Company Overview: Sanford Limited is a seafood company, which is engaged in farming, processing and aquaculture business. The Company's segments include wildcatch, which is responsible for catching and processing inshore and deepwater fish species, and aquaculture, which is responsible for farming, harvesting and processing mussels and salmon. The Company's farming business includes Fleet, which operates a fleet of vessels for inshore, purse seine and deepwater fishing, including vessels for freezing and processing at sea. The Company's aquaculture business includes Mussel Farming, Oyster Farming and King Salmon Farming. The Company's Sea food products include Antarctic toothfish Arrow squid, Blue mackerel, Bluff Oyster, Gemfish, Ghost shark, Hake, Hapuku, Hoki, Jack mackerel, John dory, Kahawai, King Salmon, Lemon sole, Ling, Monkfish, Orange roughy, Patagonian toothfish, Red cod, Scampi, Silver warehou, Snapper, Trevally and Yellowbelly flounder.

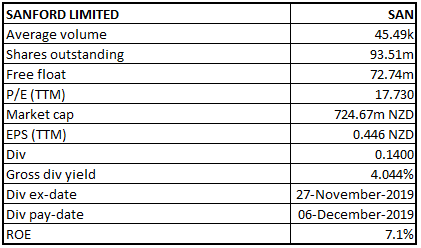

SAN Details

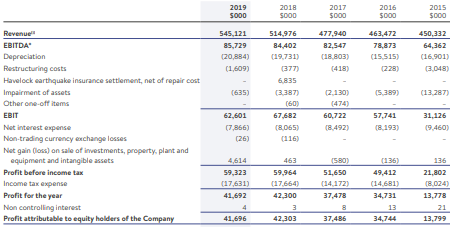

Performance of SAN Between FY15-19 Improved Significantly: New Zealand’s leading seafood company, Sanford Limited (NZX: SAN) focuses on sustainability and on maximising the value of the resources it gathers from the oceans, enabling long term value creation from oceans teeming with life. It has workforce strength of ~1,700 employees with eleven sites across the country. Looking at the past performance over FY15 to FY19, total revenue and net income of the company have grown with a CAGR (compounded annual growth rate) of 5.54% and 31.85%, respectively. Group’s total revenue improved from $439.3 Mn in FY15 to $545.1 Mn in FY19, and net income improved from $13.8 Mn in FY15 to $41.7 Mn in FY19. Considering the continuing and substantial investment needs (both capital as well as operational expenditure) that is needed from the transition and asset rejuvenation perspective, the Board decided that the dividend should remain at 23 cents per share (or cps). Notably, the final dividend amount stood at 14 cents per share.

The company added that the demand for marine extracts is huge and it is expected to grow. As per the release, greenshell mussel powder is known for assisting with inflammation management including for athletes, older people, or for anyone who has been troubled by joint aches and pains. The company made an announcement about the intention to create a $20 million Marine Extracts Centre in Blenheim. The Centre would be focusing on discovery and production of high value nutrition products from NZ seafood. Sanford is already producing high quality Greenshell mussel powder from the small facility in Blenheim and the success of this product convinced SAN to go several steps further. The concept plans and drawings have already been prepared and the construction is expected to begin in April 2020. It is expected to employ more than 40 people with wide range of roles from scientific research to production.

Historical Performance for FY15-19 (Source: Company Reports)

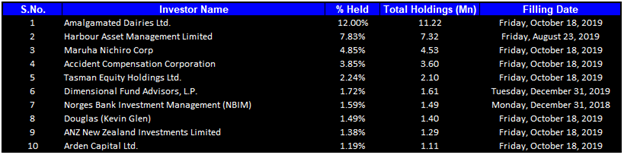

Top 10 Shareholders: Amalgamated Dairies Ltd. and Harbour Asset Management Limited hold maximum interests in the company at 12.00% and 7.83%, respectively. The top 10 shareholders have been highlighted in the table below:

Top 10 Shareholders (Source: Thomson Reuters)

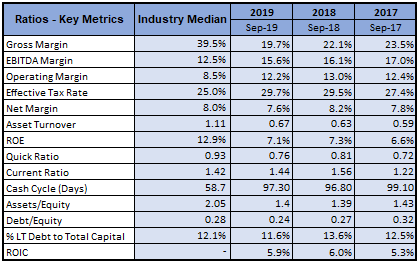

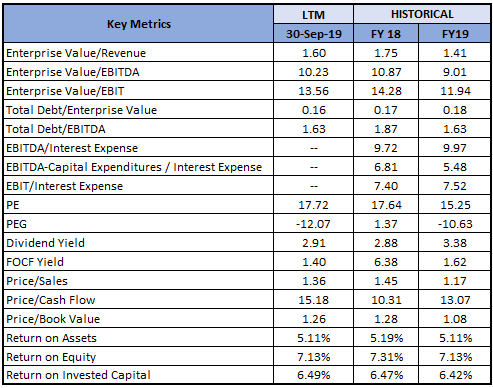

A Quick Look at Key Metrics: Its EBITDA margin for FY19 stood at 15.6%, better than the industry median of 12.5%. Its net margin for FY19 stood at 7.6%, higher than the industry median of 8.0% and, therefore, it can be said that the company is possessing decent capabilities to convert its top line into bottom line as compared to the broader industry. Its current ratio for FY19 stood at 1.44x, better than the industry median of 1.42x, which implies that the company is in a good position to address its short-term obligations. Also, decent liquidity levels might provide the company with opportunities to make deployments towards strategic growth objectives which could help in achieving long-term growth.

