.png)

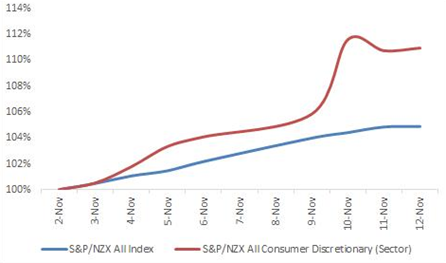

Exhibit 1: S&P/NZX All Index v/s S&P/NZX All Consumer Discretionary (Sector) (MTD Basis) *

Source: S&P Dow Jones Indices

*November 2, 2020 to November 12, 2020

The above chart reflects that S&P/NZX All Consumer Discretionary (Sector) has outperformed S&P/NZX All Index on MTD basis by ~6.02%. The outperformance could be as a result of lifting of restrictions, favorable news with regards to vaccine development, better consumer confidence, upcoming Christmas season, and decent growth expectations.

At the time New Zealand entered Alert Level 4 in late March, sales in the supermarket were up, and panic-buying led to a substantial increase in demand. Those stores which had access to the online market and whose products were considered ‘essential’ also did well.

Exhibit 2: Major Electronic Card Transactions in Retail Sector (January 2020 -October 2020)

Source: Stats NZ, Kalkine Group

Exhibit 3: Electronic card transactions in Retail Industry

Source: Stats NZ, Kalkine Group

By industry, the Y-o-Y movements were:

Rise in Retailers Confidence as the Second Lockdown Restrictions Lifts

As per the latest report published by Retail NZ, in the month of September, 45 % of retailers stated that their sales improved versus the same time last year. Also, retailer confidence has improved with 78% of retailers stating that they are confident that their business will survive the next 12 months. This is an increase from 64% recorded in last month. The online market supported retailers in the time of the pandemic as 77% of retailers are now trading online. This is a noteworthy increase in the digital capability since the beginning of the year.

Normally, retail businesses operate on very low net margins, and if consumers are unable to shop, there are cashflow issues that can threaten the survival of retail businesses.

Opportunities for New Zealand’s Retail Sector

Improvement in domestic economic conditions will increase the demand for retail goods. However, the sector can face challenges over the coming years from disruptions in supply and rise in the online retailing’s share of the total retail market. Nevertheless, online retailing also presents opportunities for savvy operators.

With the improvement in the domestic economy, income levels of New Zealanders and willingness to spend are likely to rise substantially over the coming years. In this situation, retailers’ capability to restore profit margins will also increase.

Online retail sales have grown substantially during the time of the pandemic. For retailers who sell their goods online, distribution is a crucial consideration. It is unquestionable that online retailing is transforming the face of retailing in the country and around the world. An online existence not only opens the door to the country’s consumers, but it gives retailers the chance to sell abroad more easily.

Few minor retailers have the capability to deliver from their existing location, but shops which have a huge online presence are required to consider warehousing outside city centres and nearer to transport routes. This will place additional demand on industrial warehousing in some areas and rising pressure on rent prices for some warehouse owners.

Exhibit 4: Growth drivers for NZ Retailers

Source: Kalkine Group

Importance of Retail Sector in New Zealand

The retail sector in New Zealand employs about 10 percent of the total workforce wherein about 90 percent of retail businesses employ lesser than 10 people and the larger retail businesses employ almost half of the total workforce. Thus, it forms a crucial part of New Zealand’s economy. The sector is dominated by small and medium enterprises (SMEs). It has been experiencing immense changes including a shift from unorganized to organized retailing.

Over the past three decades, growing internet and mobile phone penetration have completely changed the ways of doing business. The country is at the cusp of the digital revolution. The internet has become an integral part of the population. The declining of broadband subscription prices, the advent of 4G, and now 5G services have led to the convenience of online shopping which is providing a fillip to E-commerce.

Retailers need to evolve themselves to survive the challenge of online shopping, digital disruptions, and changing trend of consumer preference. Retailers need to differentiate themselves by ensuring consumer satisfaction, whether online or in-store. Given the backdrop of growing aspirations, stores that manage to combine the digital retail world with physical comfort will stand out. Retailers are required to be pro-active, conduct the research, understand what is happening and what is going to impact their businesses and plan how they can combat or embrace it.

There is an opportunity for New Zealand retailers to grow and improve with the right kind of strategies in place; they should know what state their business is in and how creating of digital channels could be supportive to their business and brand building as a bad experience for customers can have a big impact on brand awareness and loyalty.

