Company Overview: Seeka Ltd, formerly Seeka Kiwifruit Industries Limited (Seeka) is a New Zealand-based integrated orcharding, post harvest, supply and retail services company. The Company operates through five segments: Orchard operations, Post harvest operations, Retail service operations, All other segments - New Zealand and Australian operations. The Orchard operations segment provides on-orchard management services to orchard owners producing kiwifruit, avocado and kiwiberry crops. The Post harvest operations segment provides post harvest services to the kiwifruit, avocado and kiwiberry industries. The Retail service operations segment provides fruit marketing services in New Zealand and internationally, particularly in the Australian and Asian markets. The Australian operations segment owns and operates Australian orchards; provides post harvest operations, and markets the produce from those orchards, primarily in Australia. In New Zealand, the Company also provides retail and ripening services.

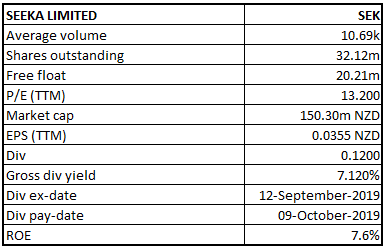

SEK Details

Striving for Excellence in Agri and Allied Business: Seeka Limited (NZX: SEK) started its operation in the year 1980 in the small rural township of Te Puke. From there, it has today evolved to become the largest producer of kiwifruit in New Zealand and Australia, and a major provider of supply chain services which delivers the very best produce to an ever-growing range of global consumers.

The company is determined on consolidating its position in the market, setting its management structures and selling orchards with winning supply contracts along with attaining operational excellence and reducing debt. During the half year period for FY19, the company has extended its core business through the Aongatete acquisition, and secured Northland post-harvest volumes while negotiating $24.11 Mn of orchard sales, and it is progressing on the sale of the remaining Northland orchards currently held at the fair value of $21.65 Mn.

SEK is marketing its Australian kiwifruit orchard portfolio, as market conditions for Australian-grown produce are good, and the fruit is of excellent quality. Production for Kiwifruit in Australia is expected to get double in the next five years, underpinned by planned sale and leaseback of three kiwifruit orchards.

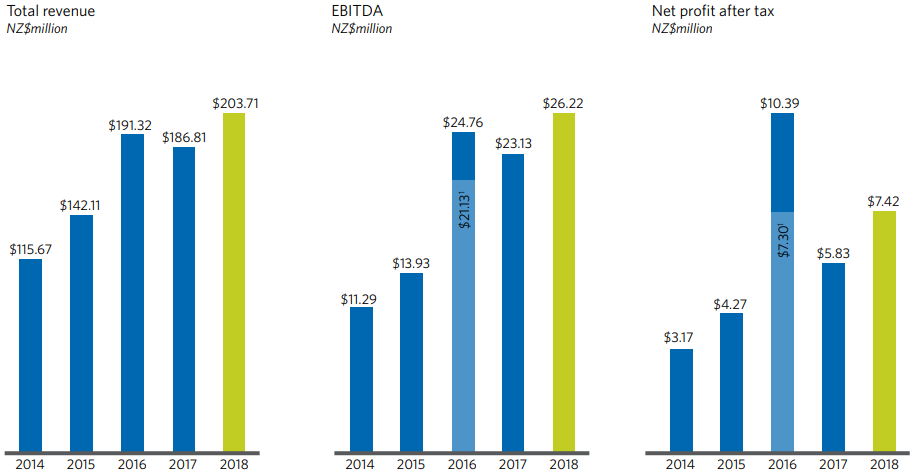

Seeka Limited has anticipated its 2019 full year EBITDA to be in the range of $32.5 Mn to $33.5 Mn, better than FY18 result, and with reduced debt. Looking at historical performance for the period FY14-18. Total revenue, EBITDA, and net profit have grown at a CAGR of 15.19%, 23.44%, and 23.69%, respectively.

SEK’s Past Yearly Performance (Source: Company Reports)

H1FY19 Key Highlights for the period ended June 30, 2019: Revenue for the period increased by 16.8% to $169.87 Mn, as compared to $145.44 Mn in the previous corresponding period. Consolidated earnings before interest, tax, depreciation and amortisation (EBITDA) was reported at $27.91 Mn, an increase of 8.6% on previous corresponding period. This includes EBITDA loss of $0.15 Mn from Seeka Australia due to a very dry summer resulting in lower Hayward kiwifruit volumes and an underperforming nashi programme, as compared to gain of $2.71 Mn in the previous corresponding period.

Consolidated profit after tax increased by 27.3% to $11.86 Mn, as compared to $9.32 Mn in the previous corresponding period. Cash flow from operations increased by 107% to $5.15 Mn, as compared to $2.49 Mn in the previous corresponding period.

Net debt, i.e., bank loans less bank deposits as on June 30, 2019, was reported at $148.08 Mn, an increase of $32.1 Mn from the previous corresponding period. This was mainly due to investment in post-harvest capacity and the Aongatete acquisition.

