The technology sector, which is characterized by the combination of ICT as well as high-tech manufacturing, happens to be a dynamic and growing part of NZ economy, reflecting increased levels of innovation, connectedness along with expenditure on Research & Development. The total tech sector contributed 8% to GDP in 2015, added 9% to exports and employed 5% of the workforce.

The revenues of ICT firms in the top 200 grew by 15.9%. Revenues of high tech manufacturers increased by 7% and biotech firms increased by 6%. The international sales of the country’s top 200 tech exporters witnessed a growth of 11.3% to $8.7 billion, resulting in an additional $882 million in terms of sales in 2019.

Key Data (Source: NZTech)

The economic and social gains that the technology has enabled is immense. Technology is redefining the way people live in. In just over a decade, technology sector contributions to GDP growth has been higher than any other OECD countries. The world recognizes the country’s innovation, quality, and ease of doing business.

The ICT Sector

New Zealand’s ICT sector (Information and Communications Technologies) is an advanced and diverse sector, that covers health IT, wireless infrastructure, geospatial, telecommunications, agricultural technology and many more. It is a breeding ground for innovation and strives effectively on the global stage.

The companies under ICT sector of New Zealand have gained an international status for being resilient, flexible, compliant, and entrepreneurial.

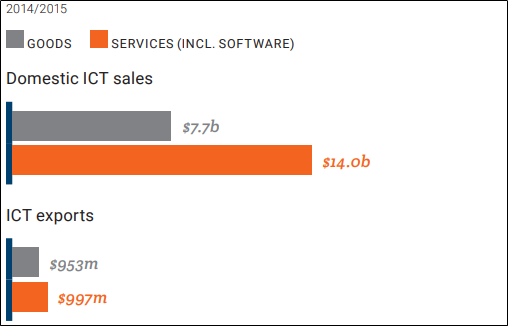

This sub-sector directly generated more than $23 billion in output and contributed $12.5 billion or 6.2% of GDP in 2015. Sales of ICT services have been increasing at a faster pace than goods, and have been expanding as a proportion of the broader ICT sector since 2008.

New Zealand’s ICT Sector Sales (Source: NZTech)

The High-Tech Manufacturing Sector

As per the New Zealand Technology Industry Association, high-tech manufacturing has demonstrated exciting growth in the past few years despite the fact that total manufacturing decreased from 26% of GDP in 1972 to ~15%. High-tech manufacturing is a comparatively small subset of the manufacturing sector and accounts for less than 22% of economically significant manufacturing firms. The high-tech manufacturing sector is comprised of a small number of large firms like F&P Healthcare, Glidepath, Gallagher Group, Compac Sorting as well as Scott Technologies.

The sector employs about 44,161 people and they are mainly located in Auckland (54%), followed by Christchurch (25%) and Hamilton (3%).

How Digitisation Helps Broader Technology Sector

While the technology sector is the fastest-growing sector, there are huge opportunities in digital space. Digital technologies are virtually transforming all aspects of people’s lives. It is creating big opportunities in areas such as precision healthcare, e-education, and autonomous vehicles.

As per the Productivity Commission Report, New Zealand’s current expenditure on R&D as a percentage of GDP is 1.3 percent which is low compared to Israel and Korea of 4.3 percent and 4.2 percent, respectively. The R&D spending in New Zealand is also below Australia, which spends 2.1 percent of GDP. The ministry has the realization of this fact. The government has committed to raising R&D expenditure to 2 percent of GDP over 10 years. Nonetheless, the country is fast adapting itself to innovations that take place in the technology sector.

Young New Zealanders, with their technological thrust, are driving the nation on a technological path. Whether it is agritech, which helps produce more food for the country; biotech, which helps improve health; and fintech, helping New Zealand prosper into the future.

Challenges Faced by IT Sector

There have been discussions on how increased use of technology impacts employment, whether and how technological forces are shaping work, and how New Zealanders should best prepare for the change in the future. This assumes greater significance in the present context as New Zealand is emerging out from the pandemic-led long lockdown, which has derailed economic growth and has created a huge unemployment situation in the process.

Since we now have a broad idea of the IT sector, it is important to look at the performance of some companies operating in the same sector (SKO, SPY, PPH and IKE).

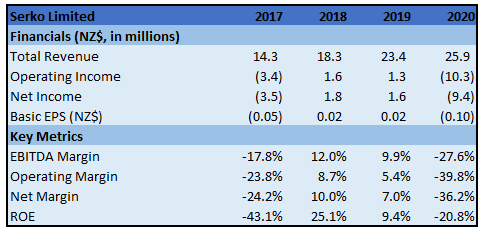

1. Serko Limited (NZX: SKO) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$307 million)

Business Description: The purpose of Serko Limited (NZX: SKO) revolves around transforming the way businesses manage expenses as well as travel.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company considers itself to be well-positioned for growth when the travel industry recovers, and trading conditions start to improve. The company has a strong hold in Australasia, with its major transactions being domestic and Trans-Tasman in home markets.

Key Risks: The company has some exposure to foreign exchange risk because of its transactions denominated in foreign companies.

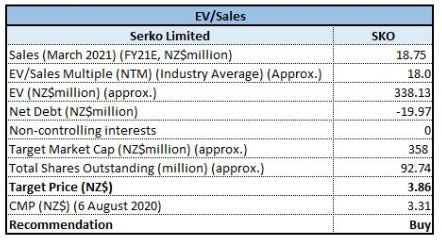

Valuation: The company is now mainly focussing on domestic travel within North America, where it remains to add resellers to its platform and maintain development work to localise the content in the region. It also has a strong balance sheet and continuing commitment towards investment, which would help existing and prospective customers. We have applied EV/Sales based relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms).

