Company Overview: New Zealand based company, Tower Limited (NZX: TWR) is involved in the provision of general insurance in two important geographical regions i.e. New Zealand and the Pacific Region. The company offers wide range of insurance services such as car insurance, house insurance, travel insurance, content insurance, business insurance, and others. Over the span of past 3 years, Tower has undergone a divestment programme which saw the company divesting its Medical Insurance Limited business, Managed Funds Limited business as well as TOWER Life (N.Z.) Limited business to concentrate its focus as the pure NZ general insurer.

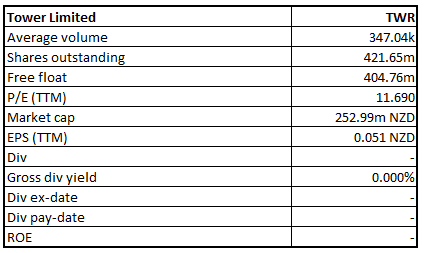

TWR Details

Investment Summary:

Looking at the historical performance from FY2015-19, the topline of the company grew at a compounded annual growth rate (CAGR) of 3.37%. Its total revenue improved from $265.7 million in FY15 to $303.4 million in FY19. Its net income improved from a loss of $7.0 million in FY15 to $16.6 million in FY19.

The company demonstrated solid growth and stabilised claims ratio in the first half of FY20 on the back of the implementation of the strategic initiatives such as growth through digital channels, challenging outdated industry norms. Besides, introduction of new technologies help in simplifying and automating many functions enabling productivity gains. In the month of March, almost 60% of its new business came in through digital channels.

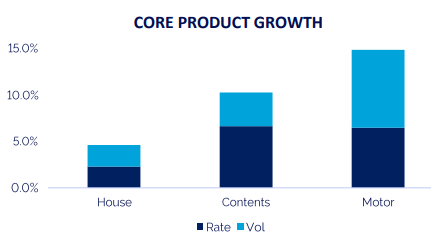

Core NZ portfolio grew at 11.9%, with 8.3% attributable to organic growth and 3.6% to Youi NZ. The underwriting and pricing improvements continue to deliver positive outcomes, excluding Timaru Hailstorm. Claims expense ratio was reported at (excluding large events) 44.6%, which is a normalized claims ratio after a year of year benign weather. Reinsurance ratio reduced to 14.9% in first half, mainly due to improved underwriting, risk-based pricing approach, EQC changes, growth in motor and addition of Youi NZ portfolio. GWP’s growth across core NZ products comprised 4.6% growth in NZ house, 9.6% growth in NZ contents and 14.7% growth in NZ motor.

The period also witnessed continuation of migration of customers onto new platform as their policy renews. The company’s tailored, transparent and customer-focused approach delivered strong retention, in line with previous experience. Over 7,000 Youi NZ customers successfully migrated to new platform as on May 1, 2020, with strong retention of over 88% achieved. Migration of the Youi NZ portfolio is expected to be completed in February 2021.

TWR’s Core Product Growth (Source: Company Reports)

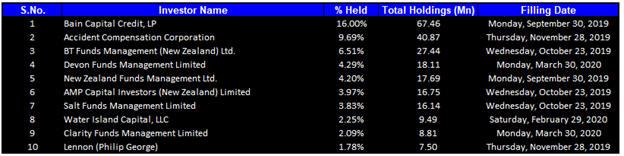

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 54.61% of the total shareholding. Bain Capital Credit, LP and Accident Compensation Corporation are holding maximum interests in the company at 16.00% and 9.69%, respectively.

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

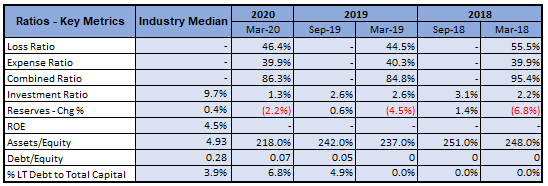

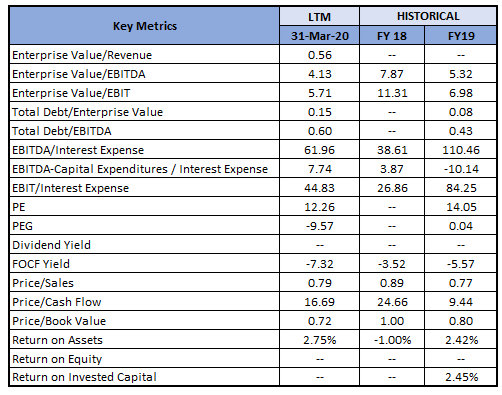

A Quick Look at Key Metrics: TWR's debt to equity ratio for H1FY20 stood at 0.07x, lower than the industry median of 0.28x, depicting reasonable leverage position of the company.