The Board of Directors declared a (fully imputed) dividend of $0.12 per share with record date and payment date on September 13, 2019 and October 9, 2019, respectively. The dividend reinvestment plan (DRP) was applicable to the distribution with a 2% discount applied to determine the strike price.

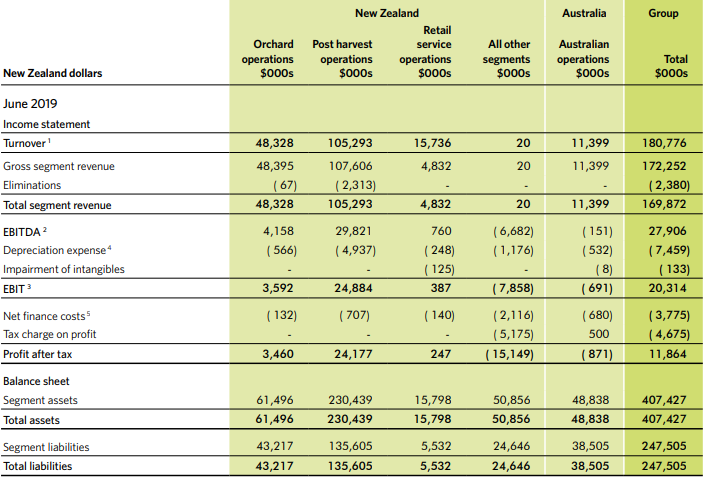

H1FY19 Financial Statement (Source: Company Reports)

New Zealand Operations: Orcharding kiwifruit volumes from new production associated with the Northland and Aongatete acquisitions in the year 2019, increased to 41.11 Mn kilograms of kiwifruit, as compared to 37.44 Mn kilograms in the previous corresponding period. The company also grew avocados and kiwiberry of weight 732,000 kilograms and 64,400 kilograms, respectively, as compared to 200,000 kgs and 15,000 kgs, in the previous corresponding period.

Australian Operations: Company’s 100% owned-entity, Seeka Australia PTY Limited, owns and operates kiwifruit, nashi and pear orchards along with associated post-harvest facilities in Victoria, and directly markets Seeka produce to retailers. A very hot and dry summer impacted Kiwifruit yields, i.e., fruit size, however, kiwifruit remained profitable even at lower yield levels. The green nashi sales program suffered loss, following which volumes and planted areas were reset to match the crop to profitable market opportunities.

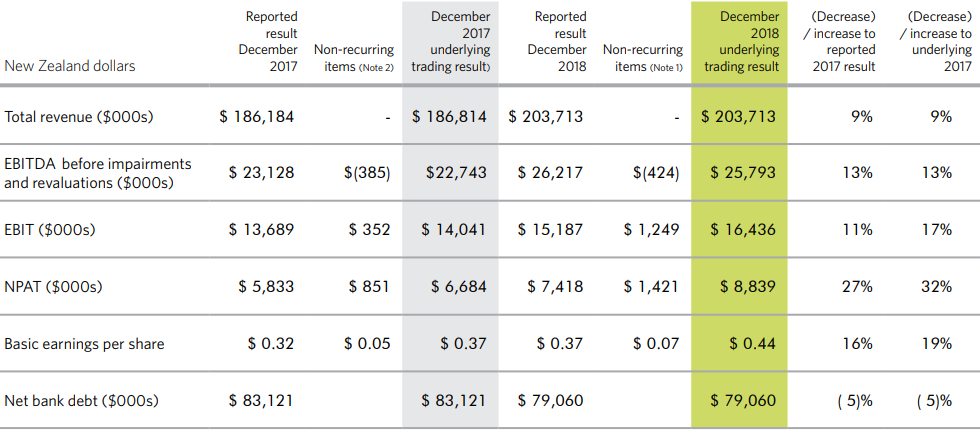

FY18 Financial Highlights for the period ended December 31, 2018: Total revenue for the period improved by 9% to $203.71 Mn, as compared to $186.81 Mn on previous year. This was mainly due to an increase in sales of Hayward Kiwifruit Volumes in New Zealand after an industry-wide decline in 2017, along with an increase in SunGold Volumes and the increased volumes associated with the acquisition of the T&G Horticulture kiwifruit assets and business in Northland. Profit after tax for the period improved by 27% to $7.42 Mn, as compared to $5.38 Mn on previous year. EBITDA for the period improved by 13% to $26.22 Mn, as compared to $23.13 Mn on previous year.

Net debt, i.e., bank loans less bank deposits as on December 31, 2018, was reported at $79.06 Mn, a decrease of $4.06 Mn than a year before.