Key Metrics (Source: Thomson Reuters)

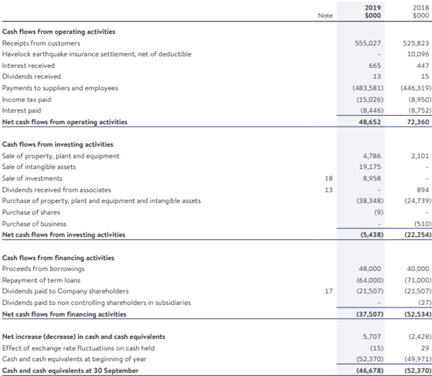

FY19 Key Highlights for The Period Ended September 30, 2019: Net Profit After Tax (NPAT) for the financial year 2019 stood at $41.7 million, as compared to $42.3 million in FY18. Underlying adjusted Earnings before Interest and Tax (EBIT) for the period was reported at $64.8 million, as compared to $64.7 million in the previous year. Despite the sales volume declining by 5% (on previous year) to 115,000 tonnes, sales revenue for the period increased by 8% (on previous year) to $558 million. Gross margin for the period improved by $6.3 million with favourable sales pricing, product mix and sales channel optimisation more than offsetting cost pressures such as higher labour and fuel costs.

SAN’s balance sheet was strengthened with the decrease of year-end debt by $16 million to $139 million. This increase in the debt headroom would be utilised for capital investment to advance the business across numerous fronts. Its operating cash flow for the period was reported at $48.7 million, as compared to $72.4 million last year.

FY19 Cash Flow Statement (Source: Company Reports)

Recent Updates: On January 29, 2020, the company announced the appointment of Fiona Mackenzie as the newest member of its board of directors, effective from February 1, 2020. Her appointment is following the retirement of Mr Paul Norling. She brings with herself right skills, qualifications and experience for the role.

On January 21, 2020, the company informed the market that it was pleaded guilty to the three charges in the Invercargill District Court of fishing in a Benthic Protection Area (BPA), reflecting incidents where one of its vessels inadvertently strayed into a BPA while fishing. Responding to this, the company has highlighted that the incursions were a mistake and in no way intentional, and it plans to avoid such mistakes in future. It has developed and adopted technology that creates an electronic fence system around sensitive areas which SAN’s fishing vessels should avoid. Even if the skipper fails to respond to the alarm, the shore-based vessel manager will be alerted who can take the requisite steps.

Key Risks: The company faces a risk of climate change where warmer waters and adverse weather conditions plays out in the oceans affecting its earnings. The company’s strategy to mitigate the risk through investing towards innovation throughout the business and bringing the customer focus to life at the same time is actually paying off.

What to Expect: The company added that deployments have been made in FY 2019 towards processing plant improvement on the vessels and in sites supporting operational excellence. Operational investments in Precision Seafood Harvesting technology on the vessels as well as in reducing ambient temperatures in the landing pounds and processing areas supported the company’s ability to improve and maintain catch quality. Notably, the company has also deployed towards technology and training to put robust risk mitigation systems in place in Big Glory Bay farms, as it has acknowledged that climate change happens to be the significant risk.

SAN’s priority areas under FY20-22 capital investments include, 1) Marine extracts facility and equipment, 2) Scampi vessel replacements, 3) Mussel water space expansion, 4) Salmon capacity growth, 5) San Core Project, and 6) Australia footprint.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

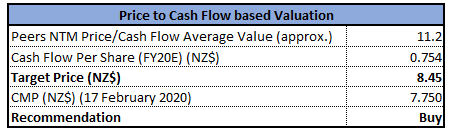

Price to Cash Flow Multiple Approach

Price to Cash Flow Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Analysis:

Monthly Chart:

(Source: Thomson Reuters)

Weekly Chart:

(Source: Thomson Reuters)

On both the charts, the stock is trading above 20 EMA, 50 EMA and 200 EMA, indicating bull trend. On weekly chart, previous week candlestick was the green candle (bullish candle) on the 20 EMA, suggesting continuation of trend. The stock is expected to test the level close to $8.2021 (Fibonacci Projection level of 38.2%), underpinned by stochastic oscillator suggesting the stock to be oversold region.

Note: EMA – Exponential Moving Average.

Stock Recommendation: The company is investing in the innovation to create new revenue streams from the marine resources. It plans to improve its margins by reducing and containing its fixed costs and to recover its investments in sales and marketing. The company’s policy is to maintain robust capital base in order to maintain investor, creditor and market confidence as well as to sustain future development of the business. The company stated that continued strong demand along with channel diversification are keeping the returns high. The company stated that NZ remains at the forefront of sustainable fisheries management globally and Fisheries New Zealand’s announcement with respect to an ambitious aquaculture strategy for the country was encouraging and it highlighted the potential of the industry.

Given the backdrop of the aforesaid parameters, decent balance sheet and cash flow position, favourable outlook, prudent execution of its business strategy, and strategic investment approach into innovative marine extracts centre, we have valued the stock using a relative valuation method, i.e., Price to Cash Flow multiple, and arrived at a target price of higher single-digit growth (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $7.750 per share, down by 1.90% on February 17, 2020.

SAN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...