn in FY15 to $111.4 Mn in FY19. The cash position of the company improved from $1 Mn in FY15 to $6.1 Mn in FY19.

Company’s focus during FY19 has been on improving the operating performance of the business and progressing projects. The company partenered with NorthWest Healthcare Properties REIT to acquire a substantial portfolio of healthcare property assets in Australia. The portfolio added during the FY19 was worth $25.2 Mn, which were purchased to facilitate future projects adjacent to Vital owned facilities.

Looking at the healthcare demand, the company has also made strategic investments in land acquisitions adjacent to existing facilities to support and enhance long term value. Cash distribution for FY20 has been estimated at around 8.75 cpu, underpinned by ageing and growing population needing quality healthcare infrastructure.

Historical Financial Performance for FY15-19 (Source: Company Reports)

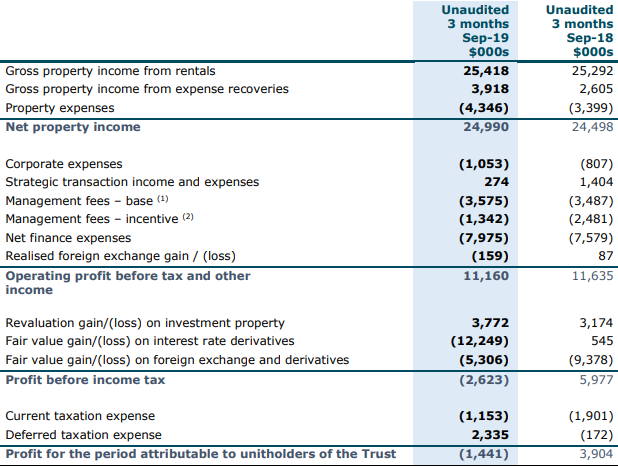

September’19 Quarter Key Highlights: VHP’s net property income as core portfolio grew by 2.6% over the prior year on the same currency basis. Occupancy in the portfolio increased by 99.9% as compared to 99.4% in the previous quarter, highlighting the lease-up of 1,000 sqm of space at the Gold Coast Surgery Centre. The portfolio’s weighted average lease expiry (WALE) decreased to 17.9 years, as compared to 18.1 years as on June 30, 2019.

September’19 Quarter Income Statement (Source: Company Reports)

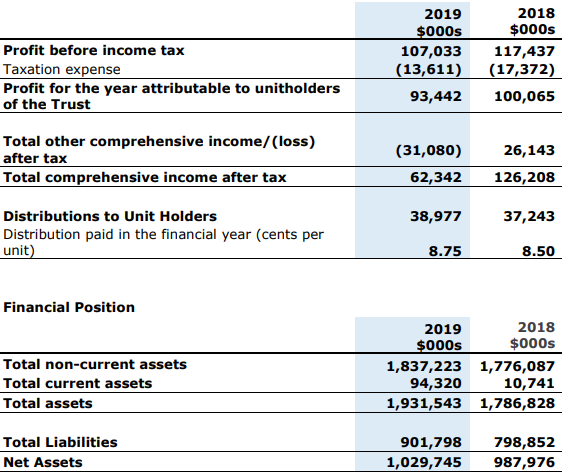

FY19 Key Highlights for the period ended June 30, 2019: Gross rental income for the period was reported at $101.1m, an increase of 7.9% on previous year. This was mainly due to the strong same property rental growth and expense containment. Normalized Net Distributable Income for the period was reported at $51.0m, a 3.8% increase on previous year. This can be attributed to the increase in Distributions by 2.2% to 8.75cpu, with an AFFO payout ratio of 76% and Normalized Net Distributable Income payout ratio of 76%. Portfolio value for the period increased to $1.8bn with 18.1 years of the weighted average lease term and at occupancy of 99.4%. The company-initiated projects of worth $218m at a weighted average return on cost of around 6.1%. Achieved revaluation gains increased by 6.0% to $103.6m, as compared to the previous year.

Cash and cash equivalents at the end of the period were reported at $6.07 m, as compared to $5.39 m at the end of the previous year. Trade and other receivables for the period were reported at $1.30 m, as compared to $1.19 m in the previous period.