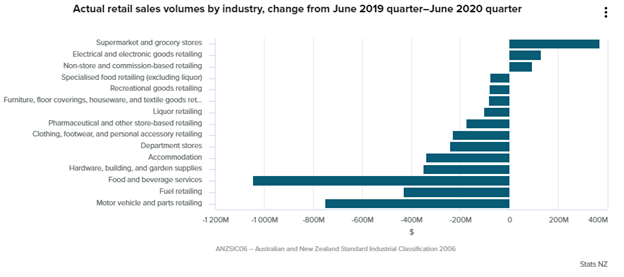

Exhibit 5: Actual Retail Sales Volumes by Industry

Source: Stats NZ

The volume of total retail sales after adjusting for price and seasonal effects, fell 15% in the June 2020 quarter, after a 1.2% decline in the March quarter.

However, the retail sector has broadly started recovering in August and sales rebounded in September following the easing of restrictions. Reported sales in September were up 19.6% against last year, although total sales from March to September were down 2.7%. However, sales activities are unevenly spread across the sector, and merely a third of retailers reported that their sales were down. The wage subsidy has helped many people employed in the sector and has helped support customers spending.

Amidst the gloom, the COVID-19 brought about great opportunities for online business. About 77% of retailers are now trading online. This is a substantial increase in digital capability.

There has been a bounce back in retailer’s confidence, post easing of restrictions. About 78% of retailers have reported that they are feeling confident that their businesses will survive. Uncertainty around the economic impact of the pandemic led to a fall in consumer confidence in April to 84.8 – roughly around the same level where it was during the Global Financial Crisis of 2008. It rebounded by 8 and 12 points in May and June, respectively.

Key Challenges

Retailers in New Zealand have been facing many challenges but the biggest of them is the sourcing of products all along the retail supply chain, from manufacture right down to anticipated demand on the shop floor, post COVID-19 related disruptions. Many retailers are also concerned about the ongoing lack of overseas customers, the uncertainty that comes with the current trading environment and the possibility of further lockdowns, and difficulties finding qualified staff.

Outlook

There is no denying the fact that the retail sector is facing unprecedented challenges. While many retailers appear increasingly pessimistic about the business prospects going ahead, focusing on customers’ needs with a differentiated retail proposition and omni-channel offer will be crucial to overcoming the present crisis. The sector is likely to receive a big boost with the news that a vaccine from Pfizer company has been tested with 90 percent success. Developments like this will give rise to confidence amongst consumers and for that matter amongst retailers, and we can expect a return to ‘new normal’ soon.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the retail sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Briscoe Group Limited (NZX: BGP) (Recommendation: Hold, Potential Upside: Low Single-Digit) (M-Cap: ~NZ$932.13 million, Gross Dividend Yield: 2.990%)

About the Company

The stores of Briscoe Group Limited operate within two retail sectors, sporting goods and homeware, under the three brand names: Living & Giving, Briscoes Homeware and Rebel Sport.

For the thirteen weeks ended 25 October 2020, the company reported total sales of $161.3 million, up by 14.97% Y-o-Y. For the third quarter, homeware sales were up by 12.28% Y-o-Y to $98.7 million, while sporting goods sales stood at $62.6 million, an increase of 19.48% Y-o-Y.

Outlook:

The company has witnessed recovery in its business after the national lockdown ended in May. The second half of FY21 has started strongly in regard to sales, gross profit dollars and gross profit percentage, despite the closing of Auckland stores for 19 days in August. However, the economic outlook for second half of the year is very uncertain.

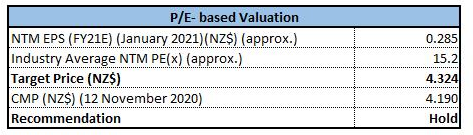

Valuation Methodology: P/E multiple-based relative valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low single digit (in % terms).

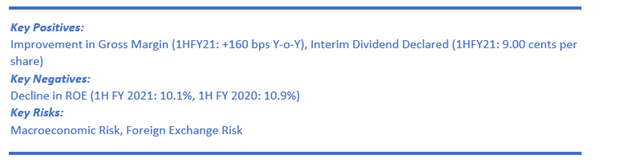

Considering the improvement in gross margin and expected upside in the stock price, we give a “Hold” recommendation on the stock at the current price of NZ$4.190 per share, up by 0.24% on November 12, 2020.

2) The Warehouse Group Limited (NZX: WHS) (Recommendation: Hold, Potential Upside: Low Single Digit) (M-Cap: ~NZ$828.95 million, Gross Dividend Yield: 4.649%)

About the Company

The Warehouse Group Limited has evolved from a single The Warehouse store to become one of the leading retailing groups in NZ.

Outlook:

The company expects significant reduction in retail demand as the complete economic impact of COVID-19 is felt by customers over the course of FY21. In the month of June 2020, the company confirmed that it would accelerate some of the changes already planned. These changes include some store closures as well as operational changes.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low single digit (in % terms).

