.png)

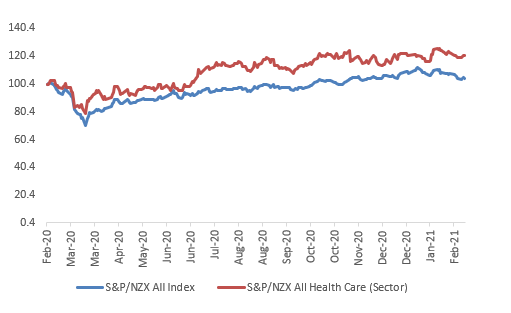

Exhibit 1: S&P/NZX All Health Care (Sector) v/s S&P/NZX All Index (One-Year Chart)*

As can be seen from the chart, S&P/NZX All Health Care (Sector) has managed to outperform S&P/NZX All Index over the time span of one year by ~16.34%

*Till February 18, 2021

Sector Landscape

New Zealand healthcare sector is one of the prominent contributors to the country’s gross domestic product (GDP) as the country spends about 10% of its GDP into healthcare which is slightly higher than the OECD average. As per the data from Statista, the New Zealand healthcare and social assistance industry witnessed a steady rise since 2014 and it accounted for a GDP of around 14.8 billion New Zealand dollars in the year ended March 2020. The healthcare system in the country is made up of both a public and private healthcare system and both indulge in offering quality care. Of which the public healthcare system is much larger as it accounts for 83% of the overall healthcare spend in the country. Overall, the country has around 220 hospitals and 20 District Health Boards managing public healthcare which are spread across the geography.

The country’s healthcare system is diverse and thus, it provides an array of job opportunities for healthcare professionals spread across every discipline or specialty. The public healthcare system offers essential healthcare services that include emergency care, essential surgery, and hospital care free of costs to not only the residents of the country but also to the people staying on a work visa valid for two years or longer. However, the cost of a private visit to the general practitioners (family doctors) is to be borne by the individuals. On the other hand, private healthcare provides services like recuperative care, elective procedures, and a range of general surgical procedures (excluding Accident and Emergency care) in private hospitals. Private healthcare also indulges in offering private radiology clinics and testing laboratories.

Key Growth Drivers

Some of the key growth drivers for the Healthcare sector have been highlighted below: -

Strong Health System

New Zealand boasts of a strong health strategy that focuses on improving the health of New Zealanders. The country’s health system also remains strong driven by the benefit from a public health system that is a free or low cost, due to heavy government subsidies. The public healthcare system in the country accounts for 83% of the overall healthcare spend in the country. The country’s healthcare system is diverse, and the public healthcare system offers essential healthcare services that includes emergency care, essential surgery, and hospital care free of costs to not only the residents of the country but also to the people staying on a work visa valid for two years or longer. New Zealand’s healthcare system offers various advantages due to its universal health system with a committed and highly trained workforce. Further, the country’s health services largely scaled towards primary care as well as wellness. Apart from this, it has a unique public health and no-fault accident compensation system, which meets the requirements of every New Zealander throughout their lifespan.

