.png)

I. Sector Landscape and Outlook

As per the Ministry for Primary Industries (MPI), New Zealand export food and primary products to more than 200 markets around the world. Further, this sector contributes ~80% of all New Zealand’s exported goods. MPI also monitors the import of ingredients and products from trading countries. The top ten export items for the year to March 2021 include Dairy contributing 40% of total export revenue, followed by Meat and Wool 22%, Forestry 13%, Horticulture 14%, Seafood 4%, Arable 1%, and Other primary sectors contributing 7% of total export revenue.

Export revenue for the year ending June 2021 is anticipated to decrease by 1.1% to $47.5 billion. For the year ending June 2022, export revenue is anticipated to reach $49.1 billion, driven by demand recovery for main export items in destination markets.

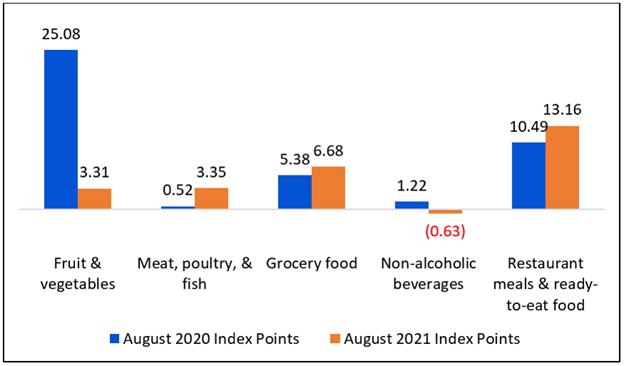

The Food Price Index Extended Their Rising Momentum in August 2021

As per Stats.NZ, the food prices increased by 0.3% in August 2021, while after seasonal adjustment, the index was up 0.2%. This rise was contributed by the rise in fruit and vegetable prices by 0.4% (up 0.2% after seasonal adjustment), meat, poultry, and fish prices increased 1.3%. Also, grocery food prices increased 0.1% (up 0.2% after seasonal adjustment), non-alcoholic beverage prices increased 0.5%, and restaurant meals and ready-to-eat food prices increased 0.4%.

Meanwhile, the food prices grew 2.4% in the year ended August 2021, where fruit and vegetable prices grew 2.1%, followed by restaurant meals and ready-to-eat food prices that grew 4.6%. Further, the grocery food prices rose 1.9%, and meat, poultry, and fish prices rose 2.2%, while the non-alcoholic beverage prices fell 0.6%.

Exhibit 1: Monthly Index Points Contribution to Food Price Index Continues to Rise

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

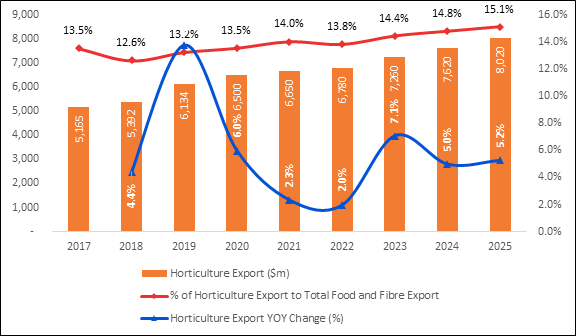

Consistent Contribution of Horticulture Export Revenue to Total Food and Fibre Sector Export Revenue

As per the Ministry for Primary Industries New Zealand, horticulture revenue is anticipated to increase 2.3% in the year ending June 2021 to $6.6 billion, primarily driven by strong crops and export volumes of kiwifruit and avocados. Demand for New Zealand fresh fruit and wine from international markets remained robust despite COVID-19 related circumstances that are anticipated to continue further. In FY22, the horticulture export revenue is anticipated to grow by ~2.0% and more than ~5% in subsequent future years as indicated in Exhibit 2. Also, the contribution of horticulture export revenue to total food and fibre sector export revenue is ~14-15% consistent.

