Company Overview: Seeka Limited (NZX: SEK) happens to be an international business which is based in New Zealand and is focused towards orchard-to-market excellence. The company’s core business is kiwifruit and it is the key supplier of New Zealand fruit to the global kiwifruit trade, via marketer Zespri. Since the company is being directly involved in every step of the supply chain, its market partners get a secure supply of the high-quality products. From the Australian orchards, the company is the country’s largest producer of Hayward kiwifruit and Nashi peers and also produce a range of European pears, apricots, cherries and plums.

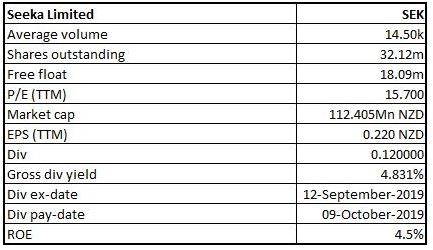

SEK Details

Investment Summary:

Cash Flow from Operations Rose 14% YoY: Seeka Limited (NZX: SEK) is an integrated horticulture and production company that is in the business of growing, processing, distributing and marketing high-quality products to the world markets. The market capitalisation of the company stood at around $112.405 million as on 30th March 2020.

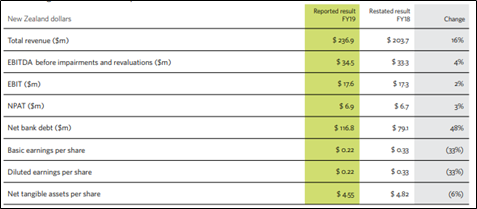

For the full year ended 31st December 2019, the company reported total revenue of $236.9 million, up by 16%. Consolidated earnings before interest, tax, depreciation and amortisation (EBITDA) stood at $34.5 million, up 4% ahead of the guidance range of between $32.5 million to $33.5 million. This includes an $0.63 million EBITDA loss from Seeka Australia as a very dry summer lowered Hayward kiwifruit volume, plus an underperforming nashi programme. Consolidated profit after tax stood at $6.88 million, up by 3% from FY18. Cash flow from operations came at $18.59, up 14% over pcp.

Operating Performance (Source: Company Reports)

The company’s Board has declared a dividend amounting to $0.12 per share. It consisted of normal dividend of $0.08 per share and the special dividend of $0.04 cents per share following completion of the property sales negotiated in 2019 and completed in 2020. Moreover, the dividend is fully imputed and it would be paid on April 17, 2020.

The company is optimistic about Australian investment and Australian orchard portfolio, and there are expectations that the proposed strategy to sell as well as leaseback the kiwifruit orchards would be realising a gain that will be utilized to repay the debt.

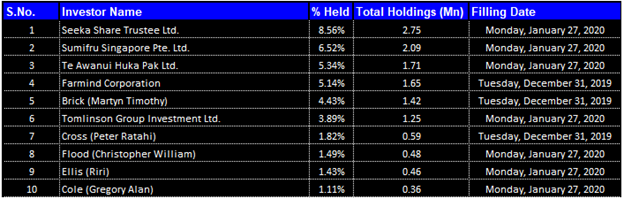

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 39.72% of the total shareholding. Seeka Share Trustee Ltd. and Sumifru Singapore Pte. Ltd. are holding maximum interests in the company at 8.56% and 6.52%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

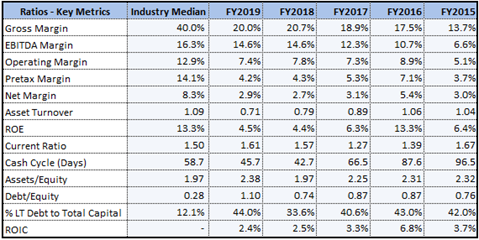

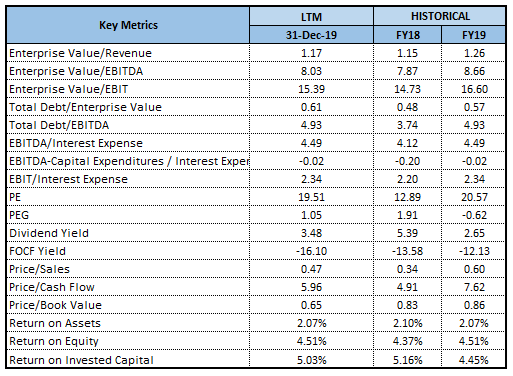

Brief Overview of Key Metrics: The company’s ROE improved marginally from 4.4% in FY18 to 4.5% in FY19. This implies that the company delivered better returns for its shareholders than the previous year. The increase in ROE is the result of an increase in NPAT by 3%. Net margins in FY19 also increased marginally from 2.7% in FY18 to 2.9% and, therefore, it could be said the company has improved its capabilities to convert its top line into bottom line.

