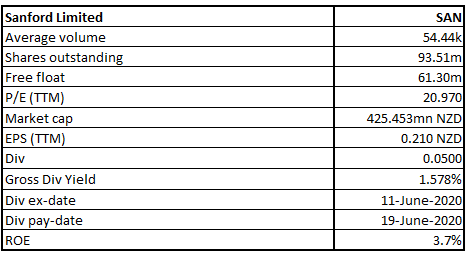

SAN Details

Company Overview: Seafood company, Sanford Limited (NZX: SAN) is engaged in the farming, processing, and aquaculture business. Its wild catch segment is into catching and processing inshore and deepwater fish species. Its aquaculture segment is into farming, harvesting and processing mussels and salmon. Its farming business operates a fleet of vessels for inshore, purse seine and deepwater fishing, including vessels for freezing and processing at sea. Its aquaculture business includes Mussel Farming, Oyster Farming and King Salmon Farming. Its seafood products include Antarctic toothfish Arrow squid, Blue mackerel, Bluff Oyster, Gemfish, Ghost shark, Hake, Hapuku, Hoki, Jack mackerel, John dory, Kahawai, King Salmon, Lemon sole, Ling, Monkfish, Orange roughy, Patagonian toothfish, Red cod, Scampi, Silver warehou, Snapper, Trevally and Yellowbelly flounder.

Sanford Limited (NZX: SAN) is New Zealand’s largest and oldest seafood company that is listed on the New Zealand stock market since 1924. The company has a market capitalisation of ~$425.453 million on 24th May 2021.

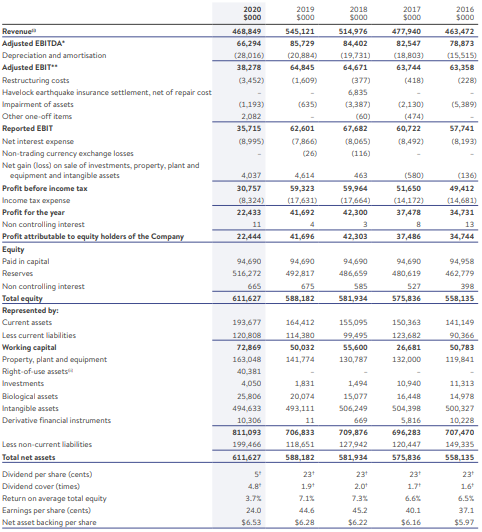

Looking at the past performance, SAN’s top-line for FY16-20 grew with a compounded annual growth rate (CAGR) of 0.28%. Its total revenue for FY20 stood at $468.8 million, as compared to $463.5 million in FY16.

Results Performance (Half-Year Ended 31 March 2021)

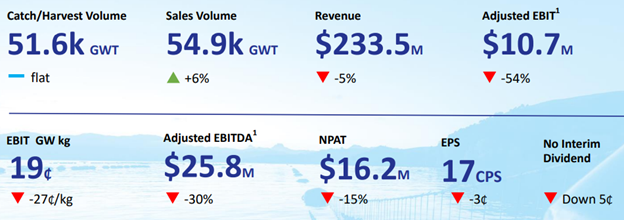

Revenue of the company from continuing operations for the half-year period stood at $233.51 million, a decline of 4.9% on the previous corresponding period (pcp), which can be attributed to the continued challenging conditions during the six months due to the impact of the Covid-19 pandemic on the demand for seafood and on international supply chains.

Adjusted Earnings Before Interest and Tax (Adjusted EBIT) for the first six months stood at $10.7 million, a decline of 54% on pcp. Net profit after tax (NPAT) for the interim period stood at $16.20 million (including a $13.3 million gain on sale for two non-core properties), a decline of 14.8% on pcp.

SAN’s balance sheet remains strong, with net debt at $181 million which was $3 million lower than September 30, 2020 and the gearing ratio (debt as a proportion of debt plus equity) was at 23.8% (from 23.4% at September).

Exhibit 1: Key Financial Statistics

H1FY21 Results snapshot (Source: Company Reports)

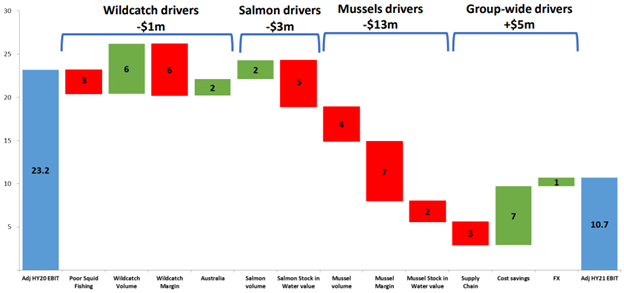

On a divisional basis, Wildcatch and salmon, which were impacted earlier in the pandemic, have begun to show early signs of recovery, particularly in volume. However, prices for mussels, which were held up in the six months to September 2020, came under substantial pressure during this period due to an excess of supply over demand.

Wildcatch profitability came below pre-Covid levels with reduced global demand impacting price. However, it has started to stabilise with wildcatch profit contribution largely unchanged.

Salmon reported strong revenue growth of 12% on pcp, driven by a growing retail presence in both New Zealand and the US. Salmon made the largest profit contribution to the group in this half.

