Company Overview: Electricity generator and energy retailer, Trustpower Limited (NZX: TPW) supplies gas and telecommunications services to its New Zealand customers as part of its multi-product retail business. Its customer base figures are impressive with around 266,000 electricity customer connections, around 40,000 gas customer connections, and around 100,000 telecommunications customer connections. It offers businesses a range of landline voice services along with a range of Internet plans with options, including Ultra-Fast Broadband and broadband. Its generation activities are undertaken in both Australia and New Zealand, while its retail operations are undertaken in New Zealand.

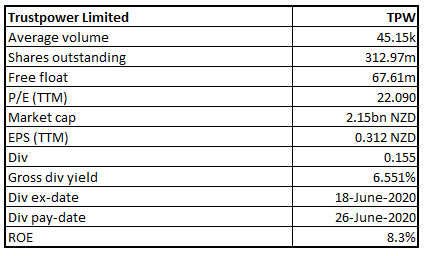

TPW Details

Investment Summary:

Electricity Demand Rising with Reopening of Industries: Trustpower Limited (NZX: TPW) is primarily engaged in the ownership and operation of electricity generation from renewable energy sources and the retail sale of energy and telecommunications products to its customers. It has a market capitalization of ~$2.15 billion as on August 24, 2020.

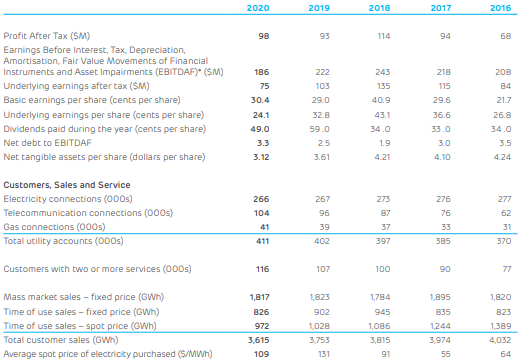

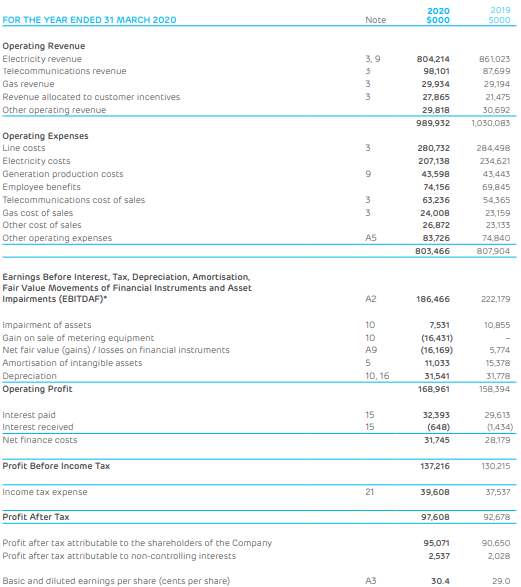

Looking at the past performance over FY16 to FY20, the top line and bottom line of the company grew at a compounded annual growth rate (CAGR) of 2.28% and 9.56%, respectively. The total revenue improved from $904.7 million in FY16 to $989.9 million in FY20 and its bottom line improved from $67.8 million in FY16 to $98 million in FY20.

In FY20, the company continued to build capability and strength in the business on the back of high-quality customer base, growing bundled retail business, and strategy to grow and enhance its portfolio of small-scale, localised, and renewable generation schemes. The financial year 2020 also witnessed the launch of wireless broadband (WBB); development of mobile capability; significant overhauls and upgrades to TPW’s generation schemes; and continued gains in digitisation and automation which have improved the customer experience and reduced both operating, and cost to serve.

Historical Performance (Source: Company Reports)

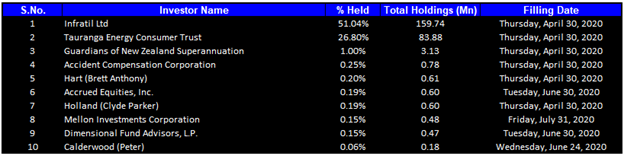

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 80.03% of the total shareholding. Infratil Ltd and Tauranga Energy Consumer Trust are holding maximum stake in the company at 51.04% and 26.80%, respectively, as provided in the table below:

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

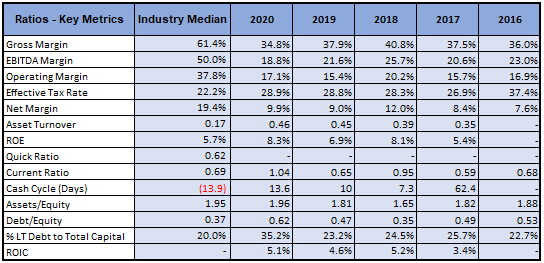

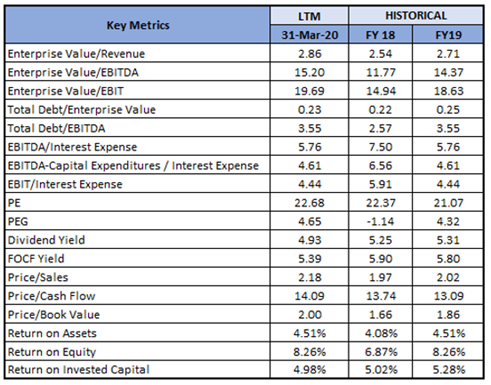

A Quick Look at Key Metrics: The company’s net margin stood at 9.9% in FY20, which is higher as compared to the figure of FY19 of 9.0%. This suggests that the company can manage its operating and non-operating costs more efficiently. RoE of TPW stood at 8.3% in FY20 which is higher than the industry median of 5.7%, suggesting TPW is more capable of generating a higher returns for its shareholders.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Subdued Q1FY21 Performance: The company, in its Q1FY21 report, highlighted that Trustpower retail market activity was materially reduced during level 4 lockdown, underpinned by a decrease in total utility accounts across the quarter, down ~2,000. Due to increased working from home and colder weather, mass market customer electricity demand grew up; however, due to a slower return to normal, and the loss of some ICP’s, C&I demand reduced materially than the pcp. There was an increase in total data usage which grew by 81% compared to the pcp, over increased working-from-home activities and increased telco customers.

