Company Overview: New Zealand-based tourism, leisure, and entertainment company, SkyCity Entertainment Group Limited (NZX: SKC) operates entertainment complexes in Auckland, Hamilton and Queenstown, New Zealand, and Adelaide, Australia. The company’s segments include SKYCITY Adelaide, SKYCITY Auckland, Rest of New Zealand, and International Business. SKYCITY Adelaide includes food and beverage along with casino operations. The rest of New Zealand comprises SKYCITY Queenstown, SKYCITY Hamilton, and SKYCITY Wharf and Associates.

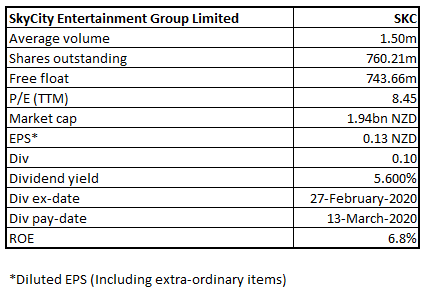

SKC Details

Investment Summary:

Tourism & Entertainment Industry Recovering Gradually: SkyCity Entertainment Group Limited (NZX: SKC) is New Zealand’s leading leisure, tourism, and entertainment company with iconic status. It is listed in both New Zealand (NZX) and Australia (ASX) stock exchanges. It has a market capitalization of ~$1.94 billion as on August 31, 2020.

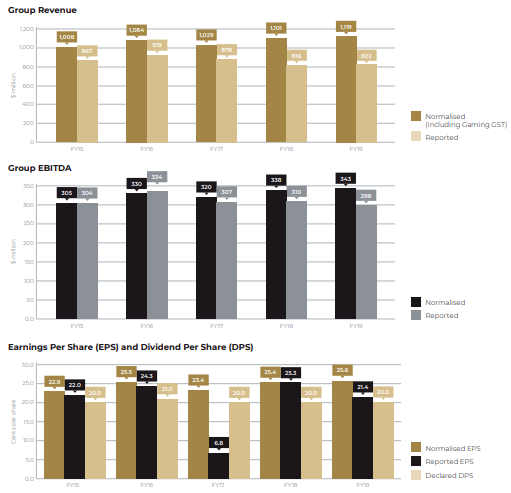

Looking at the past performance over FY15 to FY19, the bottom line of the company grew at a compounded annual growth rate (CAGR) of 2.95%. The net income of the company improved from $128.7 million in FY15 to $144.6 million in FY19.

In the first half FY20, the performance of the group was robust where it reported high double-digit growth in its revenue and triple-digit growth in its EBITDA. Under the New Zealand Properties segment, in Auckland, gaming revenue (pre-NZICC fire) was up by around 6% for the period to 21 October. Due to improved gaming activity, particularly in EGMs and good cost control offset by weaker non-gaming performance, EBITDA was up by around 4% on a like-for-like basis. In Hamilton, the company witnessed record EBITDA over strong local gaming activity along with stable F&B contribution. In Queenstown, due to increased visitation from key customers, increased win rates and margin improvements, EBITDA improved strongly in the period.

Under the Australian properties segment, in Adelaide, considering construction disruption and stronger pcp, EBITDA performance was satisfactory.

The international businesses passed through a rough patch as turnover declined by 40% to $4.6bn vs record pcp, due to fewer visits from key customers and softer regional market conditions. The normalised EBITDA, declined by 67%, where margin impacted by higher commissions/comps as % of turnover, increased investment in sales function and negative operating leverage.

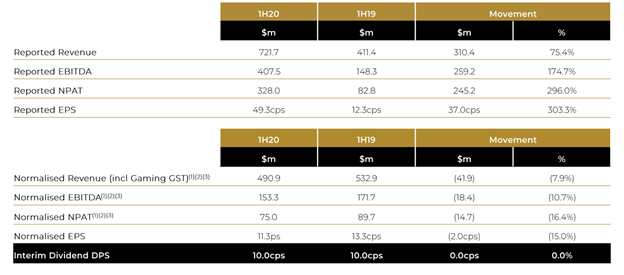

H1FY20 Income Statement (Source: Company Reports)

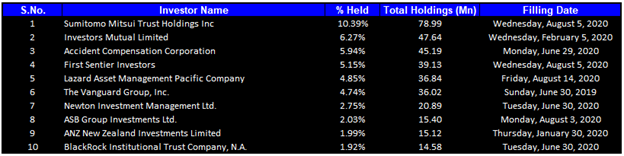

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 46.01% of the total shareholding. Sumitomo Mitsui Trust Holdings Inc and Investors Mutual Limited are holding a maximum stake in the company at 10.39% and 6.27%, respectively, as provided in the table below:

