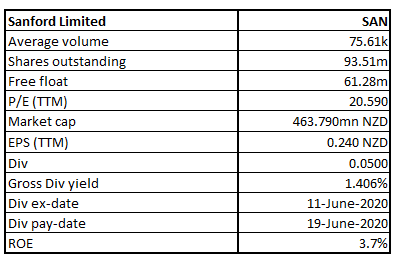

SAN Details

Company Overview: Seafood company, Sanford Limited (NZX: SAN) is involved in farming, processing and aquaculture business. Its wild catch segment is responsible for catching and processing inshore and deepwater fish species. Its aquaculture segment is responsible for farming, harvesting and processing mussels and salmon. Its farming business includes Fleet, which operates a fleet of vessels for inshore, purse seine and deepwater fishing, including vessels for freezing and processing at sea. Its aquaculture business includes Mussel Farming, Oyster Farming and King Salmon Farming.

.png)

Sanford Limited (NZX: SAN) is New Zealand’s largest and oldest seafood company that is listed on the New Zealand stock market since 1924. The company has a market capitalisation of ~$463.790 million on 18th January 2021.

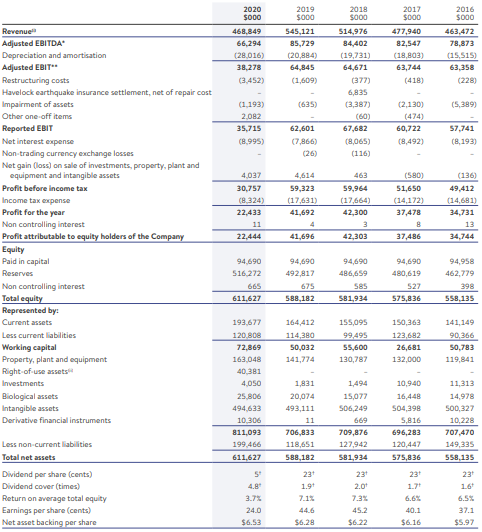

Results Performance (Year Ended 30 September 2020)

Total revenue of the company for the full-year period stood at $468.85 million, a decrease of 14% (y-o-y), mainly due to the Covid-19 pandemic and its impact on foodservice globally. Seafood companies are primarily reliant on food service as a sales channel which has been hard hit by the COVID-19 led lockdowns. Sanford experienced a sales fall of 30% YoY in North America itself. Adjusted (underlying) Earnings Before Interest and Tax (EBIT) for the period decreased by 41% to $38.3 million, as compared to $64.8 million in the previous year. Reported Net Profit After Tax (NPAT) for the period declined by 46% to $22.4 million, as compared to $41.7 million in the previous year.

The Board in order to ensure prudent cash management has decided not to pay a final dividend in respect of the 2020 financial year.

Exhibit 1: Performance Track Record

Source: Company Reports

During the year FY20 the company has been able to build up strong inventory both in terms of volume and value of seafood, which can reap benefits as the economy returns to revival post COVID-19.

Exhibit 2 : Seafood Inventory Build-up in FY20

.png)

Source: Company Reports

Diverse geographical spread enabled the company to reduce the COVID-19 impact in FY20. Despite Covid-19 lock-down, sales to Europe and Australian regions showed resilience in FY20. The company reported nearly flat sales in Europe driven by higher white fish sales and diversification of Mussels away from North America. North America was impacted due to lower Toothfish and Squid sales in FY20.

.png)

Source: Refinitiv (Thomson Reuters)

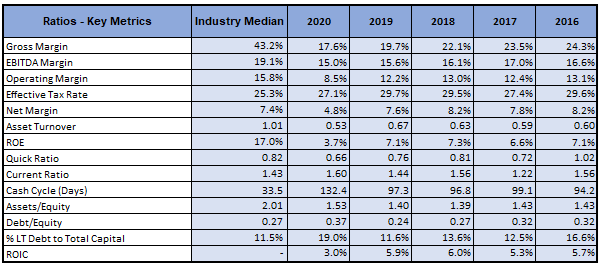

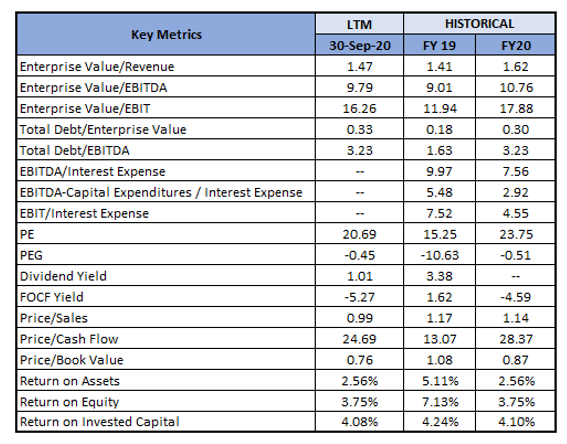

A Quick Look at Key Metrics: The company’s current ratio for FY20 stood at 1.60x, better than the result of FY19 at 1.44x, implying that the company possesses better capabilities to meet the short-term obligations.

Exhibit 5: Key Metrics

Source: Refinitiv (Thomson Reuters)

Outlook:

The company’s robust balance sheet supports funds deployment to accelerate the growth process with its innovation strategy, specifically with the marine extracts as well as its asset rejuvenation strategy. The company is planning to improve the margins by reducing and containing fixed costs and recover its investments in sales and marketing. The strategy to focus on more consumer-facing sales and plan to more flexibly response to changing environment will ensure increased profitability for the company. FY20 capital expenditure was reduced to $48 million, and a similar level is expected in FY21 in the range of ~$45 million-$55 million.

Despite of increase in debt, the company’s balance sheet remains robust. The company is possessing sufficient headroom in the borrowing facilities ($83 million as at 30th September 2020) which could help it in achieving its growth objectives and navigate challenging operating environment. With regards to operating expenditure, the company stated that reduction in discretionary spending will be maintained in H1 FY 2021.

Industry Outlook:

With the focus on regional comprehensive economic partnership (RCEP) which comprises free trade agreement between many Asia-Pacific nations, New Zealand’s primary sector is expected to benefit with access to a wider market. Already, the sector is among the key contributing segment in the NZ’s GDP with the export from aquaculture/marine products, dairy products, forestry products, etc.

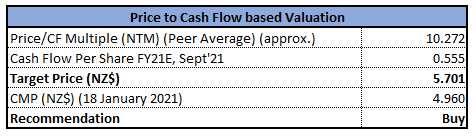

Valuation Methodology: P/CF Based Relative Valuation (Illustrative)

P/CF Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Exhibit 6: Key Valuation Metrics

Source: Refinitiv (Thomson Reuters)

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has given a stronger closing in the first trading session of the ongoing week forming a ‘Bullish Harami’ pattern thereby suggesting near-term upside for the stock. The technical indicator RSI with a reading around 38 suggests gaining of momentum.

Going forward, the stock may have resistance around the 23.6% retracement level of $5.41 whereas support could be around the previous low of $4.79.

Stock Recommendation:

The company’s balance sheet and liquidity remains robust, with a gearing ratio at 31% which is expected to help the company to sail through the present challenges by making careful choices while managing asset rejuvenation programme, balancing investment needs with cashflow realities. In addition, strong demand for the Big Glory Bay brand in North America and the resilient Mussel powder pet market will help boost the sales and profitability of the company.

We have applied P/CF multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$4.960 per share, up by 0.40% on January 18, 2021.

.png)

SAN Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...