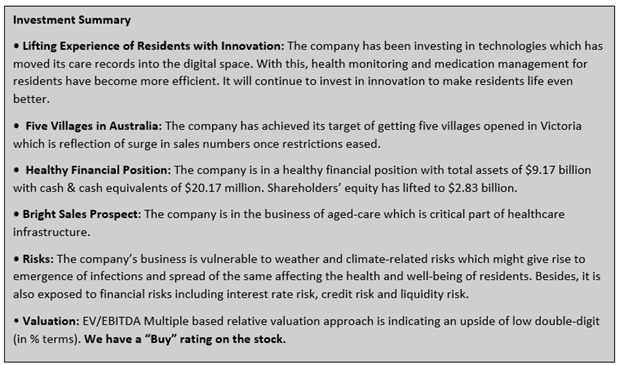

Company Overview: Ryman Healthcare Limited (NZX: RYM) develops, owns and operates integrated retirement villages, rest homes and hospitals for elderly people. The Company offers various living and care options, including independent living, assisted living, rest home, hospital and dementia. The Company offers a specialized care unit for residents. The Company's Villages include residents requiring short-term care, respite care, and day care. The Company also offers Day Care program for those just needing assistance during the day. The Company operates in New Zealand with various operations in Australia.

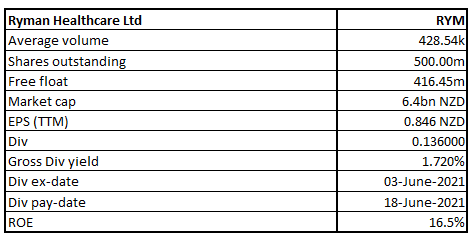

RYM Details

Ryman Healthcare Limited was founded in Canterbury in 1984 to provide retirement living and care options in New Zealand. The company has a market capitalisation of around $6.4 billion as on 26th July 2021.

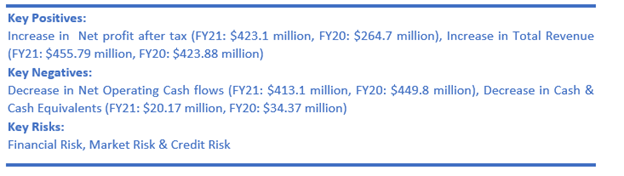

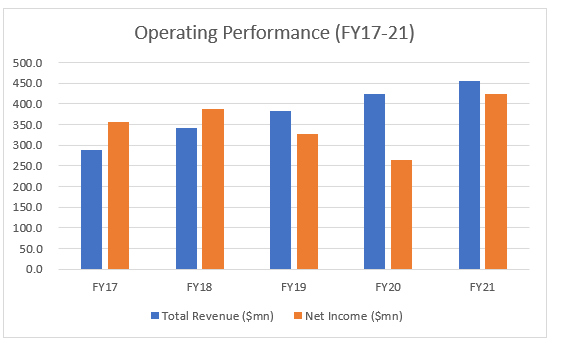

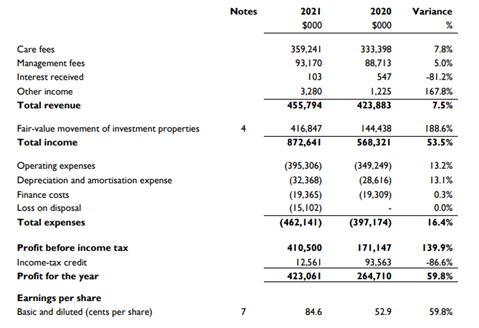

Decent Past Performance: Looking at the past performance, RYM’s top-line and bottom-line for FY17-21 grew with a compounded annual growth rate (CAGR) of 12.05% and 4.36%, respectively. Its total revenue for FY21 stood at $455.8 million, as compared to $289.2 million in FY17. Its net profit for FY21 stood at $423.1 million, as compared to $356.7 million in FY17.