Greenshell mussels’, with the highest exposure to the foodservice, were hardest hit by Covid-19 because of the restrictions on restaurants globally.

Exhibit 2: Segment Performance

(Source: Company Reports)

Results Performance (Year Ended 30 September 2020)

Total revenue of the company for the full-year period stood at $468.85 million, a decrease of 14% (y-o-y), mainly due to the Covid-19 pandemic and its impact on foodservice globally. There was a 30% fall in the company’s sales in North America compared to last year. The period witnessed the harvesting of more fish and shellfish than last year (with the exception of toothfish), but more stock than usual has gone to inventory due to the fall in demand of high-value products, reducing the company’s margins further and increasing the cost base.

Adjusted (underlying) Earnings Before Interest and Tax for the period declined by 41% to $38.3 million as compared to $64.8 million in the previous year. Reported Net Profit After Tax (NPAT) for the period decreased by 46% to $22.4 million, as compared to $41.7 million in the previous year.

The Board decided not to pay a final dividend in respect of the 2020 financial year to ensure prudent cash availability.

Exhibit 3: Income Statement

Full-year financial review (Source: Company Reports)

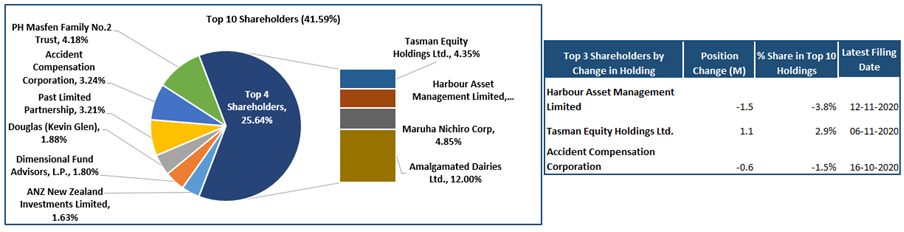

Top 10 Shareholders: The top 10 shareholders have been highlighted in the pie chart, which together forms around 41.59% of the total shareholding. Amalgamated Dairies Ltd. and Maruha Nichiro Corp are holding a maximum stake in the company at 12.00% and 4.85%, respectively.

Exhibit 4: Top 10 Shareholders

Source: Refinitiv, Thomson Reuters, Analysis by Kalkine Group

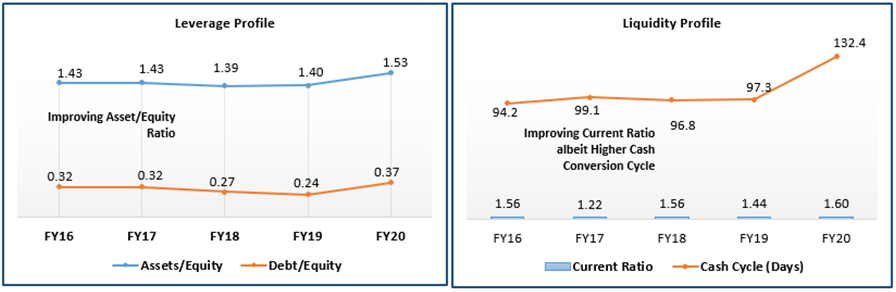

A Quick Look at Key Metrics: The company witnessed an improvement in asset/equity ratio over the years, while its debt/equity ratio has also been increasing. Its current ratio, however, has improved over the years, and it stood at 1.60x for FY20, implying that the company possesses better capabilities to meet the short-term obligations.

Exhibit 5: Key Metrics

Source: Refinitiv, Thomson Reuters, Analysis by Kalkine Group

Outlook:

The company is positioning itself as foodservice re-opens in key markets, emboldened by mass vaccination and a sharp decline in new cases of COVID-19 in many geographies. Its robust balance sheet supports funds deployment to accelerate the growth process with its innovation strategy, specifically with the marine extracts as well as its asset rejuvenation strategy. The continued strong demand and channel diversification are supporting the returns. The company is planning to improve the margins by reducing and containing fixed costs and recovering the investments in sales and marketing.

Risk:

The global supply disruptions are causing significant challenges before the company. Its supply chain costs have risen by 12% on a cost per tonne basis which could have an adverse impact on the bottom-line of the company. Further, it is also exposed to the risk of regulatory and environmental rules compliance.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

.png)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart –

.png)

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

After the previous week of a sharp decline, the stock has given a stronger close on the first trading session of the ongoing week, forming a ‘Bullish Harami’ pattern on the chart which signals a bullish reversal for the stock. The technical indicator RSI with a reading around 42 and a curve pointing up, suggests neutral to up momentum.

Going forward, the stock may have resistance around a 23.6% retracement level of $5.00 whereas support could be around the lower Bollinger band of $4.38.

Stock Recommendation:

There has been a significant impact of the pandemic on the sales and profitability of the company. However, there also have been signs of improvement in situations with the re-opening of foodservice in the company’s key markets. The company is focused on opening new channels while preserving its position in key sectors.

We have valued the stock using P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We have assigned a slight premium to Price/EPS Multiple (NTM) (Peer Average) considering decent liquidity position which could help the company moving forward.

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$4.550 per share, up by 3.41% on May 24, 2021.

Note: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...