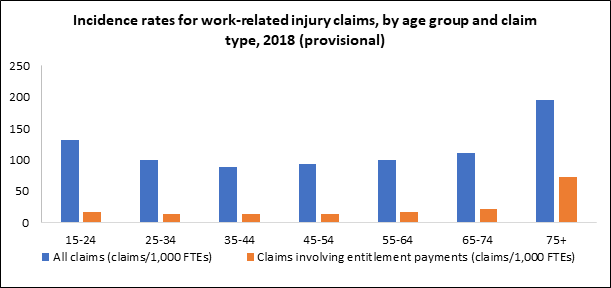

Exhibit 2: Incidence Rates for Work-Related Injury Claims

Source: Stats NZ; Chart Created by Kalkine Group

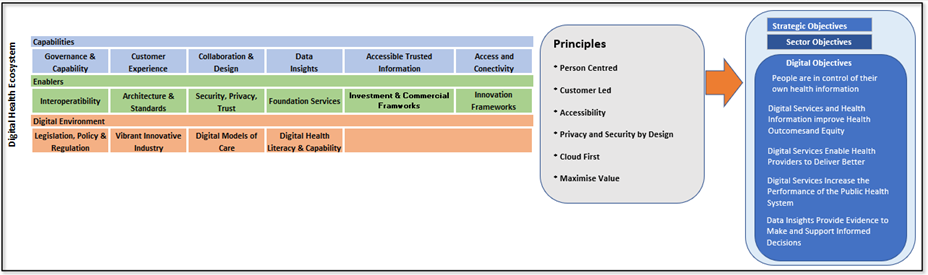

Growing Demand for Digital Health Technology

In response to changing needs and emerging technology and to support a strong and equitable public health and disability system, the government continues to pursue in leveraging the potential of technologies for healthcare. The government has developed a Digital Health Strategic Framework that emphasizes on the usage of digital technologies and data. This is aimed at providing better healthcare services, improve health outcomes and equity, boost the performance of the public health system, assist in making informed decisions through proper evidence, among others. Digital health will not only aid in enhancing the coverage of publicly funded health services but will also assist in boosting or maintaining the value of the services delivered by the healthcare service providers within available public health funding.

Exhibit 3: Strategic Framework

Source: Health Govt NZ; Chart Created by Kalkine Group

Growing Health Consciousness

The healthcare sector continued to get a major boost driven by the growing awareness towards health consciousness among the population in the country. Further, rising disposable income, as well as increase in population are also aiding in driving growth of the sector. Going forward, the improvement in economic growth prospects of the country will provide further fillip to the disposable income of New Zealanders and resultantly increased demand for better healthcare services thereby providing long-term growth visibility of the sector. Notable, this has been reflected in the improvement in New Zealand’s Real Gross National Disposable Income (RGNDI), which measures the real purchasing power of the country’s disposable income which grew 13.9% in the September 2020 quarter.

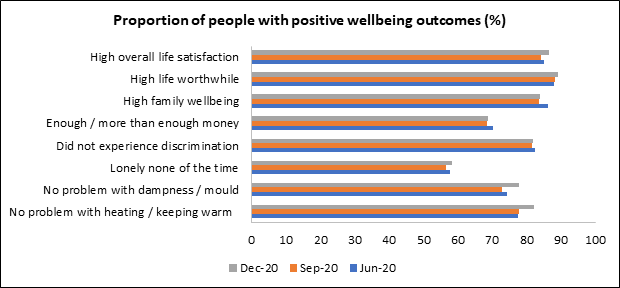

The below-mentioned chart reflects the wellbeing status of New Zealand Population.

Exhibit 4: Wellbeing Statistics

Source: Stats NZ; Chart Created by Kalkine Group

One of the growth drivers is meeting the needs of ageing population by providing services at an affordable cost as New Zealanders are living longer with aged over 65 years. The ageing population requires higher healthcare needs in order to remain healthy as they are more prone to disability or health conditions. Further, growing incidence of long-term and chronic conditions among ageing population and to deal with these conditions requires a health system which can provide affordable healthcare services which can assist the older person to stay healthy and live longer.

Source: Stats NZ; Chart Created by Kalkine Group

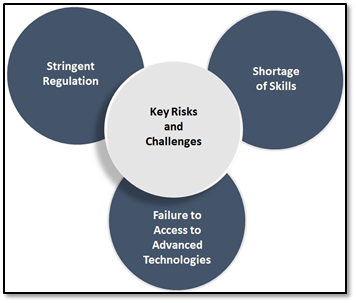

Key Risks and Challenges

Some of the risks attributable to the sector are shown below:-

Exhibit 6: Key Risks and Challenges

Outlook

New Zealand’s healthcare sector is wide-ranging and largely high-performing with a publicly funded, universal health system. The benefit of a committed and highly trained workforce also add to the strength of the sector in the global arena. Besides, the country’s health services largely scaled towards primary care as well as wellness. Unique public health and no-fault accident compensation system, which covers the whole demography through-out their lifespan also provides visibility on the sustainability of the growth momentum of the sector over the long term.