Exhibit 1: Operating Performance

(Source: Company Reports, Analysis by Kalkine Group)

Results Performance (Year Ended March 31, 2021 – FY 2021)

Exhibit 2: Income Statement

(Source: Company Reports)

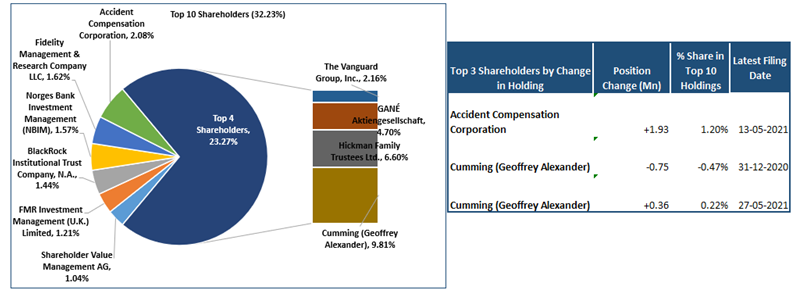

Top 10 Shareholders:

The top 10 shareholders have been highlighted in the pie-chart, which together forms around 32.23% of the total shareholding. Cumming (Geoffrey Alexander) and Hickman Family Trustees Ltd. are holding a maximum stake in the company at 9.81% and 6.60%, respectively, as provided in the chart shown below:

Exhibit 3: Top 10 Shareholders

Source: Analysis by Kalkine Group

A Quick Look at Key Metrics:

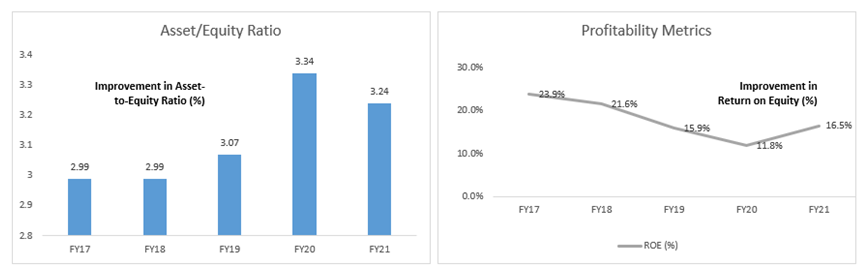

As can be depicted from the below chart, Asset/Equity ratio of the company rose from 2.99x in FY 2017 to 3.24x in FY 2021. Notably, YoY improvement was witnessed in the company’s ROE. In FY 2020, ROE was 11.8% and, in FY 2021, it was 16.5%, which implies that the company has delivered decent returns to its shareholders.

Exhibit 4: Key Metrics

Key Risks:

The company stated that there could be some ongoing uncertainty because of the pandemic. Also, elderly people are more prone to Covid-19 which could influence the company’s operations.

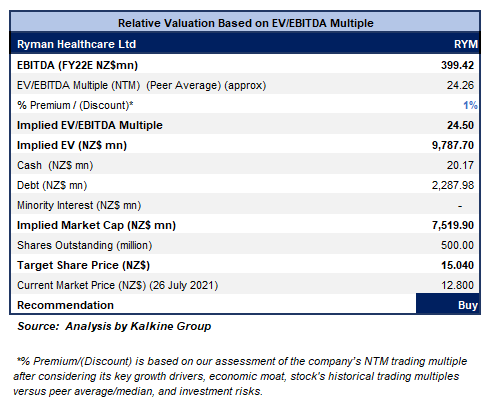

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

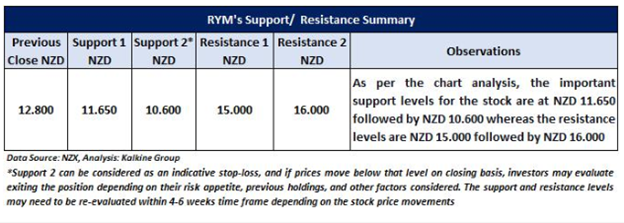

Technical Overview:

Chart:

Source: REFINITIV

Note: Purple Color Line Reflects RSI (14-Period)

Stock Recommendation:

The company’s stock declined by ~13.16% in 9 months. It has made a 52-week low and high of $12.15 and $16.02, respectively.

We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price that reflects the rise of low double-digit (in percentage terms). We have applied a slight premium to EV/EBITDA multiple (NTM) (Peer Average) considering rise in NPAT and its operations in aged-care business segments. Also, the company witnessed a rise in cash and cash equivalents which could help the company in tackling challenges ahead. In the coming period, the company is expected to see improvement in its earnings with the rise in the old population and increase in immigration activities.

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$12.800 per share, down by 1.69% on July 26, 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...