Company Overview: SRG Global Limited (ASX: SRG) is an engineering-led specialist construction, maintenance, and mining services across the entire asset life-cycle. SRG Global operates in various sectors including Infrastructure Construction, Infrastructure Maintenance, Water, Oil and Gas, Energy, Mining and Transport sectors. The construction segment consists of supplying integrated products and services to customers involved in the construction of complex infrastructure, whereas the asset segment supply integrated services across the entire life-cycle. The mining segment provides ground solutions including production drilling, ground and slope stabilization, design engineering and monitoring services..png)

SRG Details

.JPG)

Decent Increase in Revenue and Record Work in Hand: SRG Global Limited (ASX: SRG) is an engineering-led specialist construction, maintenance and mining services group operating across the entire asset life-cycle. As on 03 July 2020, the market capitalization of the company stood at ~$109.22 million. The company has a disciplined business approach and is focused on its long-term strategy to create a balanced portfolio with a mix of both recurring and project-based revenue streams. It has an exceptionally diverse capability and skillset. During FY19, the company reported a record work in hand of $708 million and witnessed an increase in revenue to $506.4 million from $431.6 million. This was mainly due to TBS acquisition in New Zealand and the acquisition of the remaining 49% of Gallery Facades. SRG also saw a step-change in the diversity of its revenue base in a way that the current work in hand is comprised of approximately 70% of recurring and term revenues. During the year, challenging market conditions, delays in the construction of large-scale projects and carrying costs of maintaining capability impacted adjusted EBITDA and EBIT of the company, which stood at $32 million and $22.5 million, respectively. However, SRG reported a robust balance sheet with a cash balance of $58.3 million. The decent financial and operational performance of the company enabled the Board to declare a final dividend of 0.5 cents per share, bring the total dividend to 1.5 cents per share for FY19.

During 1H20, the company reported solid operational performance in Mining Services, Specialist Facade and Civil Construction. SRG retains ahealthy balance sheet with liquidity and steady growth in Asset Services. It has a strong pipeline of opportunities across growth sectors.

The company is ensuring the sustainable success of SRG Global into the coming years and is building momentum with several contract wins and record work in hand. It is aiming to develop the level of recurring revenue to balance the current weighting towards project-based revenue. .png)

FY19 Financial and Operational Highlights (Source: Company Reports)

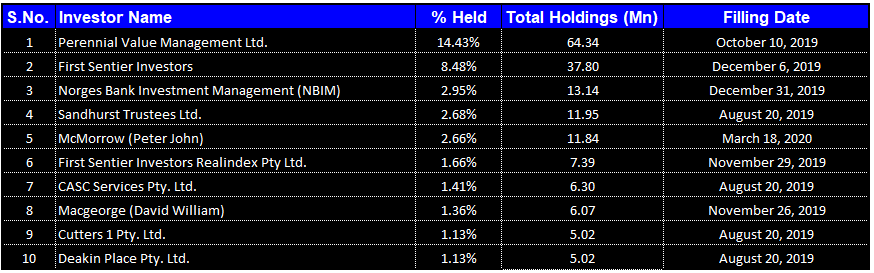

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of SRG Global Limited. Perennial Value Management Ltd. is the largest shareholder in the company, with a percentage holding of 14.43%.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

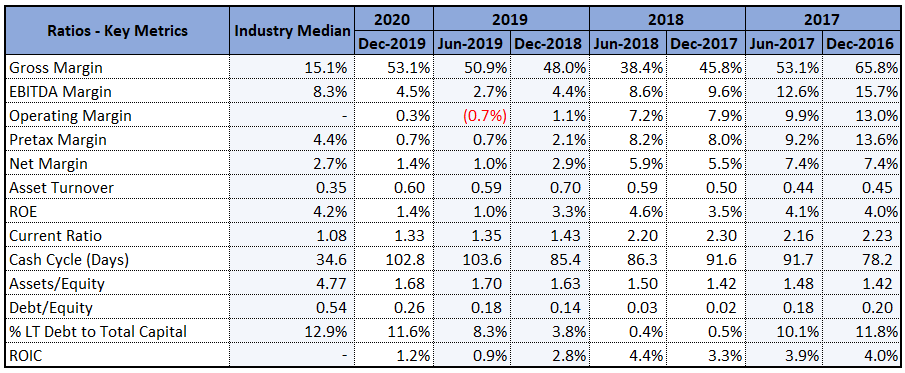

Well Management of Costs and Increasing Returns to Shareholders: During 1H20, gross margin of the company stood at 53.1%, higher than the industry median of 15.1%. In the same time span, net margin of the company was 1.4%, up from 1% in 2H19. The higher gross and net margin indicate that the company is managing its costs well and is able to convert its revenue into profits. During 1H20, EBITDA margin of the company witnessed an increase over the previous half and stood at 4.5%, up from 2.7% in 2H19, indicating increased profitability. In the same time span, current ratio of the company stood at 1.33x, higher than the industry median of 1.08x. This implies that the company is liquid enough and can pay off its current liabilities using its current assets. During 1H20, Return on Equity witnessed a slight increase over the previous half and went up to 1.4% from 1% in 2H19. This indicates that the company is well deploying the capital of its shareholders and is capable of generating profits internally. In the same time span, debt/equity ratio of the company stood at 0.26x lower than the industry median of 0.54x and assets/equity ratio of the company was 1.68x as compared to the industry median of 4.77x. The lower assets/equity ratio and debt/equity ratio indicate that the business is financed with a more significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Refinitiv, Thomson Reuters)

