Company Overview: The New Zealand Refining Company Limited is a supplier of refined petroleum products. The Company operates an oil refinery at Marsden Point near Whangarei as a toll refiner. The Company also owns and operates a pipeline, running from the refinery at Marsden Point to Wiri, located in South Auckland, transporting refined fuels for consumption within the Auckland market. Its segments are Oil Refining, Distribution and Other. The Oil Refining segment includes the oil refinery located at Marsden Point, which processes a range of crude oil types imported from around the world. Its distribution segment includes infrastructure to support the distribution of manufactured products to its customers. The Other segment includes subsidiary Company operations and properties. The Company, through its subsidiary, Independent Petroleum Laboratory Limited, provides specialized fuels, biofuels, and industrial and environmental laboratory testing services.

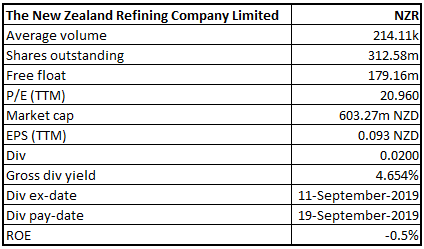

NZR Details

Strong Contribution from the Distribution Segment: The New Zealand Refining Company Limited (NZX: NZR) operates New Zealand’s only oil refinery at Marsden Point near Whangarei as a toll refiner, and owns and operates a pipeline, running from the refinery at Marsden Point to Wiri, located in South Auckland, transporting refined fuels for consumption within the Auckland market. As per the result for the first half ended 30 June 2019, the company witnessed excellent operational and safety performance during the period, with an increase in throughput and a favourable exchange rate supporting an uplift of 22% in processing fee. The result, however, was impacted by a number of unfavourable factors including, high electricity prices, lower than expected refining margins and few one-off costs. The Board declared a fully imputed interim dividend of 2 cents per share, with a record date and payment date on 12 September 2019 and 19 September 2019, respectively. The period was marked by significant improvement in health and safety at the refinery which continued till October 2019, as reflected in the operational update for September/October 2019. Also, the company reported a decent throughput in September/October, supported by good utilisation by customers and high refinery availability.

The company is focused on managing its cost base and expects to report a reduction in operating costs, excluding pass-through costs for natural gas, sulphur and carbon, in the second half of the year. In addition, development of a long-term asset management plan is also underway, which will support a reduction in capital spend.

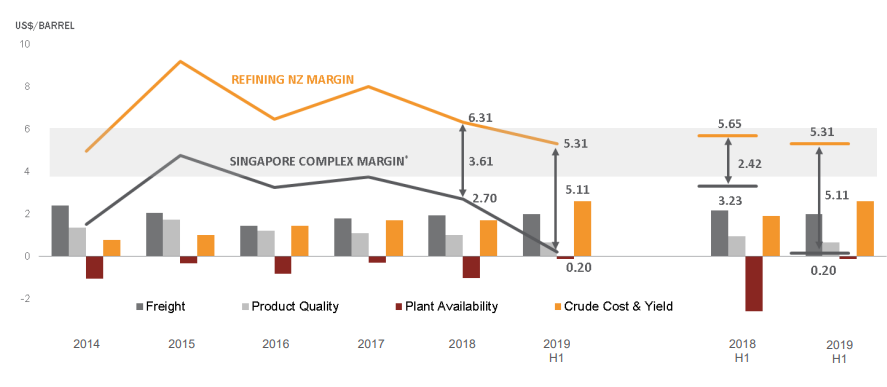

Over the period of FY14 – FY18, the company witnessed decent operating revenue CAGR of 11.7%, with FY14 and FY18 operating revenue amounting to $230.56 million and $359.32 million, respectively. During the first half, the company achieved an average uplift over the Singapore Complex Margin of USD 5.11 per barrel, as compared to USD 2.42 per barrel in the prior corresponding period, depicting higher plant availability and a balanced product make.

Uplift over Singapore Complex Margin (Source: Company Reports)