Key Metrics (Source: Refinitiv (Thomson Reuters))

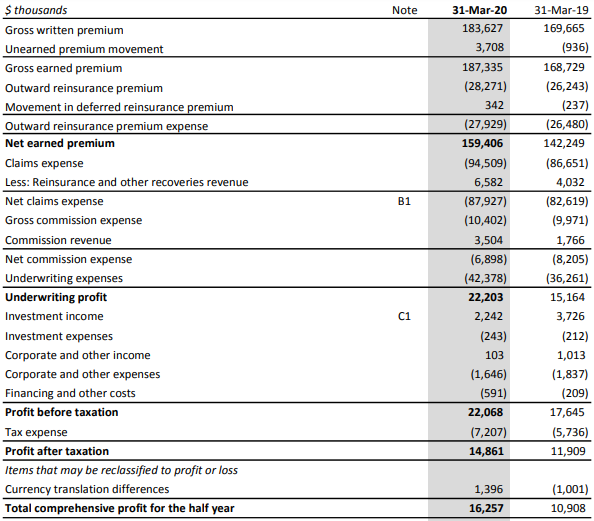

Youi NZ Portfolio Drives First Half Performance: The company reported after tax profit of $14.9 million, a $3 million improvement on previous corresponding period (pcp). Underlying profit after tax stood at $16.9 million, $2.5 million lower than prior year, driven by Timaru Hailstorm. Net earned premium was higher due to growth in core book and new pricing approach.

There was an increase in expenses due to requirement to run multiple systems during transition year. Management expenses include $0.65 million of amortization cost related to the Youi NZ portfolio acquisition in December 2019. Claims ratio, excluding large events, stabilised at 44.6%. Investment income impacted in March due to debt market volatility but has partially unwound in April.

As on March 31, 2020, TIL had a $95.3 million of solvency margin, which was equivalent to 280% of minimum solvency capital. The first half profit has contributed an additional $13.3 million of solvency, offsetting the purchase price of the Youi NZ portfolio.

At the end of first half period, Tower held $45.3 million above RBNZ minimum requirements. The agreement with RBNZ to remove EQC recoveries outstanding from TWR’s solvency calculation reduced solvency capital by $53.0 million, which was offset by the recent capital raise.

H1FY20 Income Statement (Source: Company Reports)

Tower Refunds $7.2 Mn to Customers: The company recently highlighted that, due to the lower cost of car claims during the COVID-19 lockdown period, it will be refunding customers’ $7.2 million. Every customer would be refunded part of the car insurance premiums (40% to 45%) they paid between 24 March and 13 May 2020. The refunds are expected to be paid from late June.

During the lockdown, the company’s response has been to continue helping customers with claims and supporting those experiencing financial hardships. During the lockdown, new businesses have reduced significantly but strong retention was maintained. The company proactively committed to not make a windfall gain as a result of reduced car claims during lockdown.

FY20 Guidance: As per the release, the company has updated its FY20 guidance of underlying NPAT to $25 million - $28 million, taking into account the Timaru Hailstorm, Tropical Cyclone Harold, subdued growth and lower expenses. It has also been given to understand that there would no financial impact from Tower’s refund of motor premiums as these would be offset by savings in claim costs.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

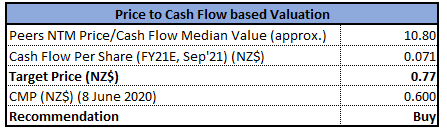

Valuation Methodology: Price to Cash Flow Based Relative Valuation (Illustrative)

Price to Cash Flow Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, yellow lines are retracement lines which measures price rebound and backtrack, and orange colour dotted line is Parabolic SAR suggesting reversal of position (i.e., from buy to sell or sell to buy).

Having experienced roller-coaster ride, the stock has formed Falling Wedge Pattern on the weekly chart with high probability of bullish break-out in the near-term. In today’s trading session of the current week, the stock gave opening at the previous week close of $0.5950 and closed at higher price of $6.0000. Technical indicators such as MACD with bearish cross-over but flattish curve at the end, and RSI reading of 41 with flattish curve at the end, suggest neutral momentum for the stock.

Going forward, if bullish break-out is taking place then there is high probability that the stock could re-visit its recent high of $0.75 where it could have major resistance while support could be at $0.58 around 23.6% retracement level which is also converging point of trend line and retracement line.

Stock Recommendation: The company’s move of not having a windfall gain and refund customers is appreciable and sets a trend which is expected to be followed by other players in the market as well. Half-yearly result has demonstrated that the company is well placed to respond to the changing economic environment. Considering the anticipation of extended economic slowdown, low growth environment and also RBNZ’s advise to protect solvency position, the company has taken initiatives of reducing its cost base in the process. The Board has decided that no first half dividend will be paid, and any second-half dividend will be determined in line with the company’s full year results while considering economic condition at the time.

We have applied P/CF Based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

.png)

TWR Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...