Strong Operational Performance and Resilient Balance Sheet: During 1H20, the company reported an increase of $28.6 million in adjusted revenue to $267.1 million and an adjusted EBITDA of $12.1 million. In the same time span, SRG also reported an opportunity pipeline of $5.7 billion across growth sectors with imminent contract awards and robust growth in Asset Services with an increase of 172% in work in hand in the past 12 months to $737 million. During the half-year, the company retained a strong balance sheet with the liquidity of $67.2 million and low gearing at 6%.The company has also announced that it has been awarded a new five-year drill and blast contract with Saracen Mineral Holdings Limited of around $70 million wherein it will offer specialist drill and blast services including production drilling, explosives supply and management as well as grade control drilling to Saracen. This contract will further diversify SRG’s customer base and will add to its long-term work in hand.

Key Risks: The group’s activities are exposed to a variety of risks including financial risk, market risk, including currency risk, interest rate risk and other price risks, credit risk and liquidity risk. Due to the outbreak of COVID-19 crisis, the Government of New Zealand and Australia imposed a complete shutdown of operations which impacted FY20 EBITDA. Compliance measures and industry pressures due to the pandemic resulted in the disruption of international projects. The company is anticipating credit losses and may incur increasing costs for the provisions.

Outlook: In the recent market update, the company stated that it has reduced its fixed cost base and is focusing on core business, clients, and geographies. Despite the short-term challenging market conditions, it retains a healthy financial position and is well-positioned for long-term sustainable growth and strong exposure to growth industry sectors. The company has provided guidance for FY20, wherein it expects underlying EBITDA to be in between $20 million to $21 million. It is also anticipating FY21 EBITDA growth to be ~50% from FY20 underlying EBITDA. The company has also announced to bring forward the payment of the interim dividend of 0.5 cents to 30 July 2020 which was earlier deferred to 29 October 2020 because of the prudent approach of the company to cash management.

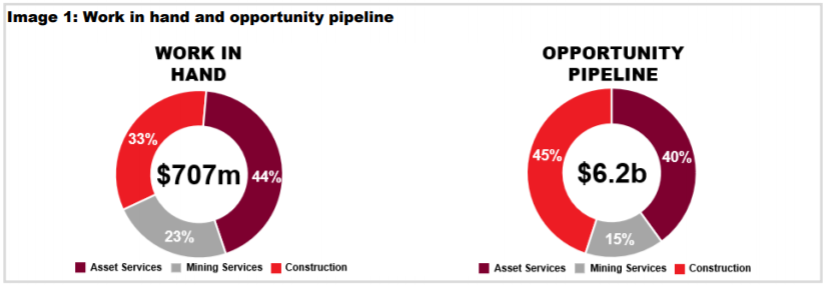

During the second half, SRG has reduced its net debt to $8 million and retains ample liquidity with available funds of $73 million. Mining Services of the company are operating in high-quality growth commodities and expect Asset Services to return to normal levels in Q1 FY21. As of 30 June 2020, the company has work in hand of $707 million with a strong pipeline of opportunities of over $6 billion. The company has a positive exposure to Government backed stimulus programs.

Work in Hand and Opportunity Pipeline (Source: Company Reports)

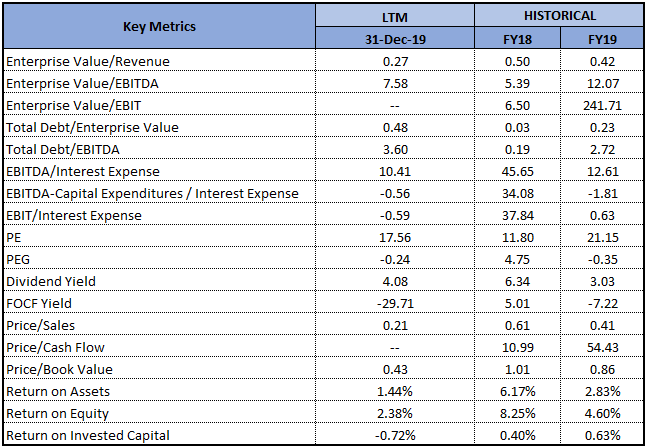

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

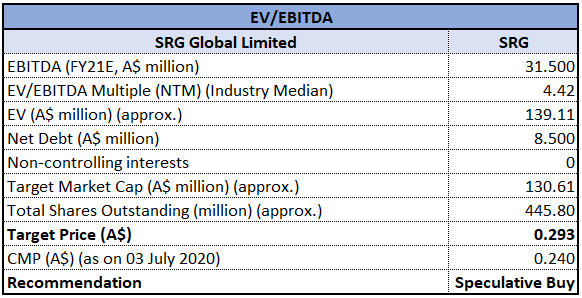

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Despite the unprecedented global market conditions because of the COVID-19 crisis, the company reported resilience in its financial position. It has significant available liquidity and diverse industries with tier one client base. The company is building a strong foundation which can deliver decent returns to shareholders. As per ASX, the stock of SRG gave a return of 25.64% in the past one month and is inclined towards its 52-weeks’ low level of $0.170, proffering a decent opportunity for the investors to enter the market. Considering the attractive trading levels, resilient financial position, decent returns in the past one month, improvement in margins and positive guidance for the coming years, we have valued the stock using the EV/EBITDA multiple based illustrative relative valuation and have arrived at an indicative target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $0.240, down by 2.041% on 03 July 2020.

.png)

SRG Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...