Company Overview: Summerset Group Holdings Limited (NZX: SUM) provides a range of living options and care services to more than 5,500 residents. It has over 31 retirement villages across New Zealand. Additionally, it has eight sites for development in Milldale (Auckland), Parnell (Auckland), Prebbleton (Canterbury), Rangiora (Canterbury), Waikanae (Kapiti Coast), Blenheim (Marlborough), Cambridge (Waikato) and Lower Hutt (Wellington), plus two properties in Victoria, Australia, taking the total number of sites to 41. Its existing villages are in Aotea, Avonhead, Bell Block, Casebrook, Dunedin, Ellerslie, Hamilton, Hastings, Havelock North, Hobsonville, Karaka, Katikati, Kenepuru, Levin, Manukau, Napier, Nelson, New Plymouth, Palmerston North, Papamoa Beach, Paraparaumu, Richmond, Rototuna, St Johns, Taupo, Te Awa, Trentham, Wanganui, Warkworth, Whangarei and Wigram.

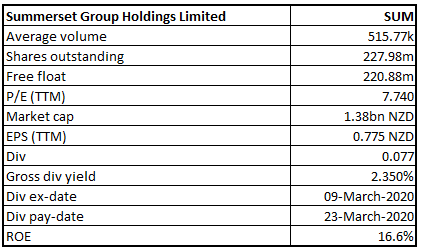

SUM Details

Investment Summary:

Rise in Aging Population in NZ and Aus. Boosts Aged Care Facilities’ Outlook: Summerset Group Holdings Limited (NZX: SUM) is one of the leading operators and developers of retirement villages in New Zealand, with 31 villages completed and many others in developing stage across the country. The market capitalisation of the company stood at ~$1.38 billion as on 11th May 2020.

Looking at the past performance over FY15 to FY19, total revenue and net income of the company have grown at a CAGR (compounded annual growth rate) of ~22.30% and 20.12%, respectively. The company’s total revenue improved from $68.8 million in FY15 to $153.9 million in FY19, and net income improved from $84.2 million in FY15 to $175.3 million in FY19. During FY19, the company made important announcement about the acquisition of a second Australian property in Torquay, on the Bellarine Peninsula southwest of Melbourne. Its significance can be marked by the fact that 8.3-hectare property is situated near shopping centres and amenities in the coastal surf town.

Other important development includes purchase of an 8.0-hectares in Cranbourne North, Melbourne, in September 2019 for the company’s first Australian retirement village, which is expected to open for residents in late 2021/early 2022.

Historical Financial Performance (Source: Company Reports)

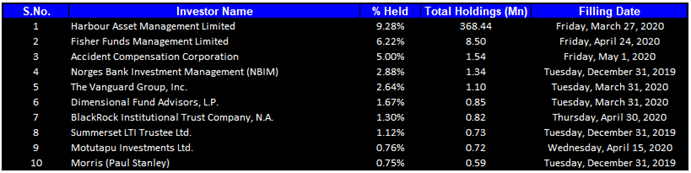

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 31.62% of the total shareholding. Harbour Asset Management Limited and Fisher Funds Management Limited hold maximum interests in the company at 9.28% and 6.22%, respectively.

In the first week of May 2020, Milford Funds Limited and Accident Compensation Corporation (ACC) became substantial holders to the company with stake of 5.267% and 5.002%, respectively.

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

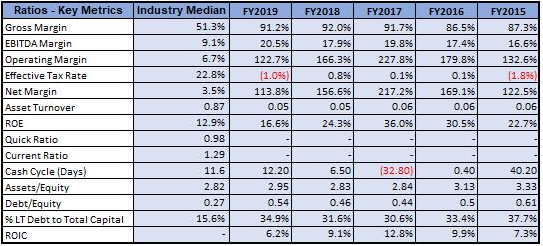

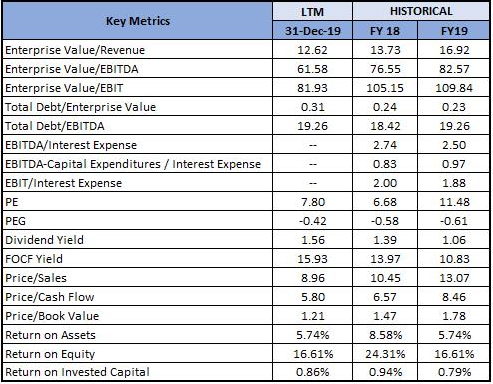

A Quick Look at Key Metrics: Its gross margin, EBITDA margin and net margin for FY19 stood at 91.2%, 20.5% and 113.8%, better than the industry median of 51.3%, 9.1% and 3.5%, respectively, implying decent financial footing of the company. RoE for FY19 stood at 16.6%, better than the industry median of 12.9%, implying that the company generated better returns for its shareholders than its peer group. Its return on invested capital (or ROIC) for FY19 stood at decent figure of 6.2%.

Key Metrics (Source: Refinitiv (Thomson Reuters))

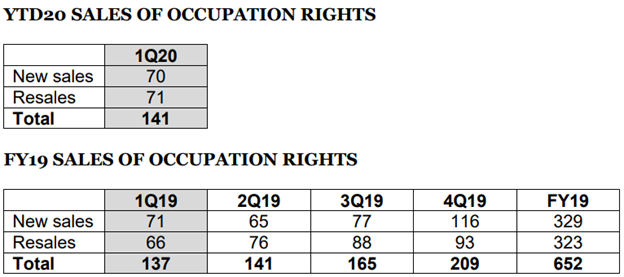

Normal Sales for the First Quarter: The company-maintained sales at normal level for the first quarter ended 31st March 2020. During the quarter, the company reported 141 sales comprising 70 new sales and 71 resales despite including one week of the alert level 4 lockdown. As of March 31, the company was having a further 98 new sales contracts in place and 73 resales contracts in place.