Moreover, the government’s pursuit to leverage the potential of technologies for healthcare also bodes well for the sector. The government has developed a Digital Health Strategic Framework which emphasizes on usage of digital technologies and data. This will not only aid in providing better healthcare services but also improve health outcomes. Such move will also boost the performance of the public health system and assist in making informed decisions through proper evidence, among others.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Fisher & Paykel Healthcare Corporation Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$18.6 billion, Gross Dividend Yield: 1.357%)

Business Description:

Fisher & Paykel Healthcare Corporation Limited (NZX: FPH) is engaged in designing, manufacturing and marketing of products and systems which finds usage in surgery, acute care, respiratory care, and the treatment of obstructive sleep apnea.

Outlook:

The company has commenced planning on its third manufacturing facility in Tijuana, Mexico, which is expected to be ready for occupancy in FY23. Considering the elevated hospitalisation rates for coronavirus, the company’s hospital hardware sales continued to be robust. Meanwhile, FPH recently has guided its FY21 revenue and net profit after tax to be higher than implied by the earlier assumptions. The company earlier has guided its FY21 operating revenue to be ~$1.72 billion and net profit after tax to be between $400 million to $415 million.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

.png)

We have applied EV/EBITDA multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied slight premium to EV/Revenue (Peer average) (NTM) considering the company’s trading juncture which has been at a premium and optimistic outlook.

We give a “Buy” recommendation on the stock at the current price of NZ$32.40 per share, up by 0.47% on February 18, 2021.

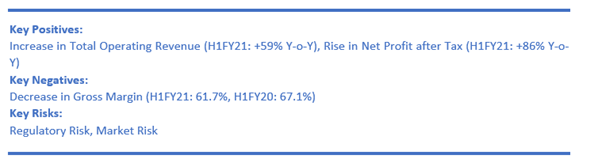

2) Rua Bioscience Ltd (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$72.937 million)

Business Description:

Based in New Zealand, Rua Bioscience Ltd (NZX: RUA) is engaged in pharmaceutical business and is targeting to be a leading producer of cannabinoid derived medicines.

Technical Overview:

