Company Overview: Seeka Ltd, formerly Seeka Kiwifruit Industries Limited (Seeka) is a New Zealand-based integrated orcharding, post harvest, supply and retail services company. The Company operates through five segments: Orchard operations, Post harvest operations, Retail service operations, All other segments - New Zealand and Australian operations. The Orchard operations segment provides on-orchard management services to orchard owners producing kiwifruit, avocado and kiwiberry crops. The Post harvest operations segment provides post harvest services to the kiwifruit, avocado and kiwiberry industries. The Retail service operations segment provides fruit marketing services in New Zealand and internationally, particularly in the Australian and Asian markets. The Australian operations segment owns and operates Australian orchards; provides post harvest operations, and markets the produce from those orchards, primarily in Australia. In New Zealand, the Company also provides retail and ripening services.

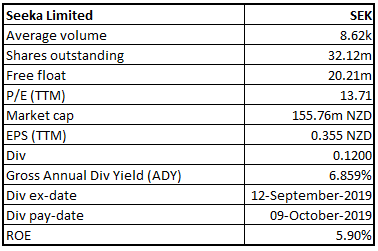

SEK Details

Growth Driven by Acquisitions: Seeka Limited (NZX: SEK) operates as a produce company in New Zealand and Australia. The Company produces papaya, kiwiberries, pineapples, apricots, cherries, etc. In New Zealand, the company extends orcharding, post-harvest and retail services to the kiwifruit, avocado, citrus, berry, and kiwiberry industries. The company is engaged in the manufacturing of Kiwi Crush and Kiwi Crushies ranges along with avocado oil. In addition, it also provides retail and ripening services for imported tropical produce and operates a wholesale market. In Australia, the company operates orchards and associated post-harvest assets. During the six months ended 30 June 2019, the company reported a decent financial performance through continued focus on its growth strategy. Key strategic initiatives during the year consisted of consolidation of the Northland orcharding and post-harvest operations & additional kiwifruit volume and processing facility through the purchase of Aongatete Coolstores Limited. Profit after tax for the six months period went up by 28% and EBITDA reported a growth of 8.5%.

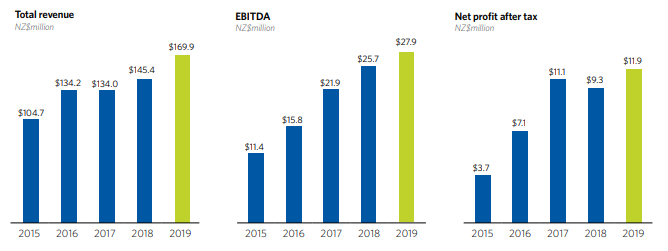

Over the period covering 2015 to 2018, the company has reported a top-line CAGR of 3.3%, with the highest growth reported in FY16 at 24.2%. FY15 and FY18 revenue amounted to $184.74 million and $203.71 million, respectively. The bottom-line CAGR over the said period was reported at 20.2%, with FY15 and FY18 profit amounting to $4.27 million and $7.42 million, respectively. The highest growth in profit was again reported in FY16, at 143.3%. Looking at the interim performance, the company has a track record of continuous increase in revenue, except for the period ended 30 June 2017 that reported a marginal decline of $0.2 million on pcp. Value of interim EBITDA, starting from 30 June 2015 to 30 June 2019, has witnessed a continuous upward movement, as depicted in the figure below. In 1H2015 and 1H2019, the company reported EBITDA of $11.4 million and $27.9 million, respectively.

As a forward statement, the company stated that it is looking to raise more finance from the sale of remaining Northland orchards that will be utilised to repay debt. As per the EBITDA guidance provided for full year 2019, the company is expecting to report single-digit growth over the prior corresponding period.