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

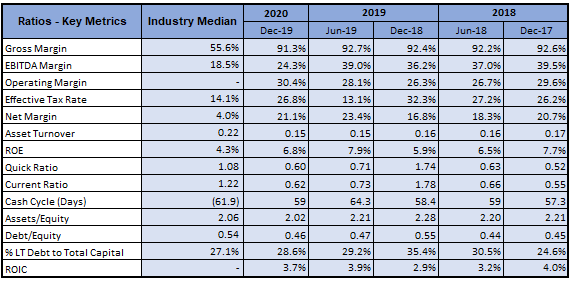

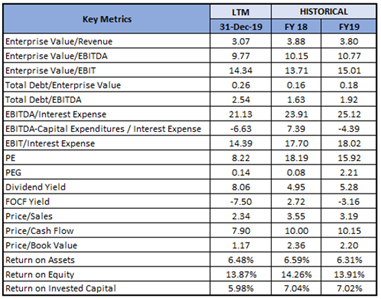

A Quick Look at Key Metrics: Its gross margin, EBITDA margin and net margin for H1FY20 stood at 91.3%, 24.3% and 21.1%, better than the industry median of 55.6%, 18.5% and 4.0%, respectively, implying greater efficiency of the management in managing operating as well as non-operating costs than the peers. Its Debt to Equity ratio for H1FY20 stood at 0.46x, lower than the industry median of 0.54x, depicting a reasonable leverage position of the company.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Staggering H1FY20 Financial Performance: For the six months ended 31st December 2019, the company’s reported revenue stood at $721.7 million, up by 75.4% and reported EBITDA stood at $407.5 million, up by 174.7%. The key driver of the company’s 1HFY20 result was a positive performance from domestic NZ businesses on a like-for-like basis. It was offset by significantly weaker IB activity and higher ICT costs. However, normalised revenue stood at $490.9 million, down by 7.9% and normalised EBITDA stood at $153.3 million, down by 10.7%. The domestic businesses represented 95% of 1HFY20 normalised EBITDA.

Due to increased investment in ICT, corporate costs surged by +13.6% as compared to the previous corresponding period. As the company was not able to capitalise interest on NZICC/Horizon Hotel project from the date of fire, net interest expense is in-line with pcp, which is higher than expected. The Board of Directors declared a fully imputed interim dividend of 10 cps, in-line with existing policy.

Historical Performance (Source: Company Reports)

FY19 Financial Performance: The company reported decline in net profit after tax (NPAT) and EBITDA in FY19 (ended June 30, 2019) by 14.7% and 3.9%, respectively, mainly due to a lower win rate in International Business and other significant items. Despite a more challenging operating environment, normalized EBITDA and NPAT, improved by 1.3% and 1.9%, respectively, on the back of strong growth in International Business (IB) turnover and Auckland EGMs, stable performances from Adelaide and Hamilton, and impact of asset sale programme.

Company Outlook: The company closed its Adelaide Casino as per the guidelines of the Australian Government under the lockdown period. Now, with the improvement in situation, there has been gradual lifting of restrictions that are likely to benefit the company. The closure requirements do not apply to construction sites, and therefore, it will continue work on its Adelaide expansion project. Because of the closure of Adelaide Casino and the uncertainty as to the duration of the closure, the company has withdrawn its earnings guidance for FY20.

Key Risks: The general economic conditions in the markets that the company operates in and volatility in certain parts of the business, can significantly influence the financial performance of the company.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

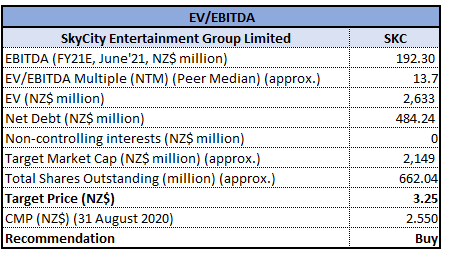

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

Demonstrating strong positive sentiment, the stock on the first trading session of the on-going week has given close at $2.55 which is above 20 period SMA of $2.52. Technical indicator RSI with around 47 reading and curve at the end pointing up, suggests gaining of strong bullish momentum.

Going forward, the stock may have resistance around 61.8% retracement level of $3.00 while support could be around 38.2% retracement level of $2.30.

Stock Recommendation: The company has diverse business divisions in the entertainment & tourism industry. It has reported a satisfactory NPAT growth from FY15-19. The company has delivered outstanding growth in H1FY20 over the previous corresponding period despite breaking out of the fire at NZICC. Even though the pandemic-led lockdown period has materially impacted the SKC’s operations, the improving conditions across the region along with economic recovery is expected to play a crucial role in the resurrection of the entertainment & tourism industry. The restriction period also witnessed growth in online entertainment modes such as gaming and poker which is further expected to surge in the coming period.

Considering the aforesaid facts, recent update and H1FY20 results, we have valued the stock using EV/EBITDA multiple based Relative Valuation (on an illustrative basis) and have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$2.55 per share, up by 2.82% on August 31, 2020.

.png)

SKC Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...