FY19 Income Statement (Source: Company Reports)

Recent Update:

On December 19, 2019, the company announced 658,560 shares under Vital Healthcare Property Trust Ordinary Units “NZCHPE0001S4” at issue price of $2.6366 per unit cash pursuant to the Distribution reinvestment plan. These issues represent 0.15% of the total number of units on issue immediately prior to the issue of the new units.

On December 17, 2019, the company provided a status update on its value-adding initiative (potential restructuring initiative). The initiative is expected to consists of a foreign exempt listing on the Australian Securities Exchange, with the primary listing to remain on the NZX; an expected increase in distributions and payout ratio for all unitholders; and related legal and capital structure changes to enable the proposal and remove structural tax inefficiencies. This initiative is expected to provide the company with access to larger pool of capital, helping it to improve its competitive position for future growth opportunities along with ensuring it as an internationally competitive investment vehicle. Under this initiative, the company’s New Zealand properties and Australian properties are expected to get separated where “Vital Australia” which would be an Australian managed investment scheme and “Vital NZ” which would remain a New Zealand managed investment scheme and PIE. These trusts would together form a stapled group, which would remain listed on the NZX main board and add a foreign exempt listing on the ASX.

Managers associated with these transactions do not expect incurrence of material tax costs (including capital gains tax or stamp duty), plus they won’t be paid any additional fees for services provided in connection with the initiative. Unitholders’ approval (at least 75%) will be required by the first quarter of the calendar 2020 to support the initiative.

On November 20, 2019, the company announced the appointment of Dr Michael Stanford as an Independent Director. Mr. Stanford has around 30 years of experience as a Senior Executive in the Australian private and public health care sectors.

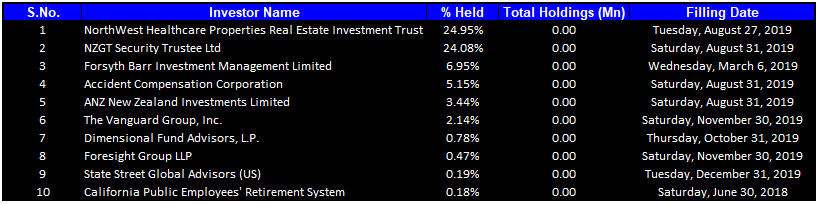

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 68.32% of the total shareholding. NorthWest Healthcare Properties Real Estate Investment Trust and NZGT Security Trustee Ltd hold maximum interests in the company at 24.95% and 24.08%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

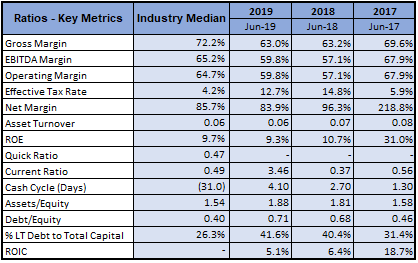

A Quick Look at Key Metrics: Its gross margin for FY19 stood at 63.0%, flat against FY18 result of 63.2%. Its EBITDA margin for FY19 stood at 59.8%, better than the FY18 result of 57.1%. Its net margin for FY19 stood at 83.9%, flat as the industry median of 85.7%. Current ratio for FY19 stood at 3.46x, better than the industry median of 0.49x, implying the company’s decent liquidity position. Its Return on Invested capital for the period was reported at 5.1%.

Key Metrics (Source: Thomson Reuters)

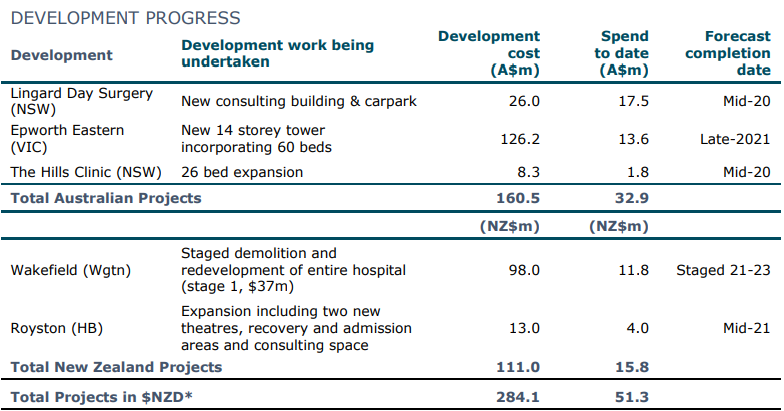

What to expect: As per the release, the company has $284m worth of “return on cost” for recently started projects, with 5 projects making up the pipeline with two representing the majority of this spend. One of these is in Melbourne at company’s Epworth Eastern campus and another as the Wakefield Hospital, Wellington’s pre-eminent private hospital. In the starting of year 2019, the company presented a formal tender process involving three qualified parties along with the appointment of Hawkins Construction as the lead contractor on the first stage of the project.