Key Financial Metrics (Source: Company Reports)

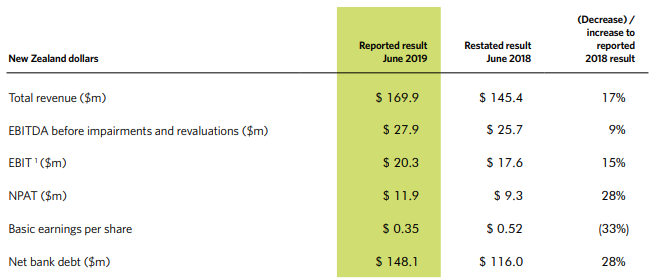

Half Yearly Highlights: During the six months ended 30 June 2019, the company generated total revenue amounting to $169.9 million, up 17% on prior corresponding period revenue of $145.4 million. EBITDA before impairments and revaluations stood at $27.9 million, up 9% on prior corresponding period EBITDA of $25.7 million. Net profit after tax amounted to $11.9 million, representing an increase of $9.3 million on pcp. Net debt for the period increased by 28% to $148.1 million, reflecting investment in post-harvest capacity and acquisition of Aongatete. On 9 October 2019, the company paid a fully imputed dividend of $0.12 per share.

1HFY19 Financial Highlights (Source: Company Reports)

Strategic Initiatives: In 2018, the company completed the acquisition of Northland kiwifruit orchards and related post-harvest business from T&G Global Limited & is making good progress towards the sale of orchards to deliver a new level of service to this growing region and securing ongoing supply to the post-harvest operations. In addition, the company expanded its kiwifruit operations with the acquisition of Aongatete in March 2019. The purchase was made for a total consideration of $14 million.

Business Highlights: In New Zealand, the company’s Orchard operations reported an increase of $9.34 million in revenue. EBITDA from orcharding was in line with pcp due to a reduction in the productive orchard area under long term lease. Post-harvest revenue in New Zealand increased by 19% while costs went up due to higher wage rates and the ongoing focus on health and safety. In Australia, the company operates through a wholly owned entity named, Seeka Australia PTY Limited, that reported an EBITDA loss of $0.15 million as a result of lower yields and an under-performing green nashi programme.

Going forward, the company is aiming to bring debt to more conservative levels through the sale of Northland orchards. In New Zealand, the company will continue to invest in long term lease arrangements. Fruit volumes in the region are set to increase as the orchards reach maturity. The Australia operations are expected to provide extended geographical reach to the company. To develop the business, the company will resort to measures such as upgrading existing and developing new orchards and investing in water to grow production.

Recent Updates:

(1) Change in Directors’ Interest - Fred Allan Hutchings acquired 971 ordinary shares in the company for a consideration of $4.7671 per share. John Garland Burke acquired 2,022 ordinary shares for a per share consideration of $4.7671. Michael Gilbert Franks and Stuart Thomas McKinstry acquired 3,011 and 15 ordinary shares, respectively.

(2) Dividend Reinvestment Plan - The company recently updated that it will be issuing a total of 93,431 shares for a consideration of $4.7671 per share, for the purpose of raising cash through its Dividend Reinvestment Plan for the dividend paid on 9 October 2019. The issue price of the shares was calculated on the basis of volume weighted average sale price for all SEK shares sold on the NZX over the period 12 September 2019 to 2 October 2019, less a 2.0% discount. Shareholders who opted to participate in the Dividend Reinvestment Plan were offered shares in place of cash in respect to dividend payable on 9 October 2019.

(3) Update on Northland Orchards – The company recently released an announcement, providing the status on the sale of Northland orchards acquired through the purchase of Turners and Growers Horticulture Limited’s KeriKeri based post-harvest and orchard business. Under the deal, the company acquired a portfolio of Northland orchards for the purpose of rejuvenation and subsequent sale. The strategy underlying the above transaction has been to repay the company’s debt via proceeds from sale of the orchards. Since 2018, there has been a series of sales transactions, all of which resulted in a gain to the company. During the year ended 31 December 2018, the company settled $7.0 million out of the portfolio, that resulted in a gain amounting to $0.6 million. Till date, 2019 has seen two tranches of sale. During the six months ended 30 June 2019, the company sold $5.4 million of the portfolio, gaining $1.2 million. The second tranche included a sale of $28.75 million, releasing a gain of $1.79 million. This included a sale of $15.5 million to Booster’s PLPP. As per the announcement, the property sold to PLPP was leased back to Seeka, with the accounting treatment subject to IFRS16. In addition to the above, the company has also agreed to $5.05 million in conditional sales that are expected to be settled before 31 December 2019 and will result in a gain on sale of $1.5 million upon completion. Post settlement of the above transactions, the company holds orchards worth $9.54 million and is under constant dialogue for sale negotiations.

