The ever evolving and resilient nature of the Telecommunication Industry has been continuously lending support to economic position of New Zealand. The industry is based on a complex yet stable and regulated infrastructure to provide quality connectivity for businesses and households across New Zealand. Prudent to mention is the tech-driven evolution that sets the industry well on a transformational landscape.

Undoubtedly, New Zealand’s telecommunications industry is one to be proud of for the following reasons:

It is worth noting that the country’s telecommunications industry is leading OECD in next-generation networks, investment and affordability. The consumers and businesses in New Zealand are increasingly connecting to the services that offer significantly improved network speeds and capacity. As inter-dependencies between sectors continue to increase, its importance is growing, providing with opportunities and risks. Demand continues to rise in both urban and rural areas, with increases in demand for mobile services and internet. Data requirements are also increasing across the board.

Telecommunications Industry of New Zealand (Source: The New Zealand Telecommunications Forum)

In this sector report, we will try to cover the formation of broader telecommunications sector in New Zealand, how resilient is this sector, key developments and how much funds have been appropriated for the sector. We will also understand how New Zealand is placed in terms of 5G access, how government is helping the sector amidst COVID-19 pandemic and what factors could help broader sector in the long-term. Let’s start with the formation of the sector.

Telecommunications Industry Segments in New Zealand

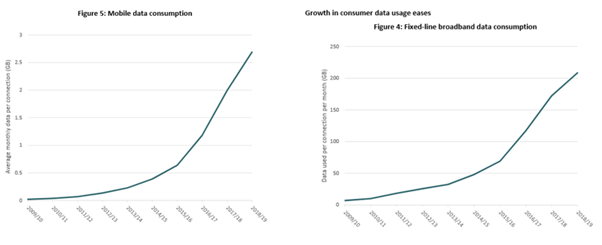

Fixed-line and Mobile Data Consumption (Source: Commerce Commission New Zealand)

How Resilient is Telecommunication Sector?

Telecommunication sector in New Zealand is fairly resilient. International connectivity with the structure of Southern Cross Cable, and the second cable to Australia carry crucial data level.

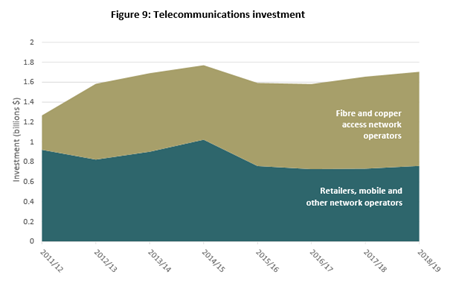

Telecommunications Investment (Source: Commerce Commission New Zealand)

Funding Planned for Telecommunications Sector

The Minister for Broadcasting, Communications and Digital Media is responsible for the appropriations in 2019/20 financial year of:

The Minister for Broadcasting, Communications and Digital Media is also responsible for around $53 million of the non-tax revenue in the year 2019/20. The bifurcation has been explained below:

New Zealand Set to Enter 5G Era

The Government and telecommunications industry has been preparing for the widespread deployment of fifth-generation cellular mobile technology (or 5G). It requires mobile network operators (or MNOs) to gain access to the sufficient radio spectrum to build 5G mobile networks.

What Future Holds for Telecommunications Industry?

The mobile market has moved at a robust rate in the span of previous 20 years and the market is now set to change rapidly in the next decade. However, identifying set of trends which could impact NZ market would always be subjective, particularly as new disruptive innovations could surface at any time – like, incredible growth in the social media usage was impossible to predict until the emergence of Facebook.

We will now have a look at how COVID-19 has impacted the broader sector and how government has been helping it to combat.