March’20 Key Information (Source: Company Reports)

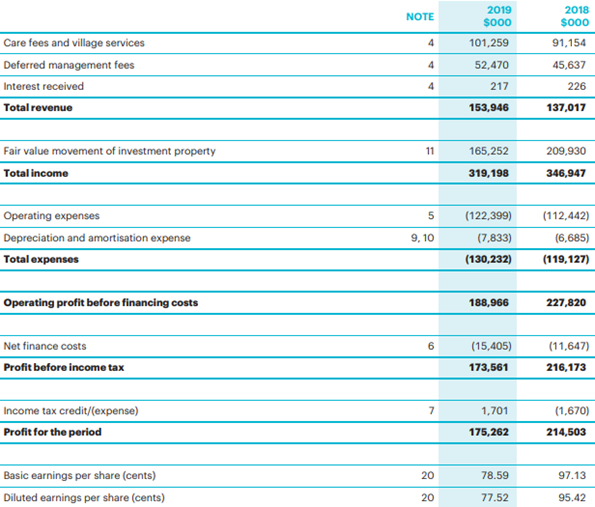

Noticeable Lift in Second Half Supported FY19 Figures: The company posted underlying profit after tax of NZ$106.2 million, an increase of 8% on previous year. Its net profit, including the impact of unrealised movements in the fair value of investment property, declined by 18% to NZ$175.3 million, as compared to previous year. This was due to fewer deliveries of retirement unit in the financial year. However, on positive front, there were noticeable lift in the activity in the second half of FY19, underpinned by record 38% sales in the final quarter of FY19. Annual growth in underlying profit averaged 38% since SUM listed on NZX in the month of November 2011. Total of 354 new homes were delivered in FY19, as compared to 454 in FY18.

The Board of Directors declared an unimputed final 2019 dividend of NZ 7.7 cents per share, with record date and payment date of 10th March 2020 and 23rd March 2020, respectively. This takes the total dividend for FY19 to NZ 14.1 cents per share, an increase of 6.8% on previous year.

FY19 Income Statement (Source: Company Reports)

Key Risks: The company is susceptible to certain risks such as credit risk, market risk, interest rate risk and liquidity risk. It manages its credit risk by holding low level of cash (exposure) with the principal banker. Receivables balances are monitored on an ongoing basis and funds are placed with high credit-quality financial institutions. Its exposure to interest rate risk is always managed by seeking to obtain the most competitive rate of interest from the market at any available time.

Retirement Village Outlook: As per the population report published over the government websites, New Zealand population as on December 31, 2019, stood at ~5 million, and it is growing at a yearly rate of 1.4%. Going on stats, latest projection indicates that the population with age of 65 years and above will represent 1 in 4.5 citizens by 2036, which figures out to be 1,258,500 million people. This number is 547,300 more than age population (65 years and above) as compared to 711,200 in 2016. With this rate, aged care facilities will always find a demand which can be in terms of retirement villages or shelter homes, etc.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

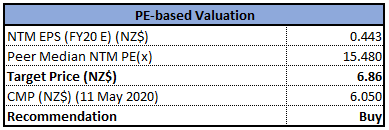

Valuation Methodology: Price to Earnings (P/E) Multiple Based Relative Valuation (Illustrative)

Price to Earnings (P/E) Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands, yellow lines are retracement lines and orange colour dotted line is Parabolic SAR.

While on northward journey, the stock ascended to peak of $9.25 but from there it was caught under selling pressure which got further intensified, bringing the stock price down to the low of $3.35. The stock rebounded beyond 50% retracement level of $6.30 from the low but it could not hold on positive momentum, so built and fell to 38.2% retracement level of $5.60 but closing was above a week prior to the previous week close thereby forming bullish Hammer on chart, suggesting bullish reversal. In the today’s session of the on-going week, the stock gave close above the previous week close thereby exhibiting bullish momentum remaining intact for the stock.

Technical indicators such as MACD with bearish cross-over and flattish curve at the end, and RSI with 42 reading and flattish curve at the end suggest flattish momentum for the stock.

Going forward, the stock is expected to continue maintaining uptrend wherein it may have resistance around 61.8% retracement level of $7.00. However, on price retreat, it could have good support around 38.2% retracement level of $5.60.

Stock Recommendation: The company made some important acquisition and purchases of properties in Australia in FY19, with one expected to operate in late 2021 or by early 2022. This was done after a meticulous effort in understanding and familiarising the Australian market for around 18 months. It also reported that there is an unmet demand for retirement villages in Australia which offer a continuum of care model, which means accommodation from independent living through to fully supported rest home or hospital care. Summerset would be replicating its successful integrated-village model from New Zealand in the Australian market as well.

In a nut shell, the company is increasing its number of properties across the geographies, underpinned by holding enough land across New Zealand and Australia to build another 5,380 retirement units and 826 care beds, providing it with the flexibility to double the size of its business over time.

Considering the aforesaid facts, we have valued the stock using Price to Earnings (P/E) multiple based method (on an illustrative basis) and we have arrived at a target price of lower double-digit growth (in % terms).

.png)

SUM Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...