The project cost for the first stage was estimated to be $37m and the construction began in July 2019. Currently, the site is undergoing excavation work but following testing of the prototype base isolators for earthquake strengthening manufacturing has commenced. The first stage is expected to get completed by early 2021. Additionally, at Epworth Eastern campus in Melbourne, the company has started one of the largest projects in the company’s history as the next phase, i.e., an A$126m 14 level East Wing tower project.

Another project comprises Epworth Healthcare, Victoria’s largest not-for-profit hospital operator. It has pre-let 80% of the net lettable area, with the remaining 20% having strong expressions of interest for more space especially from doctors for consulting space. The project on completion is expected to enhance the value for the Epworth Eastern campus at around A$350m.

All these projects are being fully funded by debt at around 3% and delivering a return of 6.1%, enhancing profits in the next few years.

Ongoing Projects Details (Source: Company Reports)

Healthcare Outlook: With the ageing population in the region, rise in disposable income following improvement in an employment situation, currency depreciation – all these factors should contribute in rise in healthcare property. Further, rise in geo-political tension in the middle east and other countries suffering from aggressive agitations, healthcare demand is likely to rise further. The company with vast infrastructure and great brand recall, is well-positioned to capitalize on emerging opportunities in the healthcare sector.

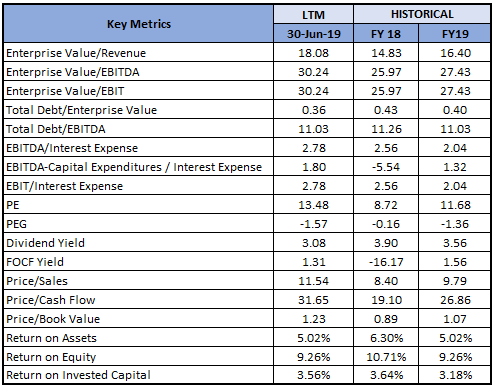

Key Valuation Metrics (Source: Thomson Reuters)

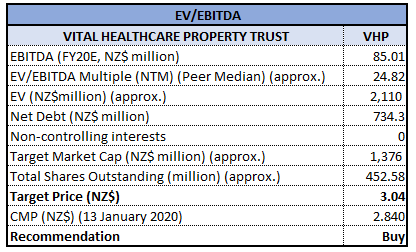

Valuation Methodology: EV/EBITDA Multiple Based Approach

EV/EBITDA Multiple Based Valuation (Source: Thomson Reuters)

Technical Overview:

Monthly Candlestick Chart:

(Source: Thomson Reuters)

Weekly Candlestick Chart:

(Source: Thomson Reuters)

The stock is trading above all key exponential moving averages including 20 EMA, 50 EMA and 200 EMA, suggesting a continuation of bullish trend. Few weeks back, the stock formed a bullish engulfing pattern at 20 EMA, which is reflected on the inherent strength of the stock. We have resorted to Fibonacci Projections to arrive at the likely target price for the stock. Ideally, it is 50% projection numbers (i.e. $3.0293) which has mostly held in the past that we have taken as likely price target for the stock.

Stock Recommendation: The stock of VHP posted a YTD return of 4.7970%, while in the span of one year it posted a return of 37.86%. Company’s financial position and stable portfolio delivered a solid core operating result for FY19. During the full year period, it witnessed an increase in valuation of its existing properties to $1.8 billion, and it aims to further grow its portfolio through the recently announced projects at Epworth Eastern in Melbourne and Wakefield Hospital in Wellington. Considering the company’s business model, FY19 top-line growth, September quarter performance, profitability margins, healthcare outlook, and current trading levels, we have valued the stock using a relative valuation method i.e., EV/EBITDA multiple, and arrived at a target price of high single-digit growth (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of NZ$2.840 up 1.07% on January 13, 2020.

VHP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...