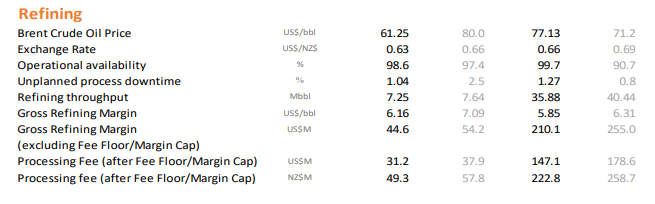

Operational Update for September/October 2019: Processing fees for September/October stood at $49.3 million, as compared to $56.2 million for July/August 2019. Year-to-date processing fee income stood at $222.8 million, as compared to $209.5 million in the prior corresponding period. Refinery throughput for the period came in at 7.25 million barrels, reflecting good utilisation by customers and high refinery availability. Throughput in July/August 2019 was the highest for 2019 at 7.42 million barrels. Gross refining margin for the period was USD 6.16 per barrel, representing lower than the normal uplift over the Singapore Dubai complex margin. Global refining margins were initially supported by the attack on the Saudi Arabian oil facilities and firm Asian demand, but later saw a negative impact due to fall in fuel oil cracks without the expected rise in diesel cracks. In the month of October, margins began to weaken as a result of the significant decline in high sulphur fuel oil prices ahead of the IMO MARPOL 2020 and rising crude freight rates. The Refinery to Auckland Pipeline reported a throughput of 3.4 million barrels with an income of $6.1 million, up 5% on the prior corresponding period. The pipeline reported high operational availability except for a planned short statutory inspection. The company maintained a good hold on the operating costs with the ongoing pressure from higher electricity prices. In addition, the company reported continued improvement in safety performance, with lost time injury frequency currently at 0.14 per 200,000 work hours and no Tier 1 or Tier 2 process safety events during the period.

Refining Operational Data (Source: Company Reports)

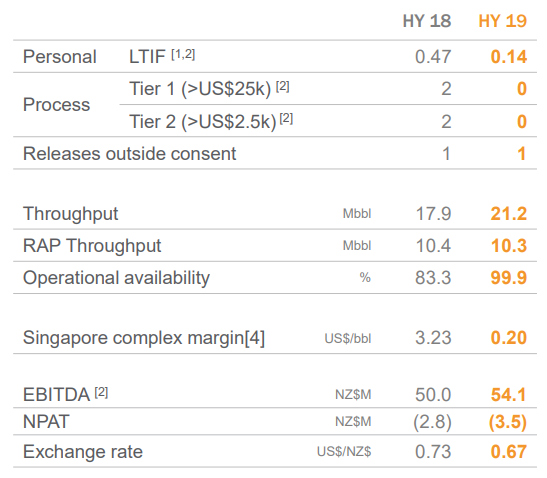

1HFY19 Highlights: During the half-year ended 30 June 2019, the company reported a gross refining margin of USD 5.31 per barrel, as compared to USD 5.65 per barrel in the prior corresponding period. The margin went down due to higher than forecast gasoline exports from China into the Asia Pacific region. EBITDA for the period came in at $54 million, up 8% on prior corresponding period EBITDA of $50 million. Free cash flow for the six months stood at $18.2 million, as compared to an outflow of $75 million in the prior corresponding period. The period was marked by excellent operational and safety performance backed by outstanding plant availability of 99.9%, as compared to 83.3% in the same period last year. Crude intake for the period came in at 21.2 million barrels, up on prior corresponding period’s intake of 17.9 million barrels.

H1FY19 Highlights (Source: Company Reports)

Refining Segment Performance: During the half, EBITDA for the refining segment stood at $32.6 million, and free cash flow amounted to $7.6 million. The company reported a strong cash flow despite cyclical historical results, supporting funding of significant capital projects and dividends. Core competitive advantages for the segment are identified by the refinery’s location and high reliability.

Distribution Segment Performance: Under the distribution segment, the company possesses a multi-product pipeline for supply in Auckland. During the half, EBITDA for the segment was reported at $20.0 million, and free cash flow came in at $9.8 million. The segment transports 52% of the refinery’s production, and 37% of New Zealand’s fuel demand. Over the last 5 years, the company has invested to meet significant volume growth in the business. Additionally, the company is under constant exploration for the use of Drag Reducing agent (DRA) on the RAP pipeline, that will increase capacity on this critical piece of infrastructure by up to 15%, and further contribute to the resilience of fuel supply into Auckland.

Laboratory Segment Performance: This segment provides specialist fuels, biofuels and other lab testing services to leading oil companies, governmental agencies, and international terminals. EBITDA for the laboratory segment stood at $1.5 million and free cash flow was reported at $0.8 million. The segment has reported strong growth in the last decade along with EBITDA and revenue CAGR of 6% since 2005.

During the second half, the company expects to report strong throughputs, along with capital spend in line with the budget and strict management of operating expenses. As per the operational update for September/October 2019, the company completed piping tie-ins as part of a project to install additional pumping capacity for the Refinery to Auckland Pipeline, which will further enhance the resilience of supply to Auckland.

