Company Overview: Spark New Zealand Limited (NZX: SPK) provides a range of telecommunications, information technology, media, and other digital products and services, including mobile services; voice services; broadband services; Internet television (TV); cloud, security and service management services; procurement and partner services and managed data and networks services. The Company’s subsidiaries include Computer Concepts Limited, Digital Island Limited, Gen-i Australia Pty Limited, Lightbox New Zealand, Qrious Limited, Revera Limited, Spark Finance Limited, Spark New Zealand Trading Limited, and Spark Retail Holdings Limited.

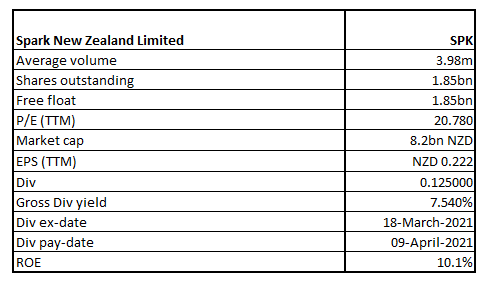

SPK Details

Spark New Zealand Limited (NZX: SPK) is a provider of digital services and telecommunications in New Zealand and operates through three segments: Spark Home, Mobile & Business; Spark Digital, and Spark Connect. The market capitalisation of the company stood at ~$8.2 billion on 22nd March 2021.

Looking at the past performance, SPK’s top-line and bottom-line over FY16-20 grew with a compounded annual growth rate (CAGR) of 0.68% and 3.65%, respectively.

Results Performance (Half-Year Ended 31 December 2020)

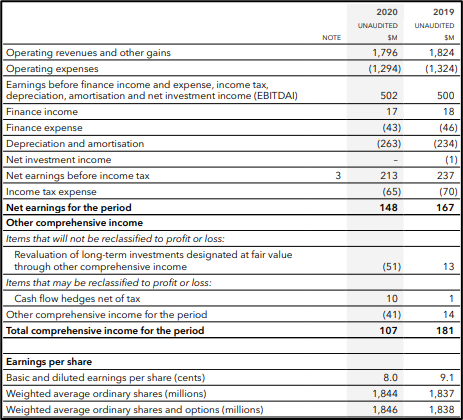

The company’s revenue from continuing operations for the interim period stood at $1,796million, a decline of 1.5% on the previous corresponding period (pcp). This decline can be attributed to the loss of higher-margin mobile roaming revenue from sustained COVID-19 border closures and higher voice revenue declines due to a non-recurring provision to refund historical wire maintenance charges.

Mobile service revenue declined by 1.2%. However, after stripping out the impact of the loss of roaming, mobile service revenue increased by 3.8% YoY. The company continued to experience growth in cloud, security, and service management revenue which grew by 4.6% to $229 million. The broadband and prepaid markets were impacted by border closures which caused fewer people to migrate to New Zealand.

EBITDAI for the period grew by 0.4% to $502 million underpinned by disciplined cost management which contributed to a decline in operating costs by 2.3%. However, net profit after tax for the period declined by 11.4% to $148 million due to increased D&A charges.

The Board of Directors announced an interim dividend of 12.5 cents per share, fully imputed, and will operate the Dividend Re-investment Plan with a 2% discount.

Exhibit 1: Income Statement

Key Data (Source: Company Reports)

Results Performance (Year Ended 30 June 2020)

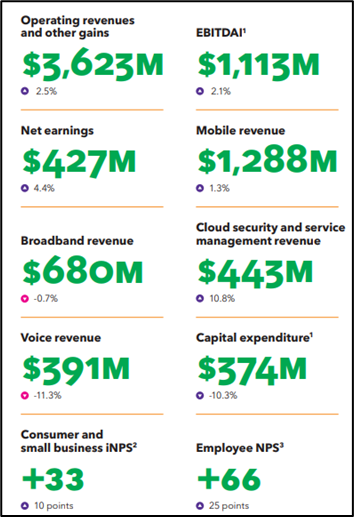

The total revenue for the full year period stood at $3,623 million, an increase by $90 million or 2.5% over the previous year on the back of 3.9% growth in mobile service revenue and 10.8% growth in cloud, security, and service management revenue. The company’s strong performance in key markets, continued focus on cost discipline and the impact of COVID-19 in the last quarter resulted in EBITDAI growth of 2.1% to $1,113 million. The growth in EBITDAI and lower tax expense contributed to net profit after tax for the period increasing by 4.4% to $427 million.