Its current ratio in FY 2019 stood at 1.61x which is higher than the industry median figure of 1.50x and, thus, it looks like SEK could meet its short-term obligations. Moreover, decent levels of liquidity could help the company in making deployments towards strategic growth prospects.

Key Metrics (Source: Thomson Reuters)

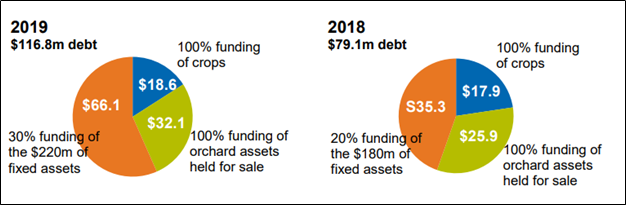

Financial Position at the Year End: Net debt at 31st December 2019, stood at $116.79 million compared to $79.01 million at year-end FY18 and $148.08 million at 30 June 2019. During the year, the company realised $44.53 million in assets held for sale of which $34.55 million is related to its Northland orchards. These Northland sales delivered $3.19 million in gains along with a secure supply commitment. Besides, at year-end, the company had conditionally sold a further $10.1 million in Northland properties; these sales settled on 24th February 2020.

In FY19, the company invested $34.67 million in property plant and equipment, primarily building the Kerikeri packhouse and commissioning a new packing machine and upgrading Oakside packing machine 2, pre-coolers and cool stores. Once additional pre-cooler and cool store builds at Kerikeri are completed, the company’s post-harvest capacity is forecast to be able to handle fruit supply for the next two seasons. Its focus is on improving supply chain efficiency and seeking innovative solutions to curtail further investments.

Net bank debt funding of business operations (Source: Company Reports)

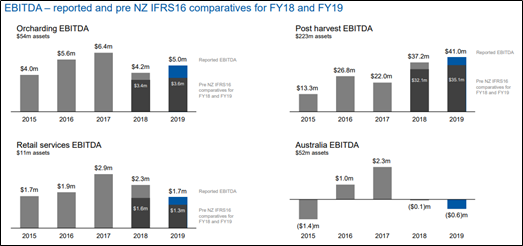

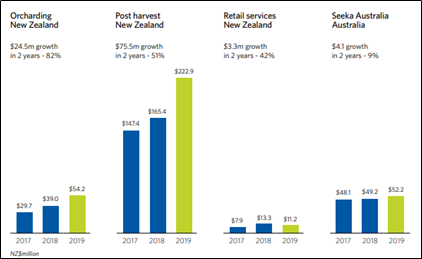

Operating Segment Overview: The orchard operations revenue stood at $72.42 million, up by 37% over $52.83 million in FY18, while EBITDA stood at $4.99 million as compared to $4.21 million in FY18. The moderate increase in EBITDA reflects the profit share mechanisms in favour of the orchard owners, alongside the primary risk. Orcharding kiwifruit volumes increased from new products associated with the Northland and Aongatete acquisitions, with the company growing 41.11 million kilograms of kiwifruit (11.42 million trays) compared to the previous year’s 37.44 million kilograms (10.68 million trays).

Post-harvest segment revenue stood at $140.11 million as compared to $123.81 million in FY18. Driven by higher wages, inflation and the ongoing focus on health and safety, post-harvest costs are up across the industry. EBITDA stood at $40.98 million as compared to $37.16 million in FY18.

New Zealand retail services operations reported EBITDA of $1.67 million down from FY18's $2.34 million due to a reduced kiwiberry harvest, lower avocado volumes from biennial bearing and higher supply chain costs.

Australian operations reported an EBITDA loss of $0.63 million as compared to $0.06 million loss in FY18 due to lower yields and an under-performing green nashi programme.

Trends in operating segment performance (Source: Company Reports)

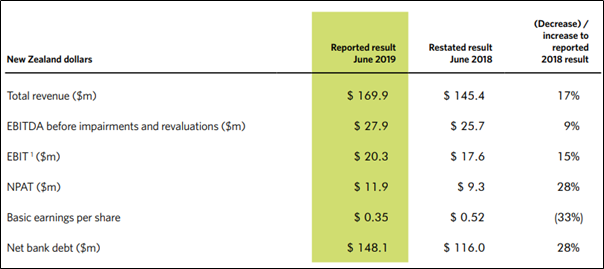

Strong Growth in Revenues: For the six months ended 30th June 2019, the company reported revenue of $169.87 million, up 16.8% on pcp. Consolidated EBITDA stood at $27.91 million, up 8.6%, which includes $0.15 million EBITDA loss from Seeka Australia, from a very dry summer resulting in lower Hayward kiwifruit volumes and an underperforming nashi programme. The company reported a consolidated profit after tax of $11.86 million, up 27.3% on pcp, with cash flow from operations up 107% to $5.15 million. The company’s net debt at 30th June stood at $148.08 million, an increase of $32.1 million, driven by the investment in post-harvest capacity and the Aongatete acquisition.