Exhibit 2: Decent Trend in Horticulture Export Revenue

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

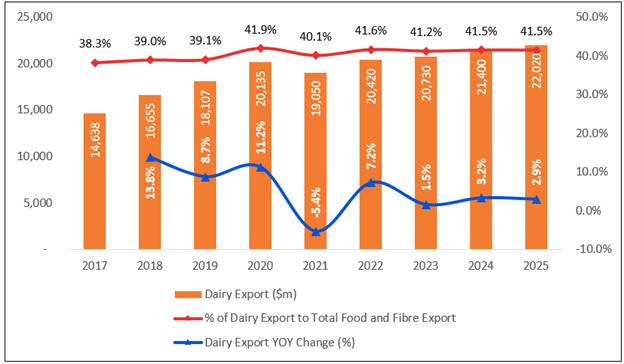

Growth Expected in Future Period for Dairy Products

As per the ‘Situation and Outlook for Primary Industry – June 2021, released by the Ministry for Primary Industries New Zealand, the dairy export revenue is anticipated to fall 5.4% to $19.0 billion in the year ending June 2021, primary due to COVID-19 related circumstances and disruptions. In the first half of FY21, dairy revenue fell significantly due to global supply chain and market disturbances, and low prices for key commodities. However, the global dairy prices jumped in the second half of FY21. Driven by the second half of FY21 demand momentum, the milk production for the 2020-21 season is anticipated to rise 1.9%.

Exhibit 3: Near-term Headwinds in Dairy Export but Growth Expected in Future Period

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

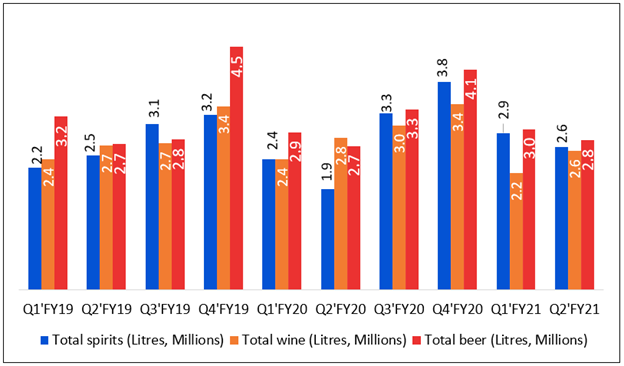

Fall in Alcohol Available for Consumption for All Beverages in Q2FY21

As per Stats.nz, alcohol available for consumption for all beverages in Q2FY21 fell by 0.5% from Q1FY21, which fell by 29.2% over Q4FY20, primarily driven by a decrease in consumption for Total beer, Total spirits, and Total Wine. This indicates the fall in alcohol available to the consumer is narrowing. Fall in demand for these items also indicates lower spending on alcohol and consumer shift towards substitute products.

Exhibit 4: Momentum in Alcohol Available for Consumption Expected to Increase

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 10-year return of ~303.07% versus ~185.33% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~117.74% in 10-year.

Exhibit 5: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

Source: REFINITIV

Key Risks and Challenges:

The Ministry for Primary Industries is responsible for planning and enforcing standards and rules for New Zealand’s food safety, biosecurity, primary production, and animal welfare systems. Primary legislation and standards controlling the primary sector in New Zealand include ‘The Biosecurity Act’, ‘The Food Act’, ‘Australia – New Zealand joint food standards’, ‘Animal Products Act’, ‘Agricultural Compounds and Veterinary Medicines Act’, and ‘Forestry Acts’, among others. These rules set by MPI are to protect the consumer’s interest and at the same time maintain a quality standard in the international market. Therefore, any variances from the rules could impact the operations and financials of the associated company.

The alcohol industry is competing to make its presence in online sales to reach a larger consumer base, like other successful online industries. While few alcohol brands have made their presence felt in the online sphere, others have learned that they need to create strategic partnerships. Further, the industry is facing high competition than before and had to deal with frequent changes in regulations and compliance requirements.

