Company Overview: New Zealand-based company, Vector Limited (NZX: VCT) owns and manages a portfolio of energy and communication. It delivers energy and communication services to more than 1 million residential and commercial customers across Australasia and the Pacific. Through Vector Communications, the company monitors and maintains its fibre network for businesses that demand faster, reliable, and secured data networks. Besides this, the company is one of the largest New Zealand companies on the NZX exchange.

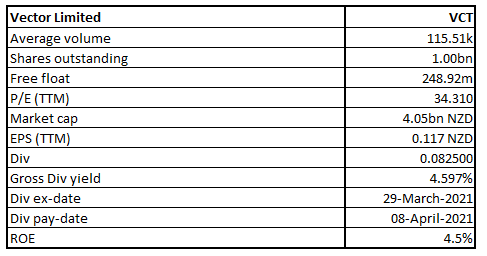

VCT Details

Vector Limited (NZX: VCT) is an innovative New Zealand energy company that runs a collection of businesses offering energy and communication services to over one million homes and commercial customers across Australasia, and the Pacific.

Looking at the past performance, VCT’s top-line over FY16-20 increased with a compounded annual growth rate (CAGR) of ~3.1%. Its total revenue for FY20 was reported at $1,294.0 million, as against $1,144.6 million in FY16.

Results Performance (Half-Year Ended 31 December 2020)

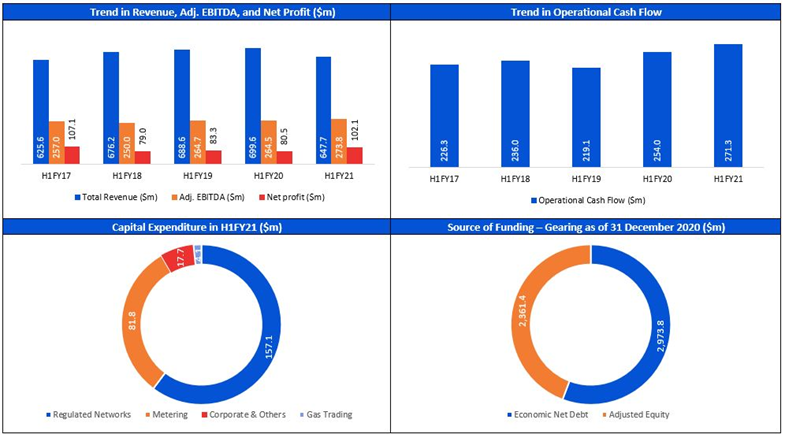

The company reported solid results for the first half ended 31 December 2020, with adjusted EBITDA of $273.8 million, an increase of 3.5%YOY. The company was able to achieve this despite the uncertainties caused by COVID-19. Further, net profit after tax was $102.1 million, a jump of 26.8% YOY.

The energy segment reported an EBITDA of $195.9 million, up 3.5% YOY, primarily benefited from the retention of loss rental rebates (LRRs). As indicated in FY20, LRRs were retained to support limit Auckland electricity customers' price increases and compensate for volume reductions because of COVID-19.

Further, in the Gas trading, after adjusting for the sale of the Kapuni gas processing plant and related assets, adjusted EBITDA decreased 1.4% to $14.6 million mainly led by lower natural gas volumes and margins that were partially offset by better performance from the Ongas LPG business.

The metering segment reported an adjusted EBITDA of $83.1 million, an increase of 9.2% YOY, driven by the continued rollout of advanced meters, particularly in Australia.

The Board declared an interim dividend of 8.25 cents per share at an imputation rate of 10.5%.

Exhibit 1: Key Metrics

Source: Company Reports, Analysis by Kalkine Group

Operational Performance (For Nine Months ended 31 March 2021)

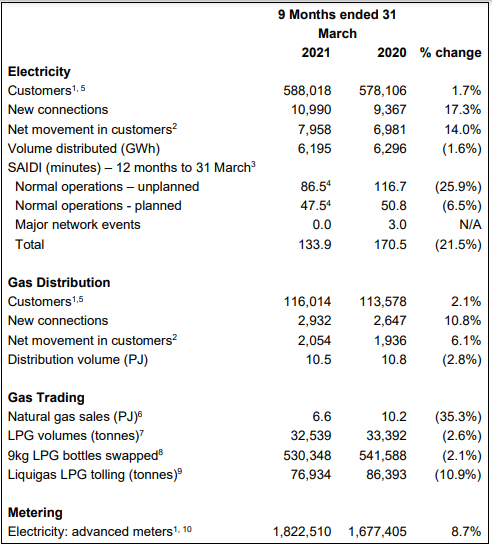

For the nine months ended 31 March 2021, the company has realized strong growth in Auckland, resulting in strong network connection numbers throughout its electricity and gas networks. Total electricity connection numbers increased by 1.7% YOY, however, electricity volume decreased 1.6% YOY, led by decreased activity from the industrial and commercial sectors due to COVID-19. Meanwhile, Gas distribution network customers grew 2.1% YOY in total connections, while volume decreased 2.8% YOY.