Broader Communications Industry Set to Withstand COVID-19 Pandemic

The word on the street has been that media industry was significantly impacted by the outbreak of coronavirus and pessimism prevailed in the minds of the investors. However, this pessimism ended after government included distribution of news publications under the definition of “essential goods.” In addition to that, the government has made an announcement about suite of initiatives which have been valued at $50 million for the media industry to help them in combating the impact of COVID-19 pandemic. The package focuses towards freeing up cash in short-term in order to help the industry to get through this immediate crisis as well as dramatic drop in the advertising revenue witnessed since the commencement of COVID Alert Level 4. Telecos in New Zealand are putting new measures to ensure connectivity for homes and businesses. A slew of data and voice plans have been made available to support telecom customers in the country during the crisis. As of March 25, of the 14 ISPs, 7 have offered free unlimited data plans to all broadband users, 7 have waived late fees and six have given free bonus add-ons for data or voice, among other measures in New Zealand.

Some of the key points of the stimulus package includes:

The broader telecommunications industry also contains print media and broadcasting. Let us now have a glimpse of print media business in New Zealand and how it plans to overcome the challenges.

New Zealand Print Media Under Transformation

In a recent report by Ministry for Culture and Heritage, certain challenges which are being faced by print media and the ways to overcome the challenges were highlighted. It is true when we say that media institutions make unique contribution to health and vibrancy of the democratic societies. Media provides wide range of entertainment, news and information for the audiences and it also reflects languages, experiences and communities of the nations. The emergence of on-demand and online content providers in New Zealand market has diversified consumer choice as well as increased the competition for attention of audience. New Zealand media has been unable to meet the needs and interests of the population and there has been increased competition from international content providers.

What Could be Done to Overcome These Challenges?

The investment of government in public media needs to support public media entities. Audiences in New Zealand choose to access mainstream and targeted content and services which support the local people with access to the range and diversity of content which they value and trust. The preferred approach was to establish new public media entity and to confirm NZ On Air’s continued role with respect to providing contestable funding for the public media content and services in such a way that it complements new entity and helps the wider media sector.

News and Media Industry Gets Sigh of Relief

On March 31, 2020, the New Zealand government refined COVID-19 essential business guidance and included distribution of news publications for communities that are not easily reachable. The guidance has been expanded to cover the news publications which

The New Zealand has been moved to Alert Level 3 and government has issued guidance about the media sector. All the media organisations (which includes community newspapers and magazines) are allowed to carry out operations under Level 3, including production and delivery of the physical product, as long as they could meet requirements for safely operating under Level 3. Online and broadcast delivery of content is preferred provided it is the contactless delivery method.

S&P/NZX 50 vs S&P/NZX All Communications Sector

The outbreak of COVID-19 has impacted the broader New Zealand market and the sectors. However, S&P/NZX All Communications Sector has managed to limit the impact. S&P/NZX 50 fell by 9.72% while S&P/NZX All Communications Sector has witnessed a rise of 0.92%, thereby outperforming the broader index.

.png)

S&P/NZX50 vs S&P/NZX All Communications Sector (Source: Refinitiv (Thomson Reuters))

We will now have a look at the three stocks operating in communications industry in New Zealand (SKT, CNU, TLS)

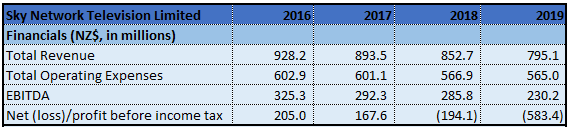

1. Sky Network Television Limited (NZX: SKT) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-cap: $122.14 Million)

Business Description: Sky Network Television Limited is an entertainment company dedicated to connecting New Zealanders to the sport and stories they love.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company comes under “Essential Services” with its news and entertainment content delivered to New Zealanders over its reliable satellite platform. The company has taken various measures to encounter the impact of pandemic. It has reduced its operating expenses, deferred non-essential capital projects and implemented a travel and hiring freeze. The company has also made a range of offers to residential and commercial customers with immediate effect to help them through the lockdown and to offer more value to residential customers.

