Company Overview: Telstra Corporation Limited (NZX: TLS) is Australia’s leading telecommunications and technology company, that provide a full range of communications services and competing in all telecommunications markets. In Australia, the company provides 18.3 million retail mobile services, 3.7 million retail fixed bundles and standalone data services as well as 1.4 million retail fixed standalone voice services. The company has business partnerships with complementary brands Belong and Boost Mobile. With the help of Telstra Foundation, the company partners with not for profits driving social innovation with technology.

TLS Details

Investment Summary:

High Internet Speed & Usage Growth Drivers for Telecoms: Telstra Corporation Limited (NZX: TLS) is Australia based leading telecommunications and technology company which offers a full range of communications services for domestic and international customers. The market capitalisation of the company stood at ~$39.72 billion on 25th May 2020.

Under its T22 strategy, the company has emphasis over continuing strong performance with reduction in costs and delivering new and simplified products and services to its customers. Till now, the strategy has helped reduce underlying fixed costs by $422 million, or 12.1%, bringing the total underlying fixed cost reductions to around $1.6 billion since FY16. Talking about statistics, by the end of first half of FY20, the company had 2.4 million services on its new, radically simplified plans. It delivered more than 1.7 million Smart Modems to homes around the country and more than 1.2 million customers are now able to enjoy the benefits of being a Telstra Plus member.

Telstra’s ongoing research and investment continues to make Australia a global leader in 5G, supported by the increase in number of customers enjoying access to Telstra’s world-leading 5G mobile network and a growing range of 5G-enabled devices. Global credit rating agencies, S&P and Moody’s, reaffirmed Telstra’s credit rating to A- (stable) and A2 (stable), respectively. The company’s continued access to low-cost capital and A-band credit rating demonstrates the strength of the business during this very volatile time.

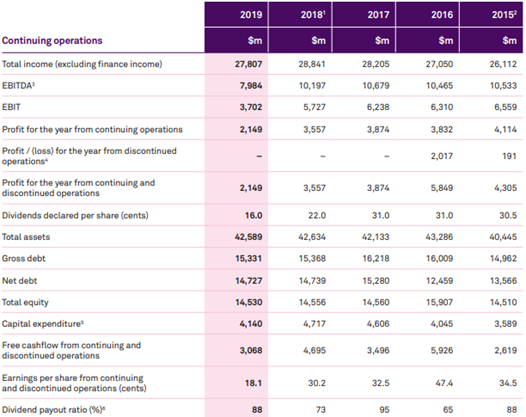

FY19 will go down in the company’s history as strategic year wherein the existing business strategy was reviewed and new strategies in form of T22 and costs reduction measures were implemented. The costs involved in implementing strategies had immediate impacts in terms of softer performance for FY19. The company reported decline in total income by 3.6% to $27.8 billion, EBITDA de-grew by 21.7% to $8.0 billion and NPAT decreased by 39.6% to $2.1 billion. However, the company witnessed continued customer growth. The company’s Internet of Things (IoT) business exceeded industry growth rates. Dividend payout ratio for the financial year stood at good level of 88%. There was also marginal decrease in gross and net debt.

Historical Financial Performance (Source: Company Reports)

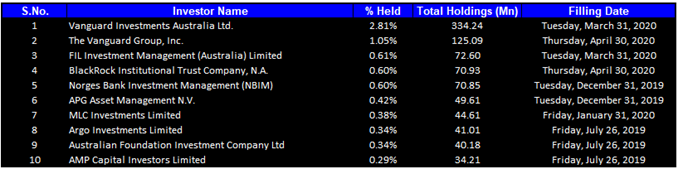

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 7.43% of the total shareholding. Vanguard Investments Australia Ltd. and The Vanguard Group, Inc. hold maximum interests in the company at 2.81% and 1.05%, respectively.