Further, the metering business continued its winning streak in New Zealand as well as in Australia, where advanced meter numbers grew by 8.7% YOY, with a total fleet of 1,822,510. The company has installed over 360,000 advanced meters in Australia. BottleSwap decreased 2.1% YOY in the number of 9kg bottles swapped, mainly due to a significant rise in demand at the start of the COVID-19 alert level 4 lockdown in late March 2020. In addition, Natural gas LPG volumes and Liquigas LPG tolling fell due to a 35.3% fall in natural gas volumes led mainly by the loss of a large customer in January 2020.

On 31 March 2020, the company finalized the sale of its interests in the Kapuni Gas Treatment Plant (KGTP) and co-generation facility. Therefore, it has changed the methodology of calculating LPG volumes to report continuing activities only. LPG volumes include LPG sold by the OnGas business only.

Exhibit 2: Key Operational Statistics

Key Data (Source: Company Reports)

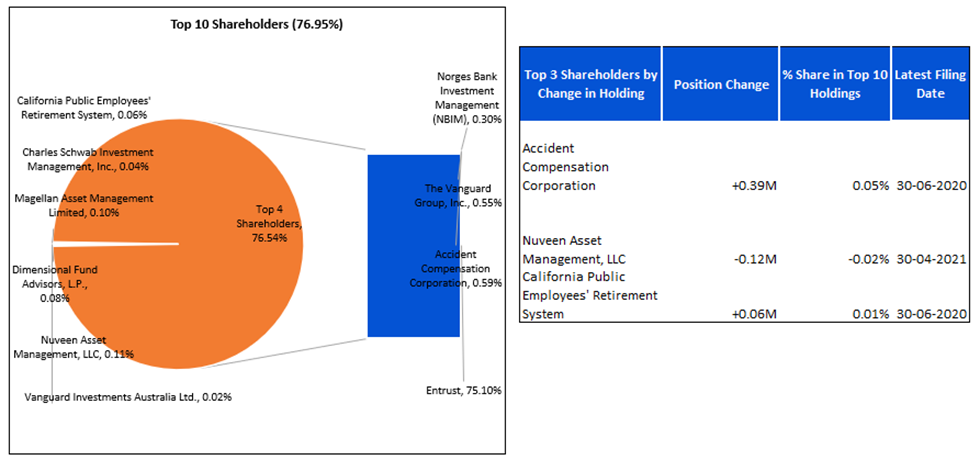

Top 10 Shareholders: The top 10 shareholders have been highlighted in the pie-chart, which together forms around 76.95% of the total shareholding. Entrust and Accident Compensation Corporation are holding a maximum stake in the company at 75.10% and 0.59%, respectively, as provided in the table below:

Exhibit 3: Top 10 Shareholders

Source: Analysis by Kalkine Group

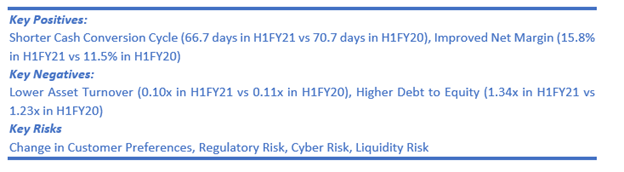

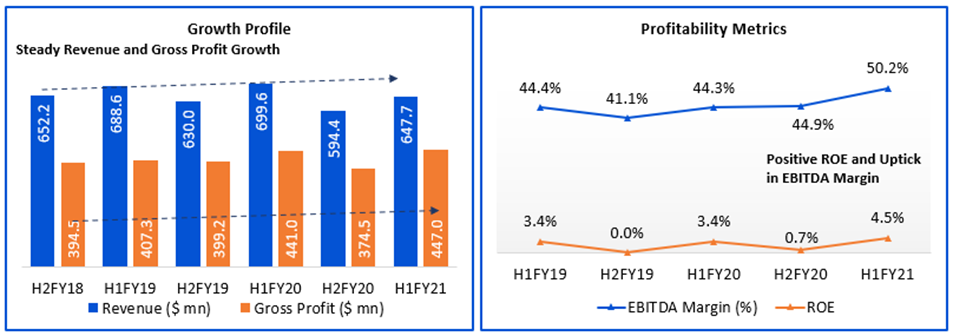

A Quick Look at Key Metrics: The company’s gross margin and EBITDA margin for H1FY21 stood at 69.0% and 50.2%, respectively, implying greater efficiency in managing input and operating costs by the company. Its ROE for H1FY21 stood at 4.5%, higher than the H1FY20 result of 3.4%, implying a strong strategy of the company in generating a decent return on the investment it received from its shareholders. The period witnessed a stable current ratio of 0.38x.