Exhibit 2: FY20 Performance Snapshot

(Source: Company Reports)

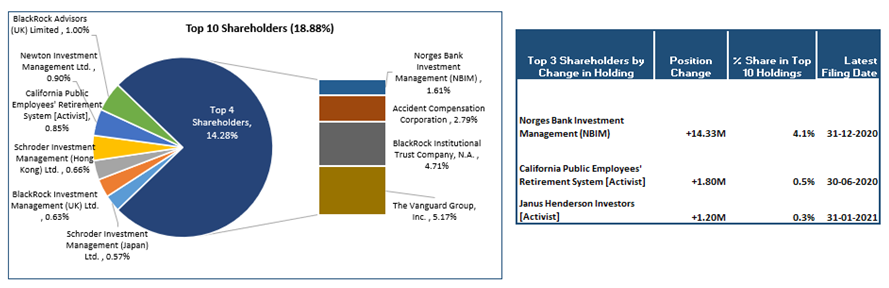

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 18.88% of the total shareholding. The Vanguard Group, Inc., and BlackRock Institutional Trust Company, N.A. holds the maximum stake in the company of 5.17% and 4.71%, respectively:

Exhibit 3: Top 10 Shareholders

Source: Refinitiv (Thomson Reuters), Analysis by Kalkine Group

A Quick Look at Key Metrics: The company’s EBITDA margin has increased from 27.4% in H1FY20 to 28.0% in H1FY21. Its ROE during H1FY21 stood at 10.1%, better than the industry median of 3.8%, implying a decent return generated for shareholders. The current ratio for H1FY21 stood at 1.17x, better than the industry median of 0.70x, implying that the company possesses better capabilities to meet its short-term obligations than its peer group.

Exhibit 4: Key Metrics

Source: Refinitiv (Thomson Reuters), Analysis by Kalkine Group

Outlook:

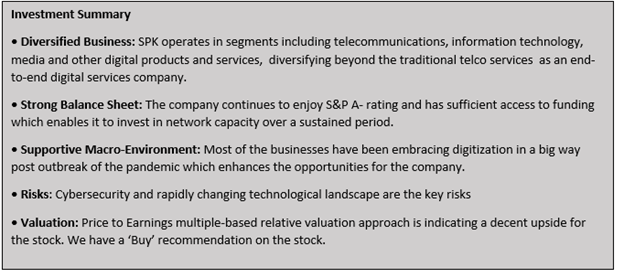

The company enjoys competitive advantages across core established markets and future growth markets. It remains focused on delivering simpler products that best suit customers’ needs. Amidst the rise in demand for business transformation and digitization following rapid adoption of work from home culture during the lockdown, the company is helping SMEs in adopting an increasingly digital marketplace.

However, the ongoing loss of mobile roaming revenues and lower growth broadband and prepaid markets which may continue to impact the revenue of the company in the short-run, has forced the company to narrow down FY21 EBITDAI guidance range to $1,100 million to $1,130 million, along with the revision in full-year dividend guidance to the top end of the range at 25 cents per share. The company’s long-term wireless ambition will help sustain the growth as there remains significant market opportunity post rolling out of 5G, and precision marketing is helping the company in identifying customers who look for best suited wireless broadband and provide them tailored offers. The company is also making steady progress in the future market with Internet of Things (IoT) connection registering a growth of 65% during the first half while its Digital Health Platform is in the development stage.

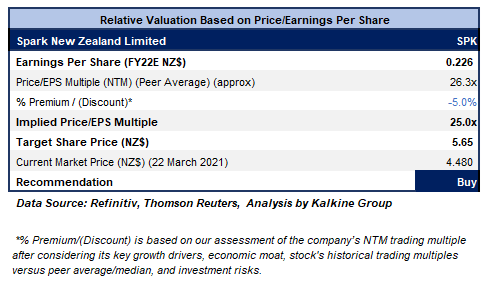

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

Stock Recommendation:

The company has 5G available in five locations across New Zealand, and has commenced live testing in Christchurch, with mobile and wireless broadband offers being launched for customers. The stock has given a return of ~6.72% and ~17.77% in nine months and one year, respectively.

Considering the aforesaid facts, we have valued the stock using Price to Earnings multiple-based valuation (on an illustrative basis) and have arrived at a target price with the potential of lower double-digit (in % terms) growth. We have applied a slight discount to the peer average price/earnings multiple (NTM) considering the company’s revised lower EBITDAI guidance for FY21, short-term impact on mobile roaming and broadband revenue, and associated risks including adoption to rapid technological changes.

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$4.480 per share, down by 2.71% on 22nd March 2021.

.png)

SPK Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...