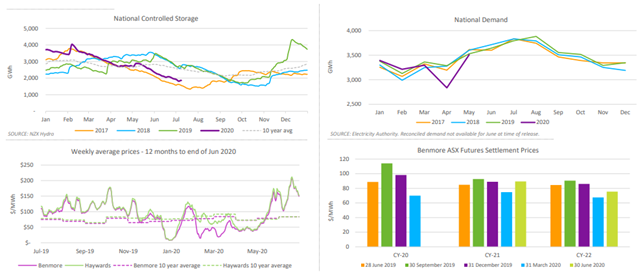

Wholesale Electricity Market Data (Source: Company Reports)

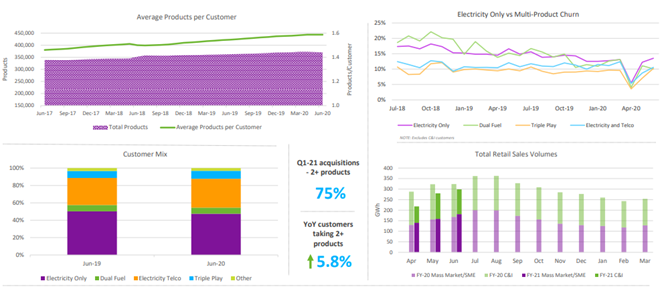

Retail Data (Source: Company Reports)

Marginal Improvement in FY20 NPAT: The net profit after tax (NPAT) of $97.6 million for FY20 (ended March 31, 2020) was up by 5% on the previous corresponding period. However, this year includes a one-off gain of $16.4 million resulting from the sale of legacy meter business. Underlying profit after tax was $75.5 million or 26% below last year. Earnings Before Interest, Tax, Depreciation, Amortisation and Fair value movements in financial Instruments (EBITDAF) was $186.4 million or 16% below last year’s EBITDAF of $222.2 million. The diminished performance was across both the retail and generation sectors. The result was affected by many factors like a decrease in rainfall which caused lower generation production, material plant outages, accounting changes, costs of developing capability and restraint in pricing changes. Some of these changes are one-off or cyclical in nature which is beyond the control of the company.

The Board of Directors declared a final dividend of 15.5 cents per share, fully imputed, delivering a total ordinary dividend to shareholders of 32.5 cents per share for FY20.

FY20 Income Statement (Source: Company Reports)

A Look at Recent Update: The company recently announced that RIO TINTO would wind-down operations at New Zealand Aluminium Smelters Limited (NZAS) in August 2021. The company believes that with its geographically dispersed generation schemes and customer bases, it is well placed to mitigate any negative impact arising out of NZAS exit. It further highlighted that it has sufficient capacity to store water for extended periods until demand increases.

What to Expect: As per the release, EBITDAF for FY21 is expected to be between $190 million - $215 million, with assumptions that generation volumes for FY21 to be around 1,862 GWh; wholesale prices are in line with current forward pricing; average residential electricity consumption and average temperatures for the year; total average mass-market customers of ~230,000; no change in overall customer pricing and bad debt levels are elevated in line with the expected economic downturn.

Utility Sector Outlook: The power sector is united to decarbonise transport and accelerate the electrification of South Island industry away from a reliance on coal. The sector is likely to adapt itself to the closure of the smelter and rebalance in the electricity system through investment in new transmission and expected growth in new electricity demand.

Key Risks: The company is exposed to interest rate risk, liquidity risk, and credit risk. Prudent liquidity risk management requires maintenance of sufficient cash, marketable securities, or unutilised committed credit facilities in order to provide cover for reasonably conceivable adverse conditions.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

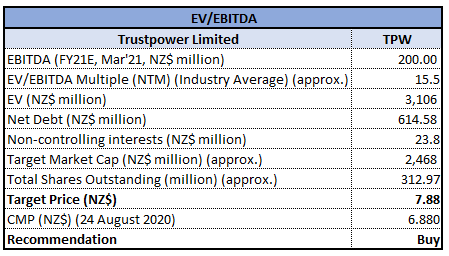

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

In a low volatile market, the stock on the first trading day of the on-going week has given close at $6.88 around the previous week’s stronger close level. The closing for the stock is also above 20 periods SMA implying strength in uptrend. Technical indicator RSI with around 50 reading suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around $7.80 while support could be around 50% retracement level of $6.60.

Stock Recommendation: The company believes that through investment in new transmission and expected growth in new electricity demand, the sector would be able to cope up and adapt to the tough situation arising out of NZAS exit. TPW is well-positioned to grow and prosper in a changing and evolving environment, underpinned by high-quality customer base and dispersed generation schemes. Furthermore, the long-term electrification of the economy will continue to drive demand. Besides, the growing demand for data usage will ensure its telecom business continues to deliver good business performance for the company.

Considering the aforesaid facts, recent update and FY20 results, we have valued the stock using EV/EBITDA multiple based relative valuation method (on an illustrative basis) and have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$6.880 per share, down by 0.15% on August 24, 2020.

.png)

TPW Daily Technical Chart (Source: Refinitiv (Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...