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months.

Thus, we give a “Buy” recommendation at the current market price of NZ$3.310 per share on August 6, 2020.

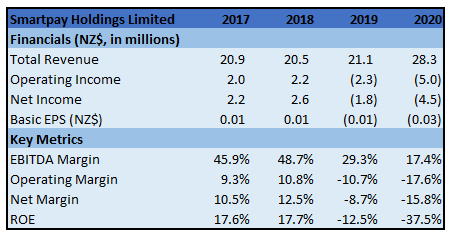

2. Smartpay Holdings Limited (NZX: SPY) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$140.34 million)

Business Description: Smartpay Holdings Limited is ANZ’s largest independent full-service Electronic Funds Transfer at Point of Sale (EFTPOS) provider.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: With COVID-19 largely behind, the company has prepared the business to resume and accelerate for growth. It has progressed with an external capital raise which was strongly supported by both current and new shareholders. The money from capital raise will allow it to continue to follow its growth strategy and also increase its financial strength by significantly reducing debt.

Key Risks: The key risks arising from the company’s financial instruments, assets and liabilities are risks in the fluctuation of foreign exchange rates and interest rates, liquidity risk, and credit risk.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has formed ‘Bullish Rectangle’ which is continuation pattern with potential of break to the upside. Technical indicator RSI with around 62 reading suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around the upper Bollinger band of $0.79 while support could be around $0.60.

Valuation: The company expects to resume its growth with the support of its recent capital raise and, hence, expects another strong performance for the rest of the financial year. On TTM basis, its EV/Sales multiple stood at 6.1x as compared to industry average of 27.3x. However, its P/CF multiple stood at 20.7x lower than the industry average of 27.1x.

Thus, we give a “Buy” recommendation at the current market price of NZ$0.670 per share, up by 4.69% on August 6, 2020.

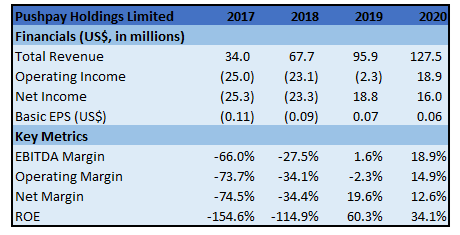

3. Pushpay Holdings Limited (NZX: PPH) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$2.14 billion)

Business Description: Pushpay Holdings Limited offers donor management system, including finance tools, donor tools as well as a custom community app, to the non-profit organisations, faith sector and education providers in Canada, the US, New Zealand, and Australia.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: In the coming future, the company anticipates further strong growth in the revenues as it continues to implement its strategy to gain market share in the medium term. The company is expecting to report EBITDAF of between US$48.0 million and US$52.0 million for the full year ending 31 March 2021.

Key Risks: The company is exposed to various financial risks including credit risk, liquidity risk and market risk.

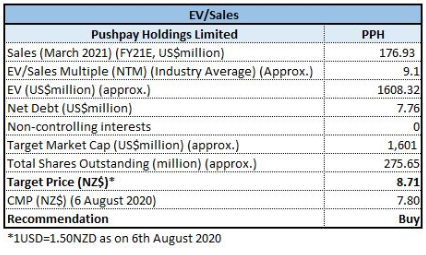

Valuation: We have applied EV/Sales based relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms).

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months.

Thus, we give a “Buy” recommendation at the current market price of NZ$7.800 per share, up by 0.65% on August 6, 2020.

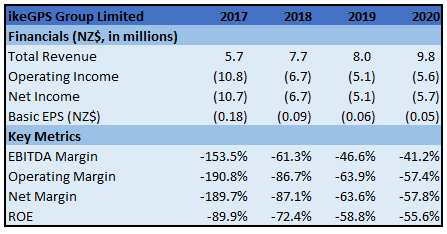

4. ikeGPS Group Limited (NZX: IKE) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$115.16 Million)

Business Description: ikeGPS Group Limited is a technology company, seeking to be the standard for analysing, collecting and managing pole as well as overhead asset information for communications companies, electric utilities and their engineering service providers.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: Although the company’s North American customers experienced a significant slow-down in activity from March to May 2020 due to the abrupt uncertainty because of Covid-19, their operations have restarted in June, even with the presence of coronavirus in the U.S. The company is continuously monitoring the risks which are related to coronavirus and, operationally, it has transitioned its U.S. operation to mostly remote working, while the company’s operation in NZ is back to “in-office” status in the environment of Level-1.

Key Risks: The key risks which arise from the company’s financial instruments are liquidity risk, credit risk, foreign currency risk and interest rate risks which arise in the usual course of the company’s business.

Valuation: On TTM basis, its EV/Sales multiple stood at 10.2x as compared to industry average of 27.3x.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci projection lines.

The stock remained very resilient throughout the previous week. For the on-going week, the stock on this date has given stronger close at $0.92 thereby exhibiting strength in uptrend. Technical indicator RSI with around 64 reading suggests strong bullish momentum for the stock.

Going forward, the stock may have immediate resistance around 38.2% Fibonacci projections level of $1.0374 while support could be around $0.8000.

Thus, we give a “Buy” recommendation at the current market price of NZ$0.920 per share, up by 5.75% on August 6, 2020.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...