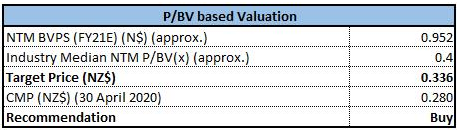

Valuation: The company has made an announcement that it has withdrawn its revenue and EBITDA guidance for the year ended June 30, 2020. However, the company has wrapped up the purchase of entertainment streaming service Lightbox from Spark, enabling Sky to merge Lightbox with its own entertainment streaming service Neon, creating super-charged service for the customers of New Zealand with best content from NZ and around the world. We have applied P/BVPS based relative valuation (on an illustrative basis) and the target price reflects the growth of lower double-digit (in % terms).

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

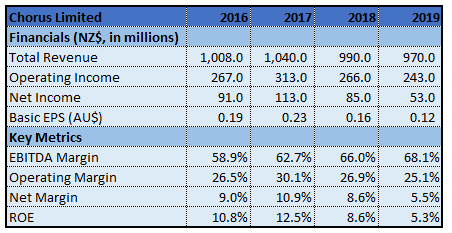

2. Chorus Limited (NZX: CNU) (Recommendation: Hold (Subject to Certain Factors), Potential Upside: Lower Double-digit) (M-cap: $3.16 Billion, Gross Dividend Yield: 4.490%)

Business Description: Chorus Limited (NZX: CNU) is a New Zealand’s leading fixed-line telecommunications network operator.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has suspended its non-essential field activity to support the government objective of eliminating the risks of spreading COVID-19. It has reduced its FY20 gross capital expenditure guidance from a prior range of $660 million to $700 million, to a new range of $610 million to $650 million. The company has increased its FY20 EBITDA guidance to a new range of $640 million to $655 million, from a previous range of $625 million to $645 million. The company’s development on improving its business and lowering costs, all together with broadband connection performance, has offered it the trust to raise FY20 EBITDA guidance. Dividend guidance for FY20 is unchanged at 24 cents per share, subject to no material adverse changes in circumstances or outlook.

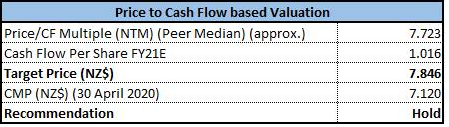

Valuation: The company recently announced that it has entered into an extension to $550 million committed bank facility, which provides it with financial flexibility and funding certainty. It would also support its potential future funding needs. We have valued the stock using P/CF Based Relative Valuation (on an illustrative basis) and the target price reflects the growth of lower double-digit (in % terms). However, the company has suspended its planned activity like UFB communal rollout, subdivision build, door-to-door ibre campaigns, etc. Therefore, we advise the investors to "Hold" the stock at $7.120.

P/CF Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

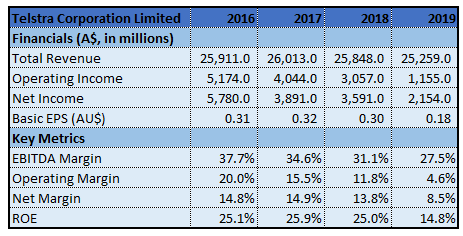

3. Telstra Corporation Limited (NZX: TLS) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-cap: $39.01 Billion, Gross Dividend Yield: 5.053%)

Business Description: Telstra Corporation Limited (NZX: TLS) provides telecommunications and information services for domestic and international customers.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: As per the CEO of the company, Mr. Penn, the ultimate impact from COVID-19 on the company difficult to assess at this time. The company’s FY2020 guidance is for up to $500 million growth in the underlying EBITDA (after excluding in-year nbn headwind). The total income is expected to in between $25.3 billion and $27.3 billion, and the free cash flow after operating lease payments is expected to be at the bottom range of $3.3 billion and $3.8 billion. The company has also taken certain measures amid COVID-19 pandemic. It has put a hold on any further job reductions.

Valuation: The company stated that its continued access to low-cost capital and A-band credit rating reflects strength of the business and attractiveness to global capital markets. Additionally, Telstra remains confident on the long-term outlook. We have valued using P/E Based Relative Valuation (on an illustrative basis) and the target price reflects the growth of higher single-digit (in % terms).

.png)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

.png)

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...