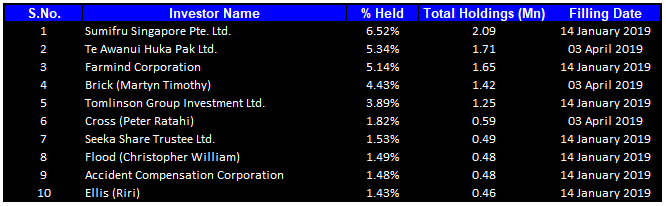

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 33.07% of the total shareholding. Sumifru Singapore Pte. Ltd is the entity holding maximum shares in the company at 6.52. Te Awanui Huka Pak Ltd. is the second largest shareholder, representing a holding of 5.34% in the company.

Top Ten Shareholders (Source: Thomson Reuters)

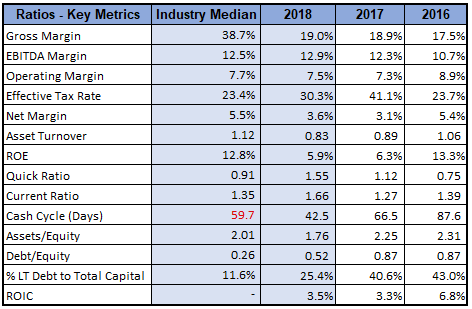

Key Metrics: During the year ended 31 December 2018, the company reported a marginal increase in gross margin on pcp. Gross margin for 2017 and 2018 stood at 18.9% and 19.0%, respectively. EBITDA margin for the year stood higher than the industry median as well the margin in pcp. Net margin for the period also increased to 3.6% in 2018, as compared to 3.1% in 2017. In 2018, the company had a current ratio of 1.66x, which was higher than the industry median of 1.35x, reflecting a better position to meet short-term obligations of the business.

Key Metrics (Source: Thomson Reuters)

What to Expect: EBITDA for the full year ending 31 December 2019 is expected to be in the range of $32.5 million - $33.5 million. The above range will result in EBITDA growth in the range of 5% - 8% over FY18 full year restated EBITDA of $31.0 million. As a result of lower volumes of fruit in store and an early selling season, the company is anticipating lower operational earnings in the second half of the financial year.

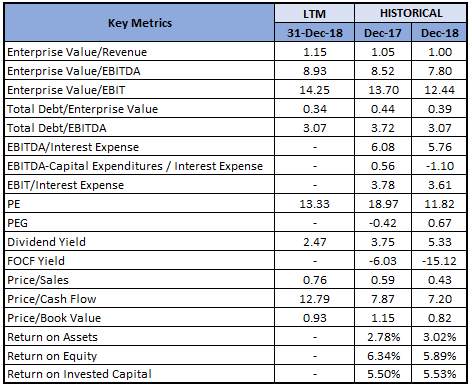

Key Valuation Metrics (Source: Thomson Reuters)

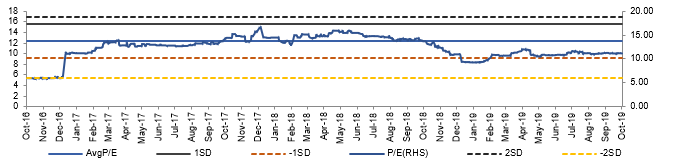

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: In H12019, the company reported decent growth across key metrics including revenue, EBITDA and net profit, supported by continuous progress towards the growth strategy. The period was marked by successful acquisitions of Northland orchards and Aongatete, to normalise debt levels and expand its kiwifruit operations. In 2018, the company had a debt-equity ratio of 0.52x as compared to 0.87x in 2017. This ratio is expected to reduce further in 2019 as the company repays its debt through proceeds from the sale of Northland orchards. Furthermore, the company is also eyeing investments in long term lease arrangements in New Zealand, along with further development in the Australian operations to expand its geographical footprints. Given the backdrop of aforesaid parameters, we have valued the stock using PE market multiple and have arrived at an upside of lower double-digit growth ascribing a valuation of three-year average PE multiple of 12.47x to FY19E EPS. Hence, we give a “Buy” recommendation on the stock at the current market price of $4.85 per share.

SEK Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...