FY18 Key Financial Metrics (Source: Company Reports)

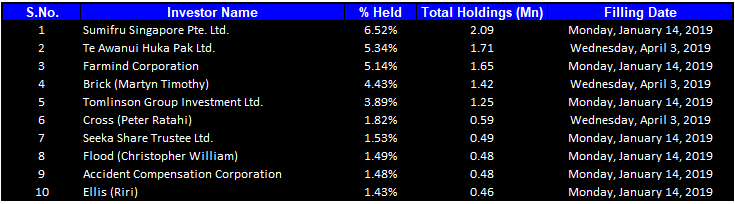

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 33.07% of the total shareholding. Sumifru Singapore Pte. Ltd. and Te Awanui Huka Pak Ltd. hold maximum interests in the company at 6.52% and 5.34%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

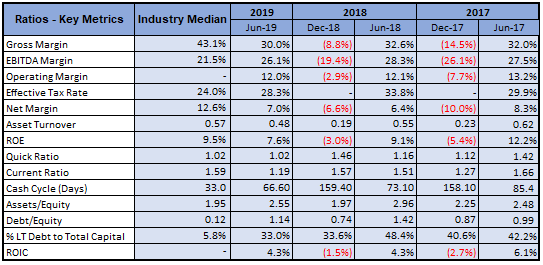

A Quick Look at Key Metrics: Its EBITDA margin for H1FY19 stood at 26.1%, better than the industry median of 21.5%. Its net margin improved from 6.4% in H1FY18 to 7.0% in H1FY19. Its cash cycle improved from 73.10 days in H1FY18 to 66.60 days in H1FY19, implying that the company is efficiently managing its asset-liability balances. Moreover, its debt to equity ratio reduced from 1.42x in H1FY18 to 1.14x in H1FY19.

Key Metrics (Source: Thomson Reuters)

What to expect: As per the release, the company is expecting lower operational earnings for the second half of the financial year 2019, reflecting lower volumes of fruit in store as on June 30, 2019 and an early selling season. It has continued with its strategy to market, negotiate and sell Northland orchards. Moreover, it has started enacting a similar strategy for the Australian market.

SEK is highly optimistic about its Australian investment and its Australian orchard portfolio. Its investments in Australian operation is expected to play an important role in extending its geographical reach and product range. It aims to upgrade its existing orchards along with developing new orchards plus invest further on water to grow production. Its yields per hectare and total volumes over the three years are expected to improve with the maturity of new plantings.

The company continues to test the production and marketing of its new kiwifruit and licensed pear varieties on its Australian orchards. It has 70 hectares of kiwifruit and 26 hectares of pears in development, which is expected to add to production from 2020 onwards.

It is expected that following realization of sale proceeds, company’s debt would reduce substantially. With this, company has provided its FY19 EBITDA guidance, which is better than FY18 result.

FY19 Guidance (Source: Company Reports)

FY19 Guidance (Source: Company Reports)

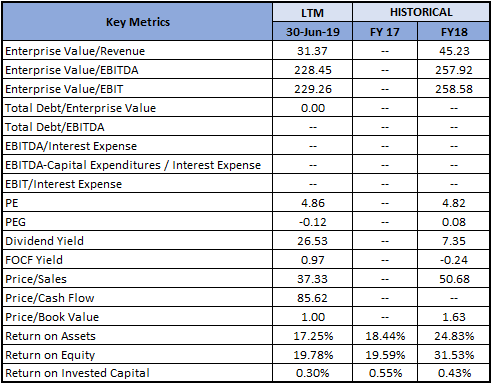

Key Valuation Metrics (Source: Thomson Reuters)

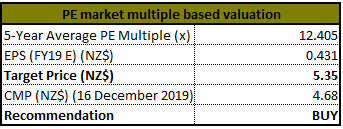

Valuation Methodology: Price to Earnings Market Multiple Approach

Price to Earnings Market Multiple Approach (Source: Thomson Reuters), NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

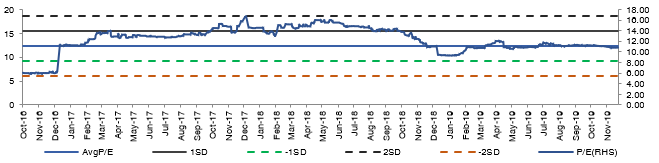

Historical PE Band (Source: Thomson Reuters)

Technical Overview:

Monthly Chart-

.png)

Monthly Chart (Source: Thomson Reuters)

.png)

Stock Recommendation: The stock price posted a positive YTD return of 8.83%. Currently, the stock is trading towards its 52-week low of $4.20, proffering an opportunity for share accumulation. Company’s top-line and bottom-line have shown a decent performance over the past four years for the period FY14-18, with CAGR ~15% and ~23%, respectively. Company’s Northland acquisition is expected to help it in consolidating its operation plus helping it in pursuing the buying opportunity of Aongatete, which is a reputable competitor in the region. SEK has developed a world-class post-harvest facility in Kerikeri and is now pursuing a similar sale and potential leaseback strategy for orchards in Australia. Substantial cash gains realized by the ongoing sales of its Northland orchard portfolio is expected to benefit the company in its initiatives for expansion and reducing debt. Key risks to valuations could be from the seasonal labors where the industry is relying on overseas labour to complement the available local workforce. Looking at the business prospects over the long-term, we have valued the stock using a PE market multiple method and arrived at a target price of lower double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$4.68 per share on December 16, 2019.

.png)

SEK Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...