Exhibit 6. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the New Zealand Treasury, the growth of New Zealand’s primary sector has been robust in comparison to the economic growth over the last 25 years. This growth momentum is primarily driven by the performance of agriculture, and natural comparative advantage, sound productivity, favourable trade terms, the use of new technology, exploitation of economies of scale, and the advantage of rising stable macroeconomic events, and high-quality institutions, among other factors.

Looking ahead, the primary sector has a sustained growth outlook, primarily driven by favourable international trade conditions, environmental constraints (regarding water and climate change), property rights, biosecurity threats, and human capital issues. Also, the sectoral growth will be determined by the response of the individuals and companies in the sector to the external environment in which they operate.

As per the Ministry for Primary Industries, the increase in dairy commodity prices in recent months has been arrived after the peak of the 2020-21 milk season. This indicates a promising signal for the coming milk season. Milk solid production is anticipated to rise by 1.9% in the 2020-21 season, despite marginally lower dairy cow numbers.

The government plans to grow the agritech sector as an economic driver so that the sector is better placed to serve both domestic and international markets. The Agritech Industry Transformation Plan (ITP) was developed in collaboration with government agritech taskforce, encompassing seven Government agencies, and a specially formed industry group, Agritech New Zealand.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

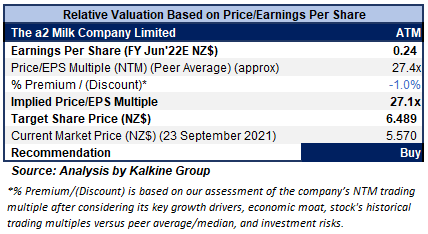

1) The a2 Milk Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$4.33 billion)

Business Description:

The a2 Milk Company Limited (NZX: ATM) improves the lives of its customers by providing the nutritional values of nature through the naturally occurring a2 Milk difference.

Outlook:

As per the annual report released on 26 August 2021, the company is confident of its sound fundamentals and relevant growth opportunities in core markets. Further, it is focused on product development, category growth, and new markets, supported by a healthy brand and strong balance sheet, for the long-term positive outlook. However, existing uncertainty and fluctuation in the consumer markets primarily led by COVID-19 circumstances and other market dynamics, particularly in China, the company has decided not to share specific guidance on revenue or EBITDA margin at this time.

Further, the company is anticipating H1FY22 revenue (including MVM) to be marginally below than H1FY21. Also, the FY22 gross margin is anticipated to be broadly like FY21 (excluding FY21 stock write-downs and before consolidating the MVM business in FY22).

Valuation Methodology: Price/Earnings per Share Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight discount to its peers’ average, considering continuing uncertainty and volatility in the consumer markets, primarily due to COVID-19 related circumstances and other rapidly changing market dynamics, particularly in China.

For the purposes of relative valuation, we have taken peers such as Scales Corporation Ltd. (SCL.NZ), New Zealand King Salmon Investments Ltd. (NZK.NZ), Sanford Ltd. (SAN.NZ), to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $5.57 per share (New Zealand Time: 11:33 AM (GMT +12) on 23rd September 2021.

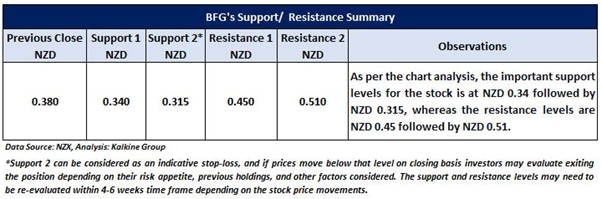

2) Burger Fuel Group Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$19.13 million)

Business Description:

Burger Fuel Group Limited (NZX: BFG) deals in the restaurant business and has more than 20 years of experience. It operates 3 brands: Shake Out, BurgerFuel and Winner Winner.

Outlook

The company’s healthy cash position, lower operating costs, and no debt, positions it well to counter the business challenges amidst the spread of a new variant of the pandemic. Besides, with the re-opening of economies in general and New Zealand in particular trading conditions have improved substantially. Apart from improving trading conditions which augur well for the Hospitality Sector as a whole, the company continues to review its options on a possible sale, merger, joint venture, or alternative processes to streamline its operations thereby create value for its stakeholders.