Exhibit 4: Key Metrics

Source: Analysis by Kalkine Group

Outlook:

As per the operational performance 9MFY21, the company has partially recovered from its Covid-19 impact and reported strong growth in network connection numbers across electricity and gas networks. In addition, the metering business continues to perform despite high competition in the market. Besides, the company continues to invest in infrastructure to grow its network integrity, the rising deployment of advanced meters, the start of 4G modem upgrades, growing stock levels to counter risk associated with global production shortage.

Henceforth, the rise in industrial and commercial activities is expected to drive the demand for electricity, gas, and advanced meter which would bring the company on track with the growth momentum. Based on H1FY21 results, the company forecasted FY21 adjusted EBITDA to be increased in the ambit of $500-520 million, up from previous guidance of $480-$500 million, provided there is no further negative impact of COVID-19 on economic activity, such as extended or frequent lockdowns.

Risks:

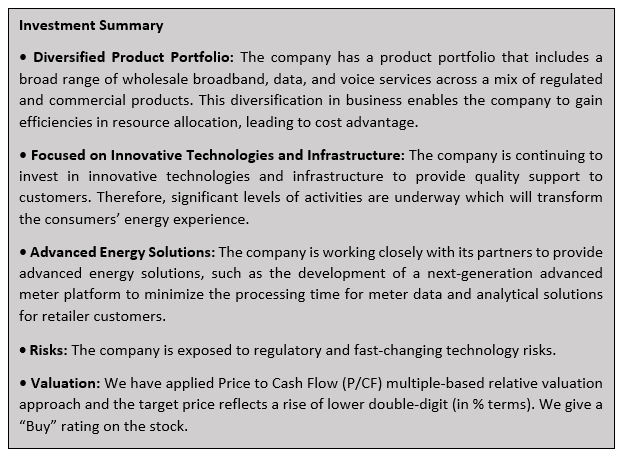

The business of the company is impacted if the company experiences a significant change in customer needs and expectations. Further, the company must appropriately innovate to keep pace with technological advancements as they emerge. The company is also exposed to external factors, resourcing, and technical constraints, and Auckland’s ongoing growth.

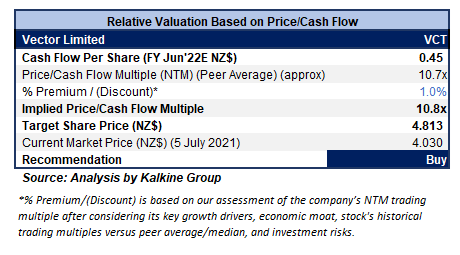

Valuation Methodology: Price/CF Based Relative Valuation (Illustrative)

Stock Recommendation:

The stock price of the company declined by ~3.80% in 9 months. It has made a 52-week low and high of $3.5900 and $4.6500.

We have valued the stock using a Price/CF multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We have assigned a slight premium to Price/CF Multiple (NTM) (Peer Average) considering a diversified portfolio of businesses and better liquidity position which could help the company during tough business conditions.

Considering current trading levels and aforesaid investment catalysts, we give a “Buy” recommendation on the stock at the current market price of NZ$4.03 per share (New Zealand Time: 11:18 AM(GMT+12)) on 5th July 2021.

.png)

Source: REFINITIV

Note 1: The reference data in this report has been partly sourced from REFINITIV.

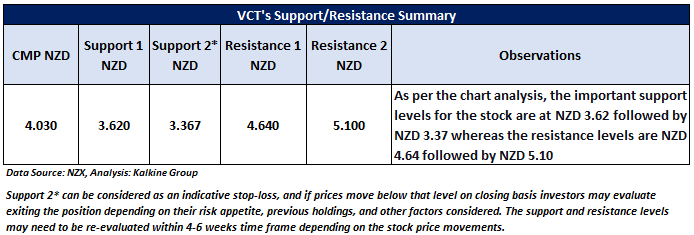

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...