Transpower Outage Update: The company recently updated that it was hit by the Northland power outage due to a fault on the Transpower national grid between Bream Bay to Kaitaia. As a result of the outage, the refinery suffered total loss of power and the plant was safely shutdown with no injuries and no identified damage to processing units. As per the most recent release on the matter, the company notified that it is working through the restart of the refinery’s processing units, which is expected to be completed in the next few days. Also, the company expects the impact of the outage to be around $1.5 million - $2.5 million. As per the update, Marsden Point fuel stocks stood at healthy levels, the Refinery to Auckland Pipeline is online and coastal shipping operations from refinery are back to normal.

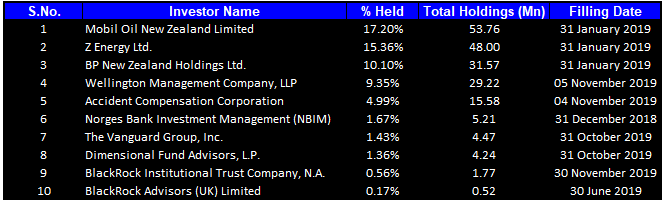

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 62.18% of the total shareholding. Maximum number of shares were held by Mobil Oil New Zealand Limited with a percentage holding of 17.20%, followed by Z Energy Ltd. with a holding of 15.36%.

Top Ten Shareholders (Source: Thomson Reuters)

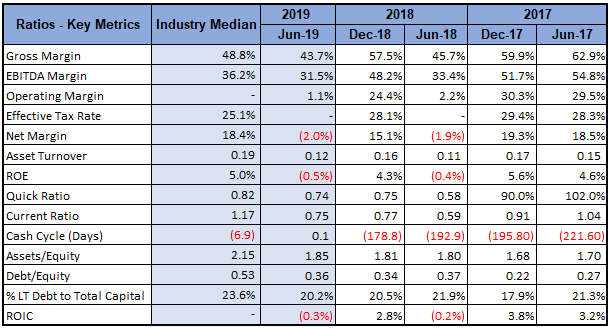

Key Metrics: During the first half, gross margin and EBITDA margin came in at 43.7% and 31.5%, respectively. Current ratio of the company stood at 0.75x, better than prior corresponding period’s current ratio of 0.59x. Debt-to-equity ratio stood at 0.36x, better than the industry median of 0.53x.

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company expects strong throughputs and has forecasted for a baseline operating expenditure of $180 million in 2020, excluding inflation. With strategic initiatives, operating expenditure is expected to be in the range of $182 million - $185 million. To limit the long term capital spend, the company has an asset management process in place. Average capital expenditure over the period covering 2023-2033 is expected to be ~$64 million. As a part of its strategic initiatives, the company has a sulphur project under construction, which is expected to commence in Q4 2019 and will support the formation of cleaner fuels. Final investment decision with respect to the Maranga Ra solar farm is also expected in the fourth quarter, which is expected to promote cost savings of $3 - $4 million per annum. Moreover, dredging optimisation is also underway with final investment decision expected in Q4 2019 or Q1 2020. As per Facts Global Energy, an independent consultancy firm, demand growth in Asia is expected to overtake refining capacity additions until at least 2029. The firm expects an improvement in Mogas margins in 2020. While jet and diesel margins are expected to strengthen in Q4 2019, high sulphur fuel oil margins are expected to fall sharply in the quarter, with gradual recovery from Q2 2020.

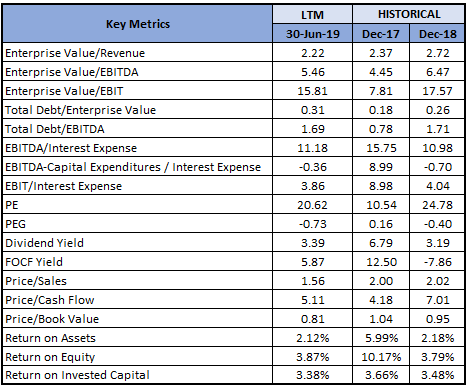

Key Valuation Metrics (Source: Thomson Reuters)

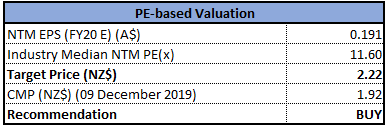

Valuation Methodology: Price-to-Earnings Multiple Approach

Price-to-Earnings Multiple Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company is currently trading at a market price of $1.930 and has a price-to-earnings multiple of 20.960x. During the first half of 2019, the company reported remarkable operational performance which continued through the initial months of the second half. As discussed in the outlook section, the company has various strategic initiatives in place, which are expected to bring in cost advantages for the business. Considering the performance in first half, operational update for September/October 2019, decent outlook, and current trading levels, we have valued the stock using Price/Earnings based relative valuation method and arrived at a target price of lower double-digit growth (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $1.920, down 1.03% on 09 December 2019.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...