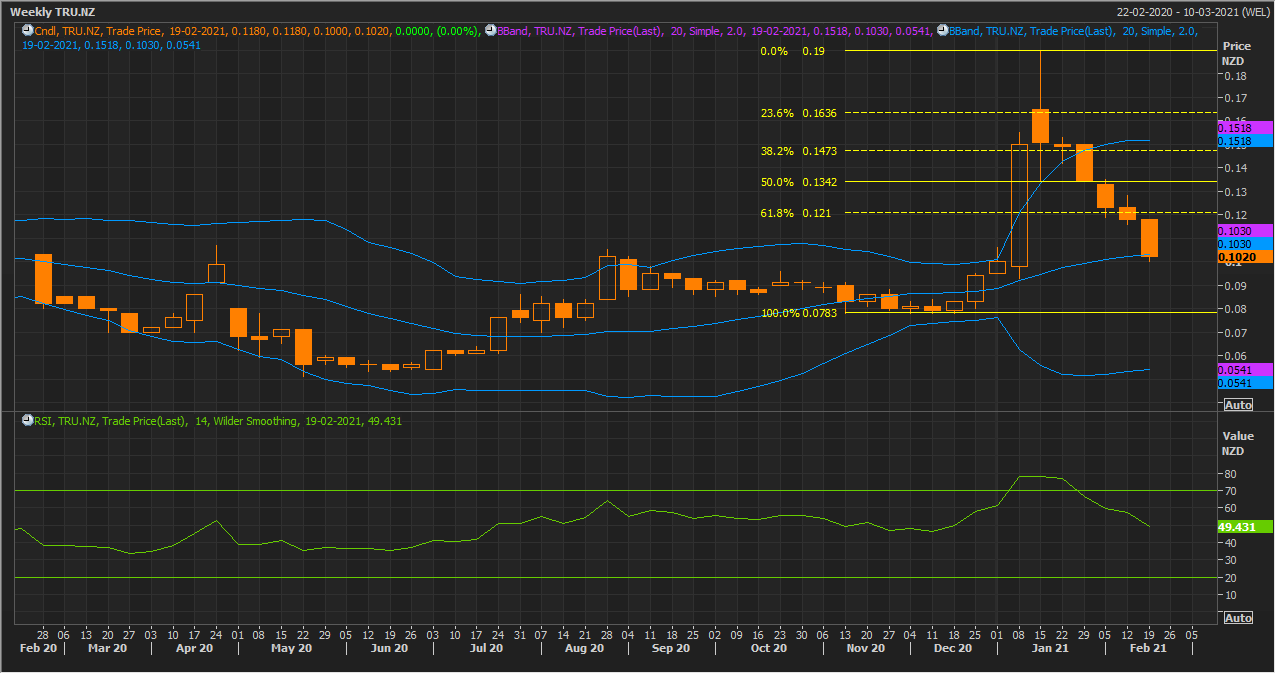

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Yellow lines are trend lines that have been drawn to find resistance and support levels for the stock.

The stock seems to have bottomed out around the $0.50 level and it is bidding to move up which gets reflected from a ‘Hammer’ formation in the previous week and in the ongoing week. The technical indicator RSI with a reading around 33 and a flattish to up curve at the end, pointing at gaining momentum while the stock being near the oversold zone.

Going forward, the stock may have resistance around $0.58 whereas support could be around $0.50.

Outlook

The company focuses on executing on its export-led strategy in order to deliver sustainable revenue. The company stated that $20 million would be utilised to finance Rua’s next stage of development, support the achievement of sustainable revenue as well as accelerate growth.

Considering the increase in other income and net assets, we give a “Speculative Buy” recommendation on the stock at the price of NZ$0.520 per share, up by 1.96% on February 18, 2021.

3) Summerset Group Holdings Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.9 billion, Gross Dividend Yield: 1.052%)

Business Description:

Summerset Group Holdings Ltd (NZX: SUM) happens to be the third largest operator as well as second largest developer of the retirement villages and aged care facilities in NZ.

Outlook

The company stated that Q4 FY 2020 reflected strongest quarter sales result in its 23-year history. The company is witnessing a decent 2021 pre-sales mainly at Summerset’s new Kenepuru (Wellington) and Te Awa (Napier) villages. SUM would open the main building at Richmond (Nelson) retirement village, providing village facilities, serviced apartments, a care centre and memory care centre in H12021.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

.png)

We have applied EV/EBITDA multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied slight premium to EV/Revenue (Peer average) (NTM) considering the company’s trading juncture which has been at a premium and the expectations that momentum witnessed in Q4 FY 2020 might continue.

We give a “Hold” recommendation on the stock at the current price of NZ$12.92 per share, down by 0.77% on February 18, 2021.

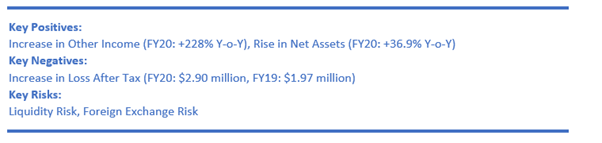

4) TruScreen Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$37.012 million)

TruScreen Limited (NZX: TRU) offers the latest technology in cervical screening, providing real-time, accurate detection of pre-cancerous as well as cancerous cervical cells to help improve the health and wellbeing of the women.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Blue colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has given a weaker close for the ongoing week at $0.10 with strong support is seen at $0.078. The technical indicator RSI with a reading around 49 and a curve at the end pointing down, suggests a weakening of bullish momentum for the stock.

Going forward, the stock may have resistance around the 61.8% retracement level of $0.121 whereas support could be around $0.078.

Outlook

The company’s goals for FY 2021 and beyond primarily revolves around achieving >160 commercially installed devices throughout key markets by March 2021 (+100% on 2020), increase the commercial coverage in Russia, following the coronavirus recovery and expand market presence in the Eastern Europe. The goals also include reducing cost of production of both TruScreen device as well as SUS via research and development and process optimisation.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...