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the aforesaid facts, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.38 per share, up 2.70%, on 23rd September 2021.

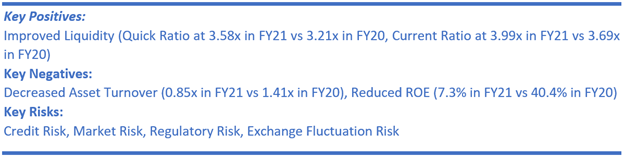

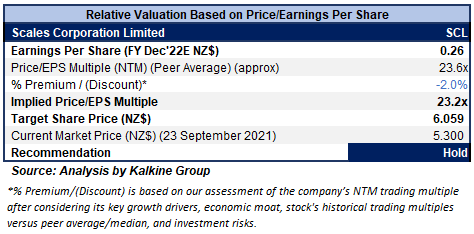

3) Scales Corporation Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$754.69 million, Gross Dividend Yield: 4.905%)

Business Description:

Scales Corporation Limited (NZX: SCL) is engaged in the agri-business. It operates in three divisions that include, horticulture, logistics, and food ingredients, in adjacent primary sectors.

Outlook

Amid strong H1FY21 result, the company has upgraded its full year guidance. Underlying Net Profit is anticipated to be in the ambit of $32.0-$37.0 million, implying an Underlying EBITDA in the range of $65.0-$72.0 million. Broadly, the company continues to anticipate disruptions to domestic and international operations including labour shortage, global markets, and supply chains due to COVID-19 related circumstances. However, the company is confident on its diversified focus which would mitigate some of the limited due to COVID-19.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight discount to its peers’ average, considering a decrease in gross margin at 29.3% in H1FY21 versus the industry median of 39.2% and a fall in fixed asset turnover to 0.97x in H1FY21 vs 1.04x in H1FY20.

For the purposes of relative valuation, we have taken peers like Sanford Ltd. (SAN.NZ), The a2 Milk Company Ltd. (ATM.NZ), and Select Harvests Ltd. (SHV.AX).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $5.30 per share, down 1.49%, as of 23rd September 2021.

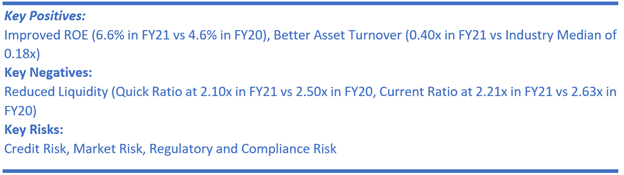

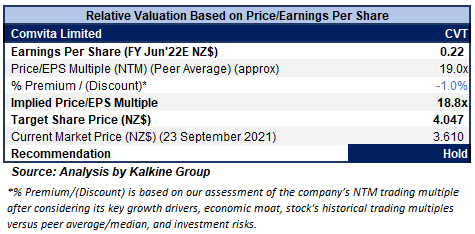

4) Comvita Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$253.52 million)

Business Description:

Comvita Limited (NZX: CVT) is one of the leading players globally in producing Manuka honey. The company has a wide geographical sales presence across Australia, New Zealand, China, and North America, among other countries.

Outlook

The company anticipates FY22 EBITDA in the range of $27.0-$30.0 million, driven by an expectation of continued double-digit top & bottom-line growth in focus growth markets. Digital revenue is anticipated to contribute at least 38% to total revenue and mid-single-digit revenue growth is anticipated in the ANZ market. Meanwhile, the transformation program continues with a $2.5 million investment within guidance and aiming a further reduction in inventory from $100.0 million to $90.0 million. Capital expenditure investment of circa is projected at $18.0 million.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight discount to its peers’ average, considering the higher inventory level, which the company is planning to reduce from $100.0 million to $90.0 million during FY22.

For the purposes of relative valuation, we have taken peers like Synlait Milk Ltd. (SML.NZ), Delegat Group Ltd. (DGL.NZ), and Fonterra Shareholders' Fund. (FSF.AX).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $3.61 per share, up 0.84% on 23rd September 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...