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

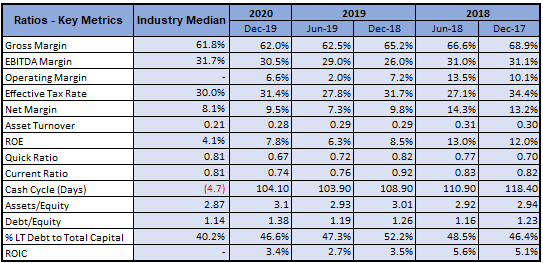

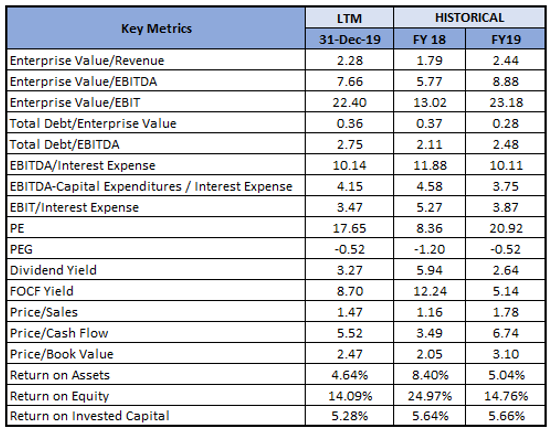

A Quick Look at Key Metrics: Its gross margin and net margin for H1FY20 stood at 62.0% and 9.5%, better than the industry median of 61.8% and 8.1%, respectively, implying decent operating efficiency of the company than the peer group. ROE for H1FY20 stood at 7.8%, better than the industry median of 4.1%, implying that the company generated better returns for its shareholders than its peer group.

Key Metrics (Source: Refinitiv (Thomson Reuters))

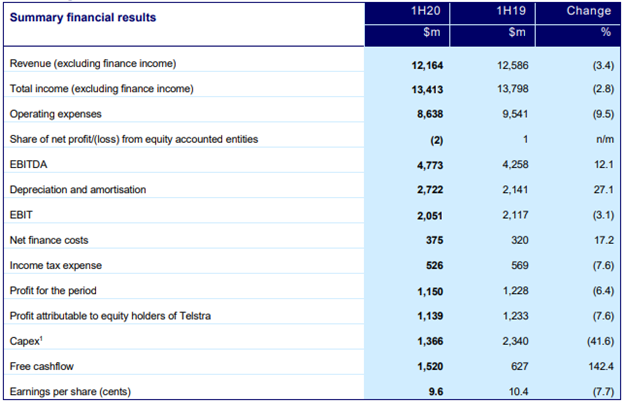

Subdued Performance in H1FY20: The company posted total income of $13.4 billion for the first half period of FY20, a decline of 2.8% on previous corresponding period (pcp). Underlying EBITDA declined by 6.6% (on pcp) to $3.9 billion, while underlying EBITDA (excluding the in-year nbn headwind) grew by ~$90 million. Net profit after tax (NPAT) for the period was reported at $1.2 billion, a decline of 6.4% on pcp.

Segmental Performance: Income from Telstra consumer and small business declined by 2.1% (on pcp) to $7,063 million, impacted by a 7.4% decline in fixed as a result of ongoing standalone fixed voice decline and a 5.7% decline in mobile services revenue as declining Average Revenue Per User (ARPU) more than offset customer net additions.

Income for Telstra Enterprise decreased by 1.8% to $3,882 million as growth in international was more than offset by a decline in domestic.

Networks and IT income increased by 29.4% to $44 million.

Telstra InfraCo income excluding internal access charges decreased by 12.0% to $1,369 million due to expected declines from Telstra Wholesale fixed legacy and nbn commercial works, partly offset by increased recurring nbn DA receipts.

H1FY20 Key Financial Metrics (Source: Company Reports)

Disruption in Foxtel Business Propels Write Down of TLS’ Share: The company is expected to make a non-cash impairment and write down of the carrying value of its 35% stake in Foxtel. The announcement follows the write down in value of Foxtel by News Corp. This impairment charge is expected to be around A$300 million, following which Telstra’s share in Foxtel will fall from A$750 million to around A$450 million. The reason can be attributed to the fact that Foxtel has been facing industry disruption for several years and further worsened from the covid-19 spread affecting global sports, temporarily closing pubs and reduction in advertisement spends from the corporates. However, on the positive side, sports will return, and through premium content such as the multi-year deal just signed with WarnerMedia including exclusive HBO and Warner Bros. content, Foxtel’s offerings will continue to be highly attractive entertainment options.

Issue of €500 Million Bond to Strengthen Balance Sheet: TLS priced the €500 million bond issue (the Notes) under its Debt Issuance Program Offering, for general corporate purposes including prefunding of future debt maturities. Since mid-March, the company has secured an additional $940 million in bank facilities, taking the committed bank facilities to the figures of $3.6 billion.

FY20 Guidance Update: Due to impact from the pandemic, the company has revised its FY20 guidance towards the bottom end of the range for free cash flow and underlying EBITDA. Underlying EBITDA growth (excluding the in-year NBN headwind) can now be expected at the bottom end of the range of $0-500 million, while capex can be expected at the top end of the same range.