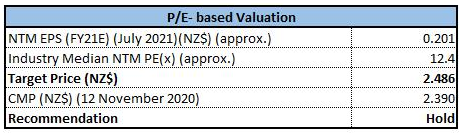

3) Hallenstein Glasson Holdings Limited (NZX: HLG) (Recommendation: Hold, Potential Upside: Low Double-Digit ) (M-Cap: ~NZ$373.4 million, Gross Dividend Yield: 8.667%)

About the Company

Business Description: Hallenstein Glasson Holdings Limited happens to be a non-trading holding company. The principal trading subsidiaries are Glassons Limited, Glassons Australia Ltd (involved in retail of women’s apparel), Hallenstein Bros Limited as well as Hallenstein Brothers Australia Limited (retail of men’s apparel). Notably, subsidiaries are 100% owned by Hallenstein Glasson Holdings Limited.

Outlook

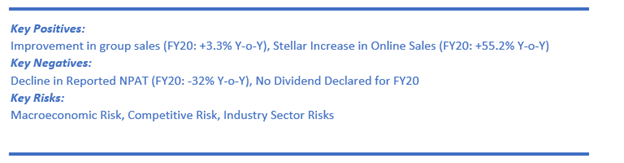

The first eight weeks of FY21 have witnessed sales growth of +10.71% Y-o-Y, which has been mainly driven by online sales as physical store growth has been slower, particularly in CBD locations. Whilst this is a positive result, the company would be careful in regard to the future impacts of coronavirus.

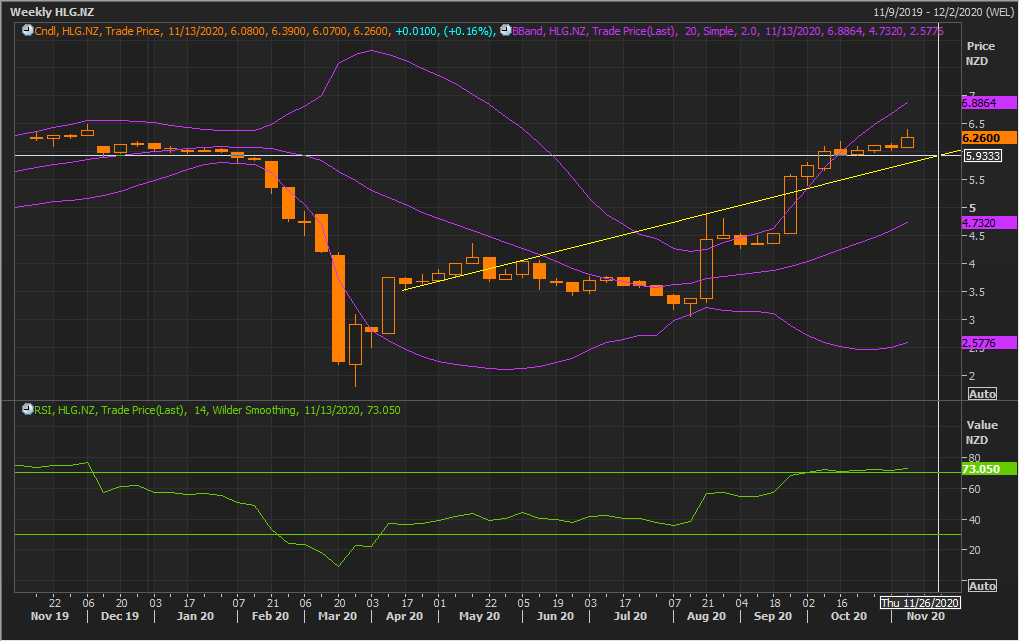

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status https://www.bollingerbands.com/

Going forward, the stock may have resistance around the upper Bollinger band of $6.88 whereas on price retreating, it may find good support around $5.93, as has been derived from the trend line.

Considering the technical analysis and better current ratio as compared to the industry median, we give a “Hold” recommendation on the stock at the current price of NZ$6.260 per share, up by 0.16% on November 12, 2020.

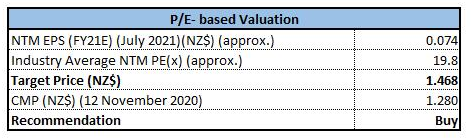

4) Kathmandu Holdings Limited (NZX: KMD) (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: ~NZ$907.52 million)

About the Company

Kathmandu Holdings Limited (NZX: KMD) is a marketer, designer, wholesaler and retailer of footwear, apparel, and equipment for surfing and outdoors. The company operates in New Zealand, Australia, North America, Europe, South East Asia as well as Brazil.

Outlook

The company has witnessed mixed same store sales performance during the first seven weeks of FY21 due to the disruption triggered by the COVID-19, with store closures observed at Melbourne, Auckland, Hawaii, Bali, and stores at airport. However, the market is now expected to improve in the coming period. The company’s investment into omni-channel capabilities allows it to quickly respond to the shifts in consumer habits as well as robust growth in online demand.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...