Operational Performance (Source: Company Reports)

SEK Completes Sale of Northland Orchard to PLPP: The company has entered into an agreement to sell a 20-canopy hectare Kerikeri SunGold kiwifruit orchard to Booster’s listed Private Land & Property Portfolio (or PLPP). The orchard is leased back by the Seeka for a fixed rate, and under the lease, it will also manage the orchard. The proceeds from the sale would be used to pay off debt and to finance the continuing infrastructure development project at the company’s Waipapa Road Post-Harvest facility.

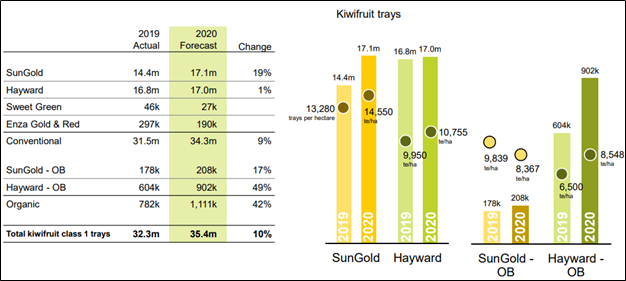

Crop Estimate for FY20: The company is forecasting 35.4 million trays for FY20, up by 10% on FY19. The biggest contributor to this increase will be from Hayward-OB, up by 49% to 902k trays. SunGold is expected to increase by 19% to 17.1 million trays.

2020 Crop Forecast (Source: Company Reports)

Operating Asset Growth Through Investments and Acquisitions: The company’s core kiwifruit industry is going through a rapid growth phase, driven by the global demand for SunGold kiwifruit. Its strategic growth plan includes investing in orcharding services so landowners can produce high-value crops, and post-harvest capacity to manage ongoing volume growth. It has also extended its geographical reach with the 2018 Northland acquisition and subsequent site build, and the 2019 acquisition of Aongatete in kiwifruit heartland. These investments have secured new capacity and are delivering world-class service to its new client growers. The company’s investments in post-harvest capacity are forecast to handle the growth in crop volumes through to 2021.

Total operating asset value by segment (Source: Company Reports)

SEK Categorized as An Essential Business: The company has been classified as an essential business for its fruit production, processing and wholesale market operations and is registering under the Ministry of Primary Industries scheme. It is adhering to the proper and stringent distancing and hygiene protocols put in place by the Government to contain Covid-19 and required to keep its people safe. It is also continuing the harvest of fruit in New Zealand and Australia.

Outlook for FY20: The company is expecting improved earnings in FY20 depending on New Zealand and Australian crop volumes. The company has an increasing volume of Zespri SunGold with both new growers and new developments, along with a significantly improved SeekaFresh business and increasing avocado volumes.

The company continues to consolidate the acquired businesses and complete Northland orchard sales and is investigating the potential sale and leaseback of the Group’s Australian kiwifruit orchards. Seeka is anticipating earnings growth, noting market uncertainty from the current coronavirus outbreak. The company will provide current year earnings guidance at half-year (once the harvest is completed).

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

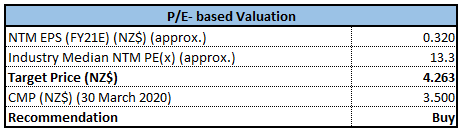

P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months.

Technical Overview:

Weekly Chart –

Source: Thomson Reuters

Daily Chart -

Source: Thomson Reuters

Note: Purple colour lines are Bollinger bands, yellow lines are retracement lines and orange colour dotted lines are Parabolic SAR.

As is obvious from both the timeframe of chart patterns that the stock has been on a falling streak and it has reached in highly oversold zone. In the today’s trading session, the stock has closed with full body bullish candle on both the timeframe of charts thereby indicating at potential reversal in price direction.

The performance of technical indicators though, confirms to weakening of momentum, the highly oversold status for the stock suggest likely rebound in the stock price to take place.

Thus, we believe that the stock has bottomed out and is going to experience technical rebound. We also believe that the current low of $3.40 which will act as support while on retracing up, it will have resistance around $4.34 which happens to be 50% retracement level.

Stock Recommendation: The company’s gross profit has witnessed a CAGR of 24.9% between FY 2015- FY 2019 and, during the same time frame, its net income has witnessed a CAGR of 12.55%. Notably, its total revenues have witnessed a CAGR of 13.6% between FY 2015- FY 2019 and, therefore, it can be said that SEK is possessing decent capabilities to garner the revenues which could help it in further strengthening its financial footing. The stock price of the company is trading closer to its 52-week lower price and, therefore, it can be said that the current trading juncture is offering decent opportunities for accumulation.

On the valuation front, we have valued the stock using Price to Earnings multiple based relative valuation method and have arrived at a target price of lower double-digit upside (in % terms).

Considering the CAGR in top line, expected upside and current trading levels, we give a “Buy” rating on the stock at the current market price of NZ$3.500 per share, up by 1.45% on March 30, 2020.

SEK Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...