What to Expect: Like any other businesses, telecommunication business is not immune to COVID-19 as it is having profound impact on business across the countries. The company is yet to assess the ultimate impact. The management expects COVID-19 impact to be material and would depend on how the situation and its impact on economy and customers evolve. As per the release, with the inclusion of new products and services, customer experience has improved, underpinned by increase in number of customers interacting online.

Its multi-brand strategy continues to deliver growth in customer numbers, particularly in mobile. It now has 5G coverage in selected areas in 32 cities and regional areas, progressing towards target of 35 by the end of FY20.

Key Risks: The company operates in a business which is constantly evolving and facing rapid change. Some of the important challenges include transformation and competition, privacy and cyber security, major regulatory changes, etc. The company is also exposed to foreign exchange rate risks owing to its business presence in overseas markets. The management has realization of the impact of COVID-19 on small business and consumer customers and accordingly, it has announced several measures providing relief to them. The impact of initiatives taken to support small business and consumers on operating profit is going to be short-lived and, with the improvement in business sentiment and business activities, things will become normal, benefiting the company.

The company’s T22 strategy was rolled out 2 years ago and it has made good progress against it. At its heart, this strategy is premised on radically simplifying the business and removing customer pain points, digitising as well as moving customers to digital channels, simplifying structure, introducing new ways of working, establishing InfraCo and leaving the legacy behind.

Telecommunication Sector Outlook: As interdependence between sectors continue to increase, significance of telecommunication sector has risen immensely. With several businesses turning online, there is going to be big rise in mobile and internet data demand.

As per data provided by the Commerce Commission in Annual Monitoring Report, mobile connections continue to increase. The report also notes that there has been dramatic increase in data use. The average data consumption per fixed broadband connection rose from 172GB to 208GB per month. The average data consumption per mobile connection witnessed a rise from 2.0GB to 2.7GB per month.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

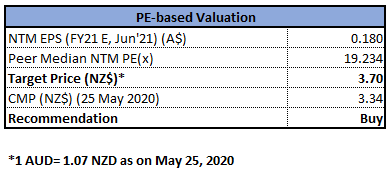

Valuation Methodology: Price to Earnings (P/E) Multiple Based Relative Valuation (Illustrative)

Price to Earnings (P/E) Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart:

(Source: Refinitiv (Thomson Reuters))

Note: Green color lines are Bollinger Bands, yellow lines are retracement lines and yellow colour dotted line is Parabolic SAR. Technical tool Parabolic SAR uses trailing ‘Stop’ and ‘Reverse’ method to identify suitable exit and entry points. It appears as dotted line either above or below the underlying stock’s price, depending upon the direction of the stock.

The stock while on winning streak, made the high of $4.12 and from there it was caught under bearish trap, pushing the stock down to the low of $2.96. The stock moved up twice beyond 38.2% retracement level of $3.40 in several recent-past weeks, but it could not hold on positive momentum and slipped down close to 23.6% retracement level of $3.23 and gave close at $3.27 in the previous week. The on-going week has positive start wherein the stock has same open and low price of $3.30 while its closing is at peak price of $3.34 thereby confirming intactness of bullish momentum.

Technical indicators such as MACD with bearish cross-over but curve at the end pointing up, and RSI with 41 reading suggest gaining of bullish momentum for the stock.

Going forward, the stock may have resistance around $3.68 as provided by 61.8% retracement level while on price further retreating, it may have good support around $3.23 which happens to be 23.6% retracement level.

Stock Recommendation: In light to the Covid-19 spread and its implications, the company has implemented certain measures such as emphasis over productivity program to reduce underlying fixed costs by $2.5 billion annually by the end of FY22. It would be recruiting an additional 1,000 temporary contractors in Australia to help manage call centre volumes. It has brought forward $500 million of capex from the second half of FY21 into CY20, which are being used to increase capacity in its network, including further accelerating the roll out of 5G and injecting much needed investment into the economy.

The recent bond issue along with the additional bank facilities are well below Telstra’s current average cost of funds and demonstrates TLS’ financial strength and attractiveness to global capital markets, while further strengthening its liquidity position during a volatile period in global financial markets.

Considering the aforesaid facts, recent updates and H1FY20 results, we have valued the stock using Price to Earnings (P/E) Multiple Based Relative Valuation (on an illustrative basis) and we have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$3.34 per share, up by 2.14% on May 